- with Senior Company Executives and HR

- in India

- with readers working within the Accounting & Consultancy and Law Firm industries

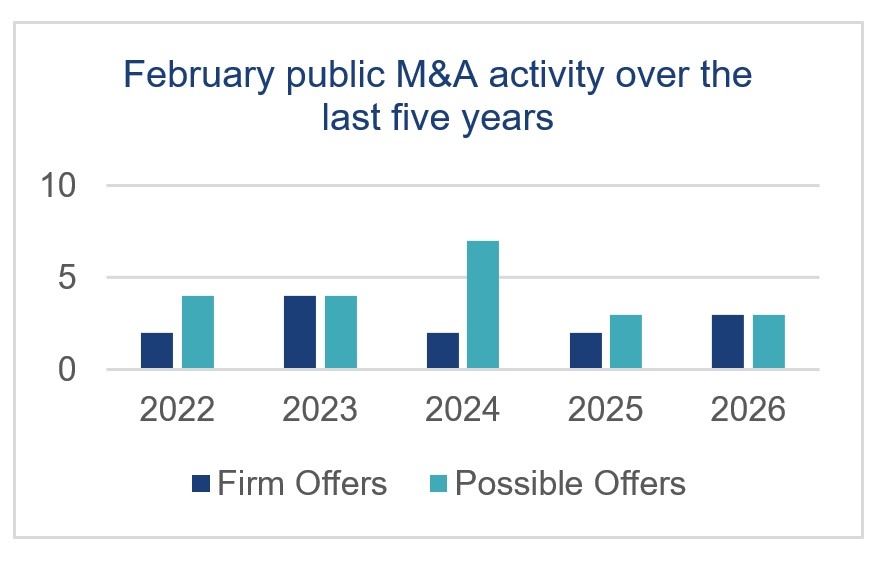

In February 2026, there were three Rule 2.7 announcements made across the UK public M&A market and three further possible offers announced.

Firm Offers announced this month:

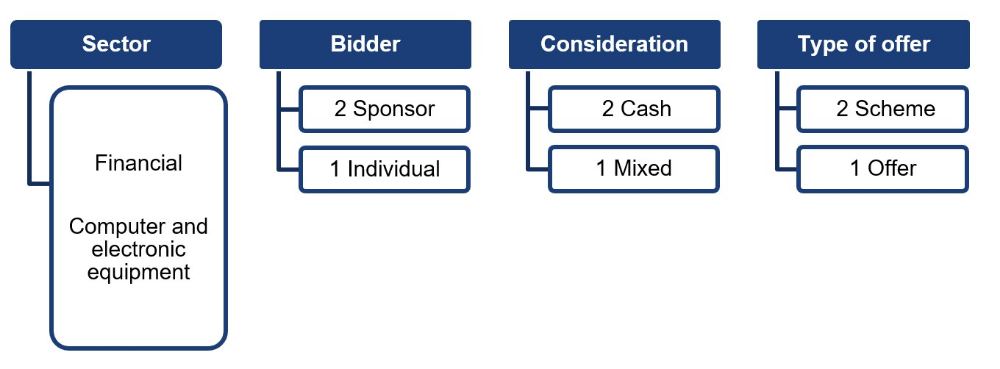

- Recommended cash offer by Nuveen, LLC for Schroders plc – £9.9 billion – public to private

- Recommended cash offer by Mark Furness for essensys plc – £11.3 million – public to private – unlisted securities alternative

- Recommended cash offer by Verdane Fund Manager AB for Augmentum Fintech plc – £185.7 million – public to private

Possible Offer announced this month:

- Possible offer by Helios consortium for CAB Payments Holdings plc – £213 million – cash and unlisted securities alternative

- Possible offer by Esyasoft Holding Ltd for CyanConnode Holdings plc – £35 million – cash consideration

- Possible offer by Advent International Limited for Senior plc (private sale process)

Firm Offers breakdown this month:

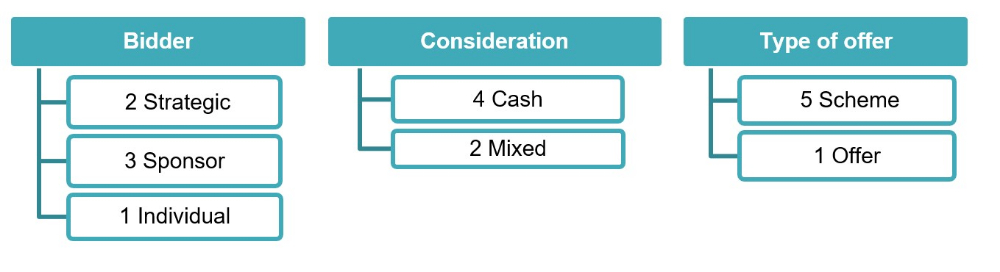

Year to date breakdown:

February 2026 Updates:

Takeover Code changes on share buybacks, companies with DCSSs and IPOs in force

The changes to the Takeover Code on how the Code applies on a share buyback, how it applies to companies with a dual class share structure (DCSS) and the disclosures required under the Code on an IPO (which were set out in RS 2025/1) have now come into force. The Takeover Panel has also published new Notes to advisers.

