- within Real Estate and Construction topic(s)

Welcome to Edition 36 of P2N0 covering the drive to avoid, reduce and remove greenhouse gas (GHG) emissions to progress to net-zero GHG emissions (NZE).

P2N0 covers significant news items globally, reporting on them in short form, focusing on policy settings and legal and project developments and trends.

This Edition 36 covers key news items arising during the period commencing October 1 through October 15, 2025. Edition 37 will cover the period commencing on October 16 through October 31, 2025. During the week beginning October 20, 2025, we will publish an update on Article 6 of the Paris Agreement.

As previously, P2N0 will not cover news items about M&A activity, or that are negative.

Access previous editions of P2N0 at bakerbotts.com.

KEY NEWS ITEMS FROM OCTOBER 1 TO OCTOBER 15, 2025

The story of CO2 is the Story of Everything: During the first few days of October 2025, the author read Peter Brannen's book, The Story of CO2 Is The Story of Everything.

While P2N0 is not intended to provide book reviews, occasionally a book is worthy of recommendation for those active in decarbonization and the energy transition. This is one of those books.

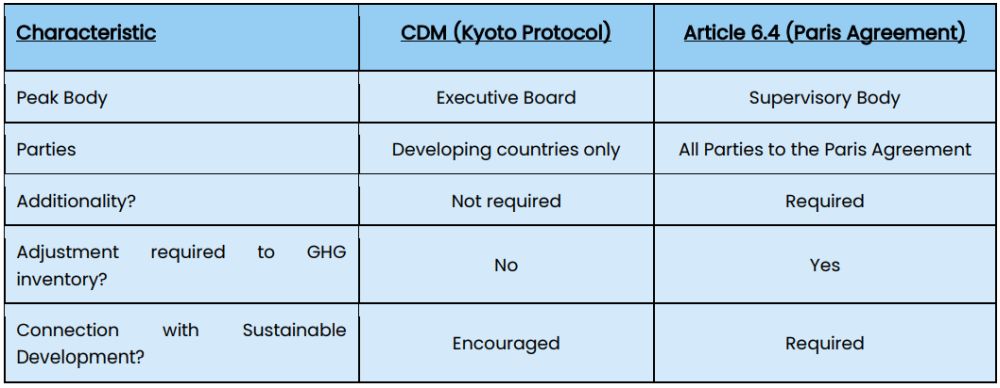

Article 6.4 Supervisory Body (A.6.4.SB) met October 6 to 10, 2025 in Bonn, Germany:

The Meeting Report of Eighteenth meeting of the Article 6.4 mechanism Supervisory Body provides a summary of the outcomes of the meeting.

Among other things, the Meeting Report states that A.6.4.SB:

- adopted the draft "Standard: Addressing non-permanence and reversals in mechanism methodologies", as contained in annex 13 to the Meeting Report;

- agreed a Common Practice Analysis Tool, which helps check whether a type of project is already widespread in a region, ensuring that credits are only given for projects that go beyond what is already happening, a concept known as "additionality"; and

- agreed to accredit four further independent auditors tasked with validating and verifying projects - also known as a Designated Operational Entities or DOEs.

Among other things, the A.6.4.SB is establishing the infrastructure and rules for the Paris Agreement Crediting Mechanism (PACM).

"[The PACM] will allow countries and other actors to cooperate in reducing greenhouse gas emissions by generating high-integrity carbon credits, while also supporting sustainable development".

Ahead of the meeting in Bonn, the key matter (arising from feedback received from parties to the Paris Agreement) for consideration was the proposed permanence standard to apply to reversals under the PACM.

At the core of the concept of the creation of any carbon credit is that:

- the carbon credit represents one tonne of CO2-e of GHG emissions (avoided, reduced or removed from the climate system though a mitigation activity); and

- the carbon credit can be used to offset one tonne of CO2-e of GHG emissions, and that corporations or other organizations place value on "high-integrity" carbon credits that allow this offset.

Article 6.4 of the Paris Agreement provides a global framework to allow the creation, registration and transfer of carbon credits for value.

Logically, this requires additionality, i.e., the mitigation activity giving rise to the avoidance, reduction or removal is in addition to "business-as-usual", and the avoidance, reduction or removal must be permanent. This may be regarded as current orthodoxy.

