- within Tax topic(s)

- in Canada

- with readers working within the Banking & Credit, Healthcare and Construction & Engineering industries

- within Tax topic(s)

- within Insurance and Law Practice Management topic(s)

1. Individuals

1.1 Personal Income Tax

Bosnia and Herzegovina (BiH) consists of two entities, the Federation of Bosnia and Herzegovina (FBIH) and Republika Srpska (RS) as well as a third region called the Brčko District (BD) in the north of the country which was created in 2000 out of land from both entities. It officially belongs to both, but is governed by neither, and functions under a decentralized system of local government.

Resident individuals pay tax on their worldwide income, while non-residents are only taxed on income sourced in BiH.

1.1.1 Residency

An individual is resident if the following conditions apply:

- They spend more than 183 days in a calendar year in the FBIH/RS

- They have a residence or business of vital interest in the territory of BIH

1.1.2 Tax Base

The tax base in the FBIH is the total gross taxable income paid by the employer less employee contributions and deductible allowances (monthly basic personal allowance, less dependent family member allowance(s) and disability allowance, where applicable).

Similarly, in the RS, the tax base is the total gross taxable income paid by the employer less social security contributions and deductible allowances (monthly basic personal allowance, less dependent family member allowance(s) and disability allowance, where applicable).In RS min salary has been increased based on school diploma-min salary is now 900 BAM, mandatory middle school 1.000 BAM and colleague degree 1.300 BAM.

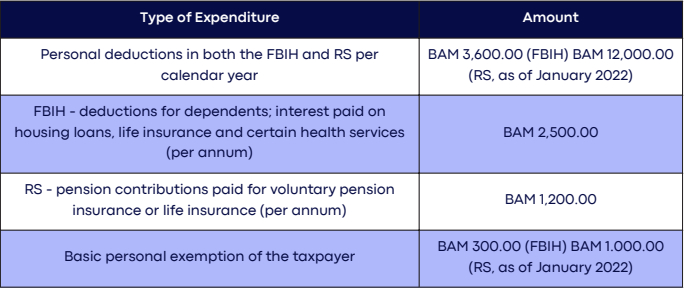

1.1.4 Deductible Expenses

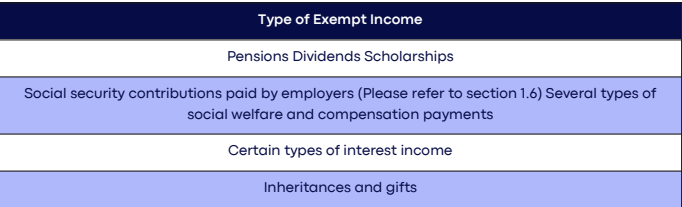

1.1.5 Exempt Income

1.2 Capital Gains Tax

Capital gains are not taxable in the FBIH. In the RS, capital gains are taxed at the rate of 13% and include gains arising from the sale of immovable assets, gains arising from the sale of property rights, authorship rights, license, and franchise rights.

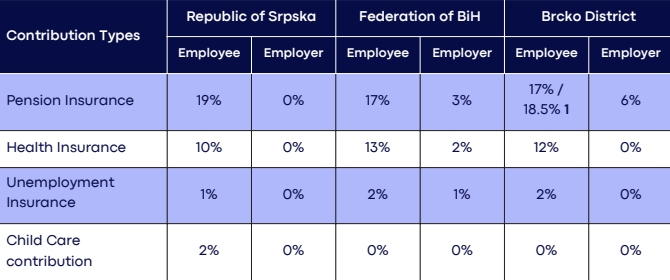

1.3 Social Security Contributions

Notes:

1 If FBIH Pension laws applicable the rate is 17%, but if RS Pension laws applicable the contribution rate is 18.5%.

2.Corporate Tax

2.1 Corporate Income Tax

Resident companies are taxed on their worldwide income, while non-resident companies are taxed on profits derived from sources in the FBiH/ RS and/or Brčko.

2.1.1 Residency

A company in BIH is resident if it is registered as a legal entity there. An entity has a taxable presence in BIH by carrying out business activities in the jurisdiction that meets the criteria for a permanent establishment.

2.1.2 Tax Rates

BiH corporate income tax rate is a flat 10%, which is one of the lowest tax rates in the region.

.jpg)

To view the full article clickhere

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.