The key rule changes relate to:

- Share buybacks – The rules around share buybacks have been made clearer, and in particular when an obligation to make a mandatory offer may be triggered by a buyback that takes a shareholder's interests through 30%.

- Companies with a DCSS – A DCSS company typically has both ordinary voting shares and a class of shares with an enhanced level of voting rights or control, held for example by a founder of the company. The new Code provisions primarily apply to a structure where the 'founder' shares carry multiple votes per share and then are extinguished or converted to ordinary shares on particular trigger events, such as a "time sunset" a specified number of years after the company's IPO or the retirement/resignation of the founder shareholder. The new rules set out a framework for how the Takeover Code applies to DCSS companies, including how the mandatory bid requirement applies when a shareholder's percentage of voting rights is increased as a result of the conversion or extinction of the founder shares, and how the acceptance condition on a contractual offer for a DCSS company should work.

- IPOs – On an IPO that would result in a company becoming subject to the Code, the company will have to disclose any controlling shareholders (and their concert parties) and describe the mandatory offer requirement under the Code in its prospectus/admission document. The ability of the Panel to grant a "Rule 9 dispensation by disclosure" has also been codified – meaning that the Panel will be able to grant a dispensation from a potential future obligation for a shareholder to make a mandatory offer (for example, upon the conversion or extinction of founder shares in a DCSS company, or the conversion of convertible securities), if certain criteria are met.

The Takeover Panel has published a new Note to advisers in relation to IPOs or admissions to trading on the disclosure requirements on an IPO and a revised version of its Note to advisers in relation to Rule 9 waivers to reflect these changes.

For more information on the rule changes, see our UK public M&A e-bulletin here.

UK Public M&A podcast EP38: Shareholder opposition on some recent takeovers by way of scheme

In this episode, we talk about a number of recent takeovers by way of scheme where the target shareholders have either voted the scheme down, or the vote has been very close.

We also discuss what bidders and targets can do if it looks like the vote will be close.

To listen to the full conversation please visit SoundCloud, Spotify or Apple.

February 2026 Insights:

February has seen activity levels broadly consistent with the same period in 2025. There has been a slight increase in firm offers compared to 2025, up from two to three. The number of possible offers match the number of possible offers seen in February 2025. February was an active month for the financial sector, with two firm offers and one possible offer.

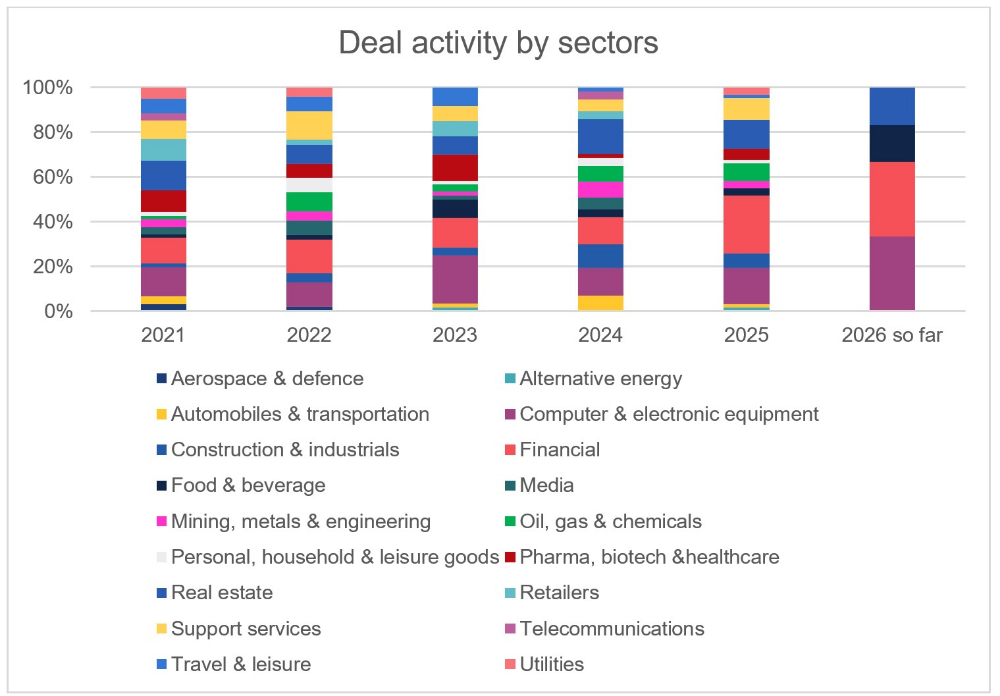

In two of the three firm offers announced this month, bidders targeted the financial sector, unsurprising given the sector's momentum, with firm offers rising from seven in 2024 to 16 in 2025. Alongside computer & electronic equipment and real estate, financials have repeatedly topped the activity chart, reflecting deep asset pools, technology refresh cycles and ongoing consolidation. The next few quarters will test whether they can maintain that momentum as macro conditions shift and capital seeks new pockets of growth.

Useful links

- Herbert Smith Freehills Takeovers Portal.

- Herbert Smith Freehills Public M&A Podcast Series.

- The Takeover Code.

- The Takeover Panel's Disclosure Table (detailing offeree companies and offerors currently in an offer period).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.