The challenge with many nature-based solutions (N-B Ss) is that they are not permanent – for example, in the case of CO2 captured by afforestation or reforestation, while the mitigation is additional, it is not permanent because on death of a tree, GHG emissions will be emitted as organic matter decomposes1.

This is the core of the debate about permanence. This debate (and each issue related to it) is not new.

Note: The following is text taken from presentations given by the author since 2019, including in the context of explaining the long-term role of carbon capture and storage as a permanent technology, rather than as a bridging technology only as framed under the European Union CCS Directive2. The thinking is that of the author, based on fundamental principles relevant to all carbon credits, not the application of Article 6.

Ahead of speaking at the IICCS Conference in Jakarta, Indonesia, October 7 and 8, 2025, the author had cause to reflect that the issue of permanence remains the same, as does the conceptual solution.

Corporations and other organizations acquire carbon credits so as to avoid having to avoid, reduce or remove GHG emissions here and now. From a policy setting perspective, corporations and other organizations should acquire carbon credits at a point in time where they are no longer able to avoid, reduce or remove GHG emissions by adopting low, lower and no carbon technologies. In this context, the carbon credits must be permanent, or the basis of the accounting for them must recognize if they are not permanent, and provide a basis for continued avoidance, reduction or removal [arguably in respect of both the GHG emissions arising from the continued activities giving rise to GHG emissions and the GHG emissions arising from the decomposition of the organic matter].

If a corporation or other organization acquires a carbon credit to defer the timing of investment to adopt a lower, low or no carbon technology, the issue of permanence is different because the corporation or organization should not be seeking to account for avoidance, reduction or removal on a permanent basis.

In short, this issue of permanence is neither an "either or" nor a "one sizes fits all" answer.

By way of reminder:

The key elements of the PACM are:

- If a Party to the Paris Agreement (Party) wants to participate in the PACM that Party must establish a Designated National Authority (DNA);

- Any Party may host an activity in its country (host

country) giving rise to mitigation outcomes in respect of

GHG emissions in the host

country, and if that activity gives rise to a mitigation

outcome, emission reduction units will be created taking the form

of:

- Authorized Emission Reduction (AER):

- A6.4ERs that have received an authorization under paragraph 42 of the Rules4, modalities and procedures of the mechanism; and

- A6.4ERs are ITMOs (when they are first transferred) and are reported in the Agreed Electronic Format (AEF) / Article 6 Database and accounted for in the structured summary; or

- Mitigation Contribution Units (MCU):

- MCUs are not ITMOs (as there have been no adjustments) and the mitigation achieved through MCUs assists the host country in achieving its NDC (or development goals); and

- MCUs can be used, among other things, for results-based climate finance, domestic mitigation pricing schemes, or domestic price-based measures, for the purpose of contributing to the reduction of emission levels in the host country.

- The transition of the Clean Development Mechanism (CDM), created under the Kyoto Protocol, is to be achieved and the A.6.4SB has developed a Procedure to effect the Transition of CDM activities to the PACM.

- Authorized Emission Reduction (AER):

The deadline for Host Country Approval (HCA) of the transition of a CDM to the PACM is December 31, 2025. It is understood that 2,462 CDM projects have applied for HCA, and that 356 have received HCA.

Nationally determined contributions (NDCs) updated:

While the original deadline to lodge revised NDC was February 2025 (see Edition 24 of P2N0), many countries (that are Parties to the Paris Agreement) have continued submitting revised NDCs as COP-30 approaches.

- China's new commitment to reduce GHG emissions by

7% to 10% by 2035: Following the announcement that China

intends to reduce its GHG emissions by 7% to 10% by 2035 (based on

having reached peak CO2 emissions by 2030).

The announcement was made by President Xi Jinping over video link to the United Nations Climate Summit 2025 on September 25, 2025.

Some previous announcements by President Xi announcing targets on climate change have already been achieved. Most notably, the commitment to achieve 1,200 GW of installed renewable energy capacity by 2030 had been achieved in June or July 2024.

Also, China is well on the way to achieving peak CO2 emissions by 2030 and carbon neutrality before 2060 (the Dual Carbon Goals).

China is approaching the fifth anniversary of its setting of the Dual Carbon Goals. It is four years since the National Voluntary Greenhouse Gas Emission Reduction Trading Market – see the section titled China's National Carbon Market below for a Progress Report of China's National Carbon Market.

