- within Government and Public Sector topic(s)

The recently published Budget Measures Implementation Bill introduces a number of legislative amendments aimed at giving legal effect to the measures announced in the Government's Budget. The Bill proposes changes across several areas of the tax framework, reflecting the authorities' ongoing efforts to update existing legislation, introduce targeted relief measures, and align domestic provisions with current economic and regulatory priorities.

This article provides a summary of the principal provisions contained in the Budget Measures Implementation Bill, highlighting the key amendments and their potential implications for taxpayers and practitioners.

Amendments to the Income Tax Act

With effect from Year of Assessment 2026

1. Addition to the definition of 'Company'

The definition of 'Company' in Article 2 of the ITA has been extended to include also:

Any Special Limited Partnership Fund established in accordance with the Investment Services Act (Special Limited Partnerships Funds) Regulations.

With effect from Year of Assessment 2027 (for points 2 - 4)

2. Additional deduction on scientific research

Article 14 currently allows for a deduction, spread over 6 years, of any expenditure on scientific research incurred for the use and benefit of the trade, business, profession or vocation, as long as such capital expenditure is not deductible under the Deduction for Wear and Tear of Plant and Machinery Rules.

Subsequent to this Article, a new paragraph introduces a new deduction with similar provisions, with an additional incentive:

- Any expenditure incurred on research, development and innovation activities incurred for the use and benefit of a trade, business, profession or vocation;

- Deduction inflated to 175% of the actual amount of such expenditure;

- Spread equally over 6 years, as long as such capital expenditure is not deductible under the Deduction for Wear and Tear of Plant and Machinery Rules.

Further Rules are expected to clarify the eligible expenditure under the new Article.

3. Increase in deduction on fees in respect of homes for the elderly and the disabled

The maximum deduction by a person who has paid fees on his own behalf or on behalf of a family member in respect of residence in a private home for the elderly or the disabled or at a respite centre for the disabled has been increased from €2,500 to €4,500.

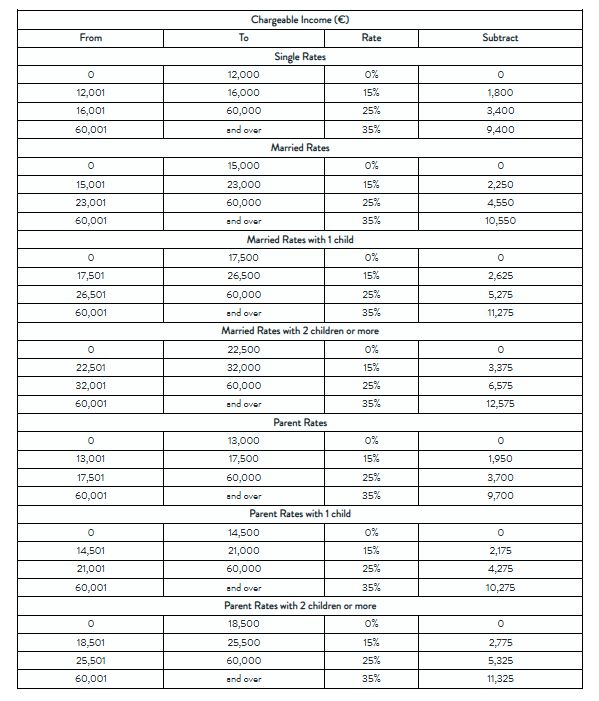

4. Changes to Tax Rates

New tax rates have been implemented as proposed in the 2026 Budget. The new tax rates, applicable from basis year 2026, are as published on the MTCA website:

Amendments to the Value Added Tax Act

5. Amendments to Definitions

Similarly, there are amendments to existing definitions (such as public authority, non-profit making organisation), as well as the addition of the definition for "revenues acts".

6. Dues vs Refunds

Article 24 currently defines the refund of excess credit to persons registered under Article 10 and provides for the circumstances under which VAT refunds may be withheld on account by the Commissioner. With effect from 1st January 2026, the Commissioner shall also be allowed to set off any amount of excess VAT credit of a person (that is not offset against any output VAT liabilities), against any amounts due by that person to the Commissioner in accordance with any of the provisions of the revenue acts.

7. Self-Supplies

The Act provides clarifications on the VAT treatment of private use of goods forming part of an economic activity and services supplied free of charge, being supply of services for consideration made by that person itself.

8. Supplies between "related parties"

The VAT Act is also amended to include provisions determining the taxable value of certain supplies between related persons, including a definition and conditions for persons to be deemed related.

9. Means of Communication for both Tax and VAT Matters

Furthermore, any notice required to be given to a person by the Commissioner or any other person authorised by the Commissioner may now also be served electronically.

10. Preparing for VIDA

Amendments to the provisions concerning the facilitation of supplies of goods through an electronic interface, distance sales, and call-off stock arrangements are to come into force on 1st January 2027.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]