- within Finance and Banking topic(s)

- in India

- with readers working within the Automotive industries

- within Finance and Banking topic(s)

- in India

- within Criminal Law, Wealth Management and Intellectual Property topic(s)

Executive summary

Many corporate borrowers in DACH face a challenging situation: Weaker cash flows and rising interest burdens are colliding with more restrictive financing conditions

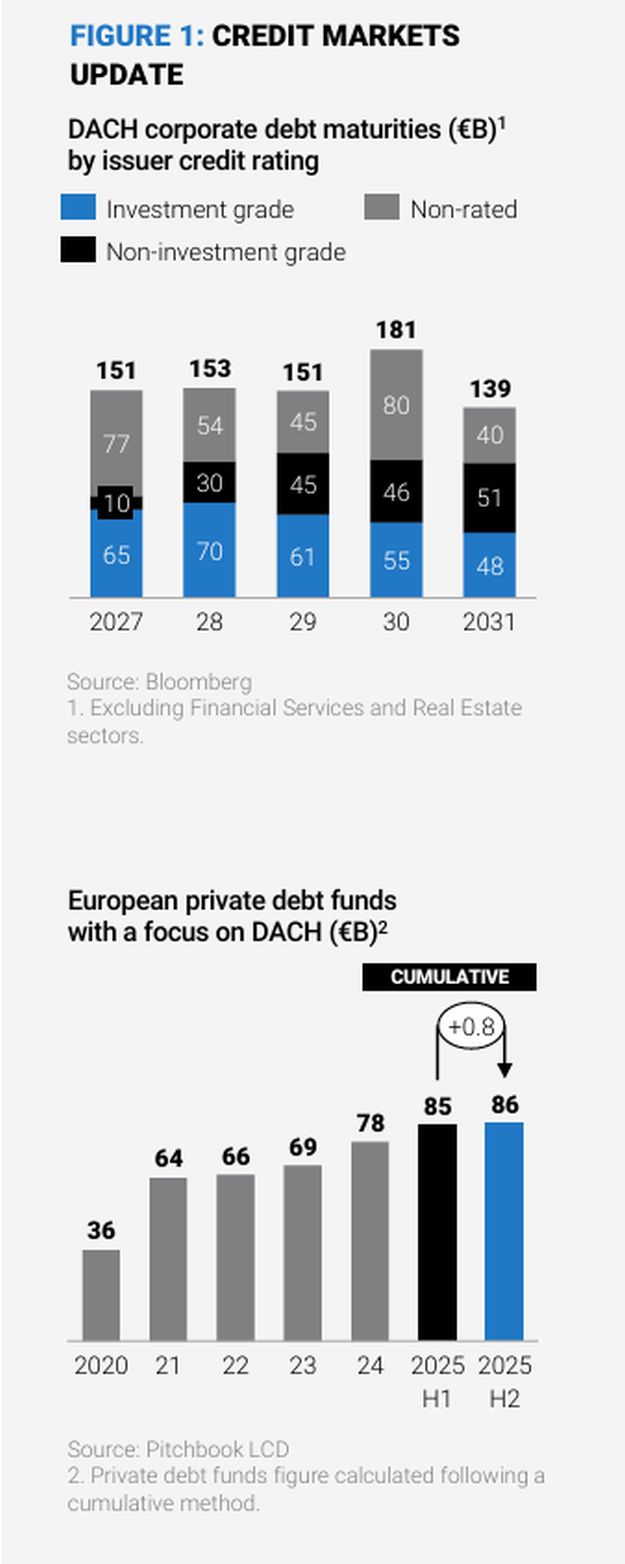

For a sample of more than 1,000 companies in DACH, €151 billion in corporate debt will mature in 2027 and must be repaid or refinanced over the coming months. This presents significant challenges for companies navigating strong commercial headwinds and tightening credit markets.

Financing conditions across the DACH region remain difficult as 2026 progresses and with the availability of new funding under pressure. In recent years, private debt funds offered an attractive alternative for companies that more traditional lenders were hesitant to fund. After a wave of redemption requests from their own investors since the beginning of 2026, private debt funds may not be a reliable source of new funding. And despite central banks’ interest rate cuts in 2025, financing costs for corporate borrowers remain stubbornly high.

The DACH region faces deep structural headwinds, including heavy bureaucracy and regulation, demographic challenges, rising labor costs, and severe geopolitical turmoil, which has resulted in new U.S. trade barriers, rising energy costs and weaker demand in export markets. Together, these pressures erode cash generation just as refinancing costs rise, drive up the cash interest burden. This leaves less room to invest in digitalization and automation, decarbonization, skills, supply-chain resilience, and product innovation.

The German automotive sector is particularly exposed. No other industry in the region is undergoing a transformation of such historic scale: weaker demand in Europe, additional U.S. tariffs, the structural loss of the Chinese market, and the shift away from internal combustion engines toward new powertrain technologies are all colliding. Against this backdrop, the sector faces acute pressure from rising external financing costs and the demands of funding a historic industrial transition.