- In addition to China, during September

2025 over 35 countries (as Parties to the

Paris Agreement) revised their NDCs (each an NDC

3.0), including:

- Australia which committed to reduce GHG emissions by 62% to 70% of 2005 levels;

- Bangladesh which committed to reduce GHG emissions by 84.97 million metric tonnes on a business as usual (BAU) basis;

- Nigeria which committed to reduce GHG emissions by 184.9 million metric tonnes of CO2-e;

- Pakistan which committed to reduce GHG emissions by 1,280 million tonnes of CO2-e on a BAU basis; and

- Russian Federation which committed to reduce

GHG emissions by 65% to 67% of 1990 levels.

A link is attached to the UNFCCC NDC Registry.

- NDCs can be defined in a number of ways,

including:

- to reduce GHG emissions by a stated percentage below an earlier date;

- to apply a BAU approach, typically, where GHG emissions of the country are going to continue to increase on a projected BAU basis, with a stated mass or percentage to be stated to be reduced compared to that BAU.

Renewable energy outstrips coal and natural gas:

- On October 7, 2025, the International

Energy Agency (IEA) published Renewables 2025 – Analysis and forecasts to

2030.

The headline findings from the publication are as follows:

- Global renewable electrical energy capacity is expected to increase to 4,600 GW by 2030, with photovoltaic solar capacity to account for 80% of the increase;

- In the context of the long-identified need to triple renewable

electrical energy capacity (reflected in the pledge arising from

COP-28 in November 2023 to which

200 countries committed), the increase to 4,600 GW

will fall short of tripling but may be regarded as keeping the

tripling within stretching distance.

The publication is excellent and may be regarded as compulsory reading for those active across the renewable energy sector.

- On October 7, 2025, Ember

reported (under Global Electricity Mid-Year Insights

2025) that:

" ... solar and wind outpaced the growth in the global electricity demand in the first half of 2025, resulting in a very small decline in [the use of] both coal and gas, compared to the same period last year".

In the context of the Ember report, Senior Electricity Analyst, Malgorzata Wiatros-Motyka stated:

"We are seeing the first signs of a crucial turning point. Solar and wind are now growing fast enough to meet the world's growing appetite for electricity. This marks the beginning of a shift where clean power is keeping pace with demand growth".

The Ember report is excellent.

- During September 2025, it was reported widely

that, across the Australia National Electricity grid:

- 48.8% of the electrical energy transmitted across the national grid was generated from renewable electrical energy; and

- 47.6% of electrical energy generated from coal powered sources.

This is a first for Australia.

Energy Outlooks:

- bp Energy Outlook – 2025 edition

lands:

In late September 2025, bp Energy Outlook – 2025 edition was published. This bp publication is one of the flagship reports published each year and is eagerly anticipated.

As always, the bp publication is excellent and is well-worth a read.

- The headlines from the bp publication are as follows:

- Artificial Intelligence or AI applications are providing a new source of energy demand, including in markets in which demand growth for electrical energy has stalled or reduced;

- Energy efficiency improvements have not progressed at the rate hoped or needed, and has resulted in a lag in the progress in energy transition; and

- CO2 emission have not yet peaked: We are approaching the 10th anniversary of the signature of The Paris Agreement in December 2015. If CO2 levels stay at current levels for the next 10 years, it will be "increasingly challenging" to stay "within a 2OC carbon budget".

- The trends identified in the bp publication

include the following:

- Energy Security continues to be a key focus of most countries across the world. While the trend is clear, the impact of the trend at a country-by-country level is different. A deeper dive on this trend, is recommended;

- Natural gas and oil production continues to grow year-on-year, with demand in China and in developing countries contributing to oil production and the growth in LNG production capacity, with no sign of a slowdown in the medium term and citing the bp publication: "global LNG exports are set to increase by more than half by 2035 relative to 2024";

- Low carbon energy continues to be a function

of the increased development and deployment of photovoltaic solar

and wind capacity, with increased development and deployment

keeping pace with rising demand for electrical energy (because of

economic development and urbanization) and is now being developed

at a rate to displace non-renewable sources of electrical energy

generation.

As recognized consistently, the challenge for the deployment of renewable electrical energy is the need to develop, augment and expand transmission and distribution systems and infrastructure.

