- within Tax topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- in Canada

- with readers working within the Accounting & Consultancy, Business & Consumer Services and Technology industries

- within Tax topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- with readers working within the Accounting & Consultancy and Law Firm industries

A. INTRODUCTION

The scope of this article

In this study we shall try to identify how the income of trusts is taxed in Cyprus, having in mind its idiomorphic concept as to the dual separation of the ownership of the trust property, to legal and beneficial.

The matter will be also examined, considering the two main types of trusts established in Cyprus, Local and International1.

The concept of trust

A trust is the relationship by which a person called the trustee, holds property, the trust property, settled to the trust by the settlor, for the benefit of some other persons, called the beneficiaries.

The type of trusts which are the subject matter of this article, are the written express trusts and not those created by operation of law such as the constructive or resulting trusts.

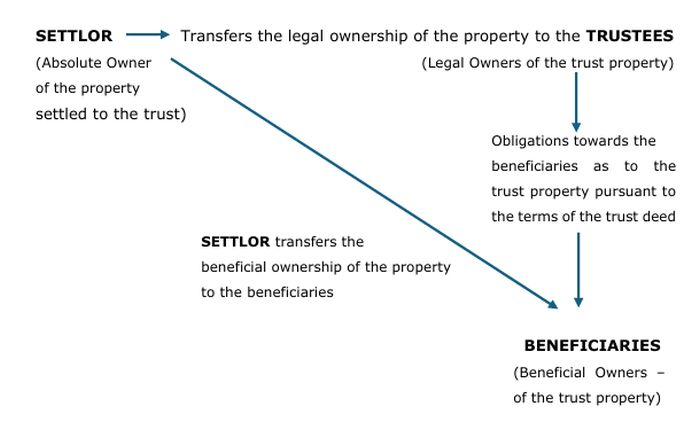

The diagram of an express written trust looks like this:

The basic concept of the trust, and at the same time its magnificence, is that the property, once entrusted to the trustees, has two owners at the same time. The legal owner of the property which are the trustees and the beneficial owner which are the beneficiaries.

The role of the trustees for tax purposes

Any property settled to the trust by the settlor as its capital and any income received from any operations, is administered by the trustees being its legal owners.

The trust does not have legal personality and for this reason any trust property is held by the trustees in their names on behalf of the particular trust as per the terms of the trust deed, having identified beneficiaries, the beneficial owners, who ultimately have the expectation to become its legal owners as well.

The idiomorphic concept of the trust and its effect on taxation

This idiomorphic concept of the trust generated from the separation of the ownership as to the trust property, to legal and beneficial, raises concerns as to the taxation of the trust income distributed to or acquired by the trustees on behalf of the trust as per the terms of its deed. Whom to tax for the trust income, the legal owner or the beneficial owner?

B. TAXATION OF TRUSTS IN CYPRUS

The law

The taxation of Cyprus trusts, either Local or International, is governed by the general provisions of Art. 31 of the Income Tax Laws of 2002 No. 118(I)/20022. Art. 31 though, is not helpful as to the taxation of the trust income. It does not lay down methodology and procedures. It simply imposes to the trustees the obligation to collect and pay the tax due considering that this income belongs to the beneficiaries.

As mentioned above Article 31 the Trustees shall be subject to tax in respect of the income arising from trust property or business in the same manner and to the same amount as beneficiaries would be taxed if they had personally received such income.

Every such trustee, shall be responsible for carrying out all actions required under Income Tax Law for the assessment and payment of the relevant tax in respect of the income arising from such trust property.

In addition, as per the provisions of the Assessment and Collection of Taxes Law No. 4/78, articles 8 and 9, the trustees must prepare and submit a tax return for a specified tax year when required by the Commissioner, for tax resident beneficiaries and for non-tax resident beneficiaries but in the case of the later, for income arising from any source in Cyprus which is taxable in Cyprus.

Footnotes

1. As to the Cyprus International Trust, its set up, maintenance and management, please refer to our publication, “THE CYPRUS INTERNATIONAL TRUST, In detail…” which can be found at the following link: https://www.kinanis.com/Media/Uploads/Publications/Brochures%202026/THE%20CYPRU S%20INTERNATIONAL%20TRUST%20in%20detail.pdf

2. Tax liability of trustees 31. Trustees in bankruptcy or receivers, trustees, executors of wills or administrators of property or guardians entrusted with the management, control or administration of property or an undertaking on behalf of any person shall be liable to tax in respect of the income arising from such property or undertaking in the same manner and to the same amount as such person would be taxed if he personally received such income, and every such trustee, receiver, commissioner, executor of wills or administrators of property or guardian shall be responsible for doing all things necessary under this Law for the assessment and payment of tax:

Provided that nothing contained in this article shall preclude the imposition of tax in the name of the person represented by such trustee, receiver, commissioner, executor of wills or administrators.

To read this article in full, please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]