Finally, the good folk at bp stated that which has been apparent to most folk for a long time now:

"The development of less mature higher cost low carbon energy vectors and technologies – including low carbon hydrogen and sustainable aviation fuel ... remain at a very early stage and heavily dependent on policy and regulatory support".

- DNV Energy Transition Outlook 2025:

On October 8, 2025, DNV published Energy Transition Outlook 2025 – A global and regional forecast to 2060.

The headline findings from the DNV publication are as follows:- Policy resets in the US will have a marginal impact on global energy transition;

- Energy security policy settings will result in lower GHG emissions over time;

- EV and photovoltaic solar will continue to reach new milestones as the rate of green electrification increases;

- While the rate of increase in electrical energy capacity is being driven by AI, by 2040, AI will be responsible for around 3% of electrical energy demand, a little below that required for EV and airconditioning; and

- GHG emissions will fall by less than half by 2050, and as such decarbonization will not progress to a level consistent with net-zero GHG emissions.

- ExxonMobil 2025 Global Outlook:

By way of remainder: On August 28, 2025, ExxonMobil published ExxonMobil 2025 Global Outlook.

The ExxonMobil publication provides the outlook of ExxonMobil through 2050. As with the bp publication, the ExxonMobil publication is eagerly awaited, not least because of the consistency and the pragmatism of the publication.

The by-line for the ExxonMobil publication is:

"Increasing global energy supply and reducing emissions is not only possible. It's essential".

For those active across the energy sector, and the hydrocarbons sector in particular, this need has long been apparent.

The ExxonMobil publication is excellent and is well-worth a read.

The key takeaways from the ExxonMobil publication are as follows:

- All types of energy are needed for a lower emission and

prosperous future, with:

- Renewable energy capacity installation increasing at the fastest rate through 2050;

- Coal to decline the most; and

- Natural gas and oil to make up more than 50% of the energy mix;

- Increasing living standards and urbanization in developing economies will result in a 25% increase in energy use, including because of increased rates of electrification, as well as increased use;

- The industrial and transport sectors underpin the world economy, and each sector will require increased supply of energy;

- CO2 emissions arising globally will fall by 25% by 2050, the affordability of decarbonization being determinative; and

- Sustaining investment in the natural gas and oil sectors will

be more important than ever.

- Value Chains in Africa: On October 6, 2025,

the IEA published Stepping Up the Value Chain in Africa –

Minerals, materials and manufacturing. The IEA

publication provides a helpful view, focusing on the

potential of the CM3 sector across Africa.

The key findings of the IEA publication are as follows:

- Africa is endowed with vast resources;

- Markets exist; and

- As yet, the realisation of the economic benefit of the

vast resources has been limited and uneven.

The IEA publication is well-worth a read providing a helpful perspective on the potential of Africa, and the countries within it

- National Agroforestry Strategy (2025 –

2035): In October 2025, the

Ministry of Environment, Climate Change and

Forestry published National Agroforestry Strategy

(2025 – 2035).

The publication recognizes the fact that economic development, environmental and climate change mitigation, and the resulting focus on sustainability are interrelated and that policy settings are needed to create and enhance economic activity for populations that are increasing while at the same time ensuring sustainability.

The publication is one of the best that the author has read on agroforestry.

- India installs 29.5 GW of photovoltaic solar to September 30, 2025: On October 14, 2025, it was reported widely that India had installed 29.5 GW of photovoltaic solar capacity in the first nine months of 2025.

- Alphabet to develop USD 15 billion AI data hub in India: On October 13, 2025, it as reported widely that Google parent company (Alphabet) intends to invest USD15 billion to develop an AI data hub in the State of Andhra Pradesh. As reported, the CEO of Google Cloud stated: "It's the largest AI hub that we are going to be investing in anywhere in the world, outside the United States".

- India's USD 77 billion master plan for hydroelectric power: On October 13, 2025, the Central Electricity Authority (CEA) of India announced that it intends to develop a 10,000 km transmission system, with 12 GW of HVDC capacity, to transmit electrical energy from hydroelectric power stations (comprising 64.9 of hydroelectric capacity in the traditional sense and 11.1 GW of pumped storage) by 2035.

- ACME Green Steel to Vietnam: On

October 13, 2025, it was reported widely

ACME (of India) had signed an agreement to supply

8 million metric tonnes of green steel to Stavian

Industrial Metal (of Vietnam).

- Renewable electrical energy accounted for 90% of new

electrical energy capacity in the US: On October 2, 2025,

it was reported widely that renewable electrical energy accounted

for 90% of new electrical energy capacity in the US during the

first seven months of 2025.

The Federal Energy Regulatory Commission (FERC) reported that around 19.4 GW of new renewable electrical energy was installed (16.05 GW of photovoltaic solar and 3.288 GW wind). As might be expected, the balance of the installations comprised 2.2 GW of gas-powered capacity,

- Data Center Load Growth: On October 1,

2025, the good folk at Monitoring Analytics published a

report on increased demand for

electrical energy across the PJM Capacity

Market.

The basic conclusion of the report is:

"that data center load growth is the primary reason for recent and expected capacity market conditions, including total forecast load growth, the tight supply and demand balance, and high prices".

The report goes on to state: "The current conditions ... are almost entirely the result of load additions from data centers, both actual historical and forecast".

While the report is specific to the PJM Capacity Market, the basic conclusion of the report may be regarded as relevant to the dynamics across electrical energy transmitted across grids to supply electrical energy to data centers as the application of AI continues to drive increased load.

- Photovoltaic Desertification Control Plan: During the first part of October 2025, there was increased coverage outlining the plans for China to install up to 253 GW of photovoltaic capacity over 670,000 hectares of land that has been desertification, principally across the Taklamakan and Tengwer deserts.

- State Government of South Australia to seek

LDES: On October 8, 2025, it was reported

widely that the State Government of South Australia is to conduct a

tender process to procure long-duration energy storage

(LDES) – a world first.

As reported, South Australia will seek up to 700 MW of LDES capacity over the next six years under the auspices of its Firm Energy Reliability Mechanism (FERM). The LDES will operate alongside the BESS capacity already installed, being installed, and contracted to be installed.

For helpful background on LDES, see The Competitive Position of Long-Duration Storage Solutions in the Power System published by the good folk at DNV. - 1 GW of BESS sought to provide system stabilization services: On October 2, 2025, it was reported widely that Transgrid is to conduct a tender process under which it is to award contracts for the provision of system stabilization services across its transmission network. The system stabilization services will be provided by the dispatch of electrical energy stored in BESSs across the Transgrid network.

- ROK to develop a USD 580 fuel cell power plant: On October 2, 2025, it was reported widely that the Republic of Korea is to develop a fuel cell plant located in Gyeongju, North Gyeongsang Province, as a bridge from grey hydrogen to green hydrogen (Gangdong Hydrogen Fuel Cell Power Generation Project).

- China's National Carbon Market: During the

final week of September 2025, the Ministry

of the Ecology and Environment of the People's Republic of

China published its Progress Report on China's National

Carbon Market. It is a little over four years since

the National Voluntary Greenhouse Gas Emission Voluntary

Trading Market (National Carbon

Market).

The Progress Report notes that that "National Carbon Market has become an essential tool in accelerating green transition in all aspects of economic and social development".

Further, the Progress Report notes that advancing the National Carbon Market is:

- a potent and cost-effective measure for achieving "Dual Carbon Goals";

- a crucial task in deepening reform in ecological conservation; and

- a vivid practice of supporting high-quality development with high-level protection.

- All types of energy are needed for a lower emission and

prosperous future, with:

- The headlines from the bp publication are as follows:

The Interim Regulations for the Management of Carbon Emission Trading entered into force in May 2024.

The Ministry of Ecology and Environment (MEE) has worked to ensure effective implementation of the Interim Regulations. Under the Interim Regulations, Departmental Rules exist, in the form of Measures for the Administration of Carbon Emissions Trading and Measures for the Voluntary Greenhouse Gas Emission Reduction Trading, with three sets of Supporting Guidelines under each of the Measures.

The Progress Report is a worthwhile read.

By way of reminder: Edition 35 of P2N0 (under China to accelerate the roll-out and roll-up of its carbon market) reported that: On August 26, 2025, it was reported widely that China by 2030 will have "a transparent, standardized and internationally aligned voluntary carbon market". It is understood that this policy setting is endorsed by both the Chinese Communist Party and the State Council.

China started its carbon market in July 2021, with the market initially covering the electrical energy sector, and set to expand to include the aluminium, cement, iron, and steel industries during 2025.

- China developing largest clean energy UHVDC

transmission line: During September 2025,

China commenced the development of the largest

ultra-high-voltage-direct-current

(UHVDC) transmission line to run from

Tibet to Guangdong-Hong

Kong-Macao.

The UHVDC transmits renewable electrical energy from photovoltaic capacity covering 162 square miles in Gonghe County, Qinghai province, China.

As reported, the 2,681 km, USD 7.5 billion, UHVDC transmission line is to transmit 10 GW of electrical energy. - IEA on ASEAN Power Grid: On September

30, 2025, the good folk at the IEA

published Driving global and regional collaboration

to realise the ASEAN Power Grid Vision.

The publication continues the on-going dialogue around the development of an ASEAN Power Grid to connect countries across ASEAN, enabling low-cost or the lowest-cost cross-border electricity transmission. The publication is worth a read.

- Magnon the source for biogenic CO2: On October 15, 2025, it was reported widely that Magnan is to produce biogenic feedstock to allow the production of hydrogen derived e-methanol. As reported, Magnon will supply up to 200,000 metric tonnes of biogenic CO2 annually.

- Smart Energy blows into Scotland: On October 13, 2025, it was reported widely that Mingyang Smart Energy intends to invest £1.5 billion to develop a wind turbine manufacturing facility in Scotland.

- Innovation Fund IF 25 Heat Auction T&Cs published: On October 10, 2025, the EC published the Terms and Conditions of the provision of up to €1 billion of funding support to encourage acceleration of decarbonization of heating across the EU.

- Google to translate in Belgium: On October 9, 2025, it was reported widely that Google plans to invest €5 billion in Belgium with the investment being to expand the capacity of the Google data centres, including for the purposes of increased capacity for AI. In addition, Google is to invest in onshore wind farm capacity to supply renewable electrical energy to the data centres.

- Federal German Government to provide €6 billion

for industrial decarbonization: On October 6,

2025, it was reported widely that the Federal German

Government had announced the provision of up to €6

billion in funding support to decarbonize the industrial

sector, including, for the first time, to fund carbon capture and

storage.

It is understood that the funding will be provided under 15-year contracts under which the Government will provide funding to support the industrial sector transitioning to low, lower and no carbon technologies. As reported, corporations and other organizations wishing to participate in the funding rounds for 2026 will have to register interest by December 1, 2025. - Greater definition on cause of Iberian electrical

energy outage: Edition 30 of

P2N0 reported on the

electrical energy outage that affected around 60 million

people on April 28, 2025.

On October 3, 2025, the European Network of Transmission System Operators for Electricity (ENTSO-E) issued a Factual Report reporting on the data and the facts arising in the lead up to the outage, and its impacts. The Factual Report is entitled Grid Incident in Spain and Portugal on 28 April 2025 – ICS Investigation Expert Panel Factual Report.

The headline is that the "root cause" of the outage was "cascading overvoltage" with the grid unable to reboot automatically to stem the problem, and then to reboot. The Factual Report is around 260 pages in length but is well worth the effort to read. As reported, a more detailed report will be published in 2026.

The European Union (EU) is taking action to avoid any recurrence, with the European Commission (EC) reported to be working on the EU energy security framework to ensure that the lessons learned from the outage are fully integrated into updated policies and measures. As reported in P2N0, the cause of the outage was not renewable energy. The EU is scheduled to share draft legislation to recognize the need for greater resilience in grid infrastructure on November 25, 2025.

What is clear is that grid investment is needed, and needed urgently, in the EU and the US. The EC estimates that by 2040 around €477 billion will need to be invested in the transmission grid, and around €730 in distribution networks to ensure that the supply from renewable electrical energy sources can be transmitted and distributed to match load at data centres and increased electrification of industry and transport.

During the second week of October 2025, it was reported widely that France, Germany, Spain and Sweden have curtailed, and have plans to continue to curtail, the dispatch of renewable electrical energy from wind power so as to ensure system integrity and stability. Over time, the need for curtailment will lessen as the transmission and distribution systems are augmented. - Tata Steel to receive €2 billion for

decarbonization using GH2: On October

2, 2025, it was reported widely that the government of the

Netherlands (Dutch Government) is to provide

between €4 billion and €6.5

billion to allow the transition to "gas-based direct

reduction technology" from "coal-fired blast furnace

technology" (at the Tata iron and steel

production facilities at Ijmuiden) including the move to convert

coal-fired power plants to natural gas and then from natural gas to

GH2. As reported in previous editions of P2N0, iron and steel

production are responsible, directly, for the emission of up to

2 giga-tonnes (i.e., 2 billion

tonnes) of GHG emissions annually.

More broadly, the plan includes the deployment of carbon capture and storage technology as well as the possible production of biomethane using captured CO2.

As reported, the Dutch Government and the Province of North Holland have entered into a letter of joint intent for the purposes of this initiative.

- Federal German Government acceleration: On October 2, 2025, the Cabinet of the Federal German Government adopted the Hydrogen Acceleration Act.

- Repsol green lights 100 MW GH2 project: In

late September 2025, it was reported widely that

Repsol had directed the commencement of

construction to develop its €300 million, 100 MW,

GH2 production facility in

Cartagena, Spain.

As reported, the GH2 production facility will produce 15,000 metric tonnes of GH2 a year to be used to decarbonize industrial activities and replace GHG emitting fuel sources. The Cartagena GH2 production facility was designated at an Important Project of Common European Interest (IPCEI) and was allocated €155 million in funding support under the Institute for Diversification and Saving Energy (IDEA) initiative. - TotalEnergies winds big: During late

September 2025 it was announced by

TotalEnergies that it is to develop and to operate

the 1.5 GW Centre Manche 2 offshore wind field

(OWF) off the coast of Normandy, northern

France.

As announced, TotalEnergies will invest €4.5 billion in the development of the OWF.

HELPFUL PUBLICATIONS AND DATA BASES

In addition to publications covered by this edition of P2N0, the most noteworthy publications read by the author during the period from October 1 to October 15, 2025, are:

- The Joint Research Centre (JRC) of the European Commission published Pipelines for hydrogen transport: A review of integrity and safety challenges. While the publication does not give rise to any surprises, it is well-worth a read.

- Organization for Economic Cooperation and

Development (OECD) published Governing with Artificial Intelligence

– The State of Play and Way Forward in Core Government

Functions. The publication is timely, focusing on the

rate of progress of the public sector in adapting and using

AI. Almost all of its coverage of

AI is in the context of its use by the private

sector, and the resulting demand for electrical energy and for

water. As governments adopt and use AI in the

public sector, the demand for electrical energy and water will

increase.

The publication, while lengthy, is well worth a read. - Defossilizing Industry: Considerations for

Scaling-up Carbon Capture and Utilization Pathways – White

Paper was published by the World Economic

Forum during September 2025.

The publication does not add to the commonwealth of knowledge, rather it provides a helpful outline of the potential size and shape of the CCS sector.

Footnotes

1. Carbon Capture and Storage involves the capture of CO2 that would otherwise be emitted to the climate system and the storage of that CO2 (sequestration) permanently and securely in a geological formation. This avoids the emission of CO2 into the climate system. Carbon Capture and Use involves the capture of CO2 that would otherwise be emitted to the climate system, and the use of it for an industrial use, including to produce products that do not store CO2 permanently. Carbon Dioxide Removal or CDR involves the removal of CO2 that is already in the climate system (from the climate system) and the storage of the CO2 in a more stable form of carbon, which is not permanent. This removes CO2 emissions already in the climate system. N-Bs may be regarded as CDR.

2. Directive 2009/31/EC of the European Parliament and of the Council of 23 April 2009 on the geological storage of carbon dioxide and amending Council Directive 85/337/EEC, European Parliament and Council Directives 200/60/EC, 2001/80/EC, 2004/35/EC, 2006/12/EC, 2008/1/EC and Regulation (EC) No 1013/2006.

"A mechanism to contribute to the mitigation of greenhouse gas emissions and support sustainable development is hereby established under the authority and guidance of the Conference of the Parties serving as the meeting of the Parties to the Paris Agreement (CMA) for use by Parties on a voluntary basis".

4. United Nations Framework Convention on Climate Change (UNFCC), 3/CMA3, Rules, modalities and procedures for the mechanism established by Article 6, paragraph 4, of the Paris Agreement, Annex, Section V.C., paragraph 42.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.