In today’s environment, refinancing success depends on tight cash flow management and capital structures that are aligned with evolving market conditions.

Credit markets update

CORPORATE DEBT MATURITIES

For our sample of corporates in the DACH region, €151 billion of financial debt will mature in 2027. While the overall volume of debt requiring refinancing is already substantial, the composition is even more striking: €65 billion of this debt maturing in 2027 is investment grade, with the remainder being non-investment grade or non-rated. The refinancing burden is concentrated among borrowers that are likely to face closer lender scrutiny, tighter terms, and higher all-in funding costs.

Rather than a single repayment peak, 2027 marks the beginning of a period where refinancing conditions become significantly more demanding for many DACH corporates. Because large volumes of debt quantities mature in the following years, the next months will also set the tone for the longer refinancing cycle. Borrowers that move early and demonstrate control over liquidity and cash flow are likely to retain options; those that wait may find the market significantly less forgiving.

PRIVATE DEBT: STRESS TESTING THE MODEL

Our previous report in October 2025 argued that private debt was becoming a core pillar of DACH mid-market financing. Recent developments suggest that the outlook is more fragile. In March 2026, several large private-debt funds restricted investor withdrawals following elevated redemption requests, prompting increased scrutiny by regulators. In Germany, BaFin has characterized these developments as a warning signal, highlighting structural liquidity constraints and limited transparency in parts of the private debt market, with implications for funds’ ability to provide follow-on financing.

Private debt was once a core pillar of mid-market financing in the DACH region, but its growth has slowed, largely induced by the recent developments. In 2025, H2 activity was broadly flat at €86 billion of cumulative funding in DACH, compared with €85 billion in H1. Rising defaults, tighter liquidity management at fund level, and more selective investor behavior are tightening access to capital, widening funding gaps for certain borrower segments despite continued demand.

Refinancing landscape

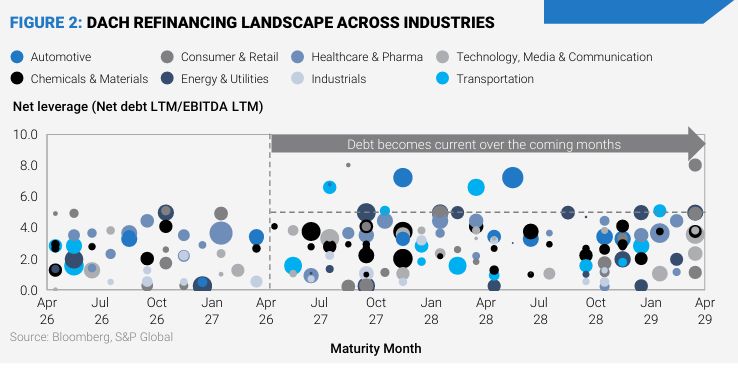

Refinancing outcomes for DACH companies are increasingly determined by the strength of balance sheets and cash flow quality, not simply by market access. Highly leveraged borrowers face more difficult negotiations than their lower levered peers. Spreads are wider, covenants are stricter, and lenders have little tolerance for earnings volatility when their primary focus is downside protection and near-term cash generation. Lower-levered companies retain meaningful flexibility and can absorb higher funding costs without existential strain, but they are not insulated either. Sustained interest expense at current levels acts as a persistent drag on free cash flow, and that drag becomes increasingly difficult to manage if revenue growth slows or margins come under pressure.

In DACH, €3.3bn of corporate debt due for refinancing or repayment in 2027 is concentrated in companies with net leverage above 5.0x, making execution challenging. This puts pressure on these companies to increase free cash flow through targeted measures.

CORPORATE INSOLVENCIES HIT 15-YEAR HIGH

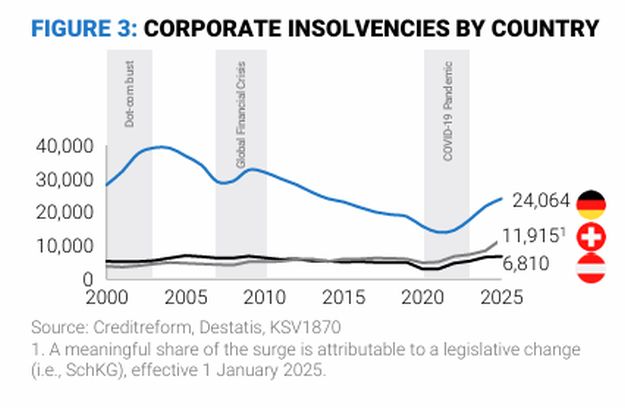

DACH corporate insolvencies continue to rise. An estimated 42,789 corporate insolvencies were recorded in 2025: the highest level in 15 years. That is up ~16% compared to 2024 (36,915 cases), after a ~21% surge the year before. Despite the current economic backdrop, insolvencies remain below levels seen after the dot-com bubble (~50,000 cases in 2004) and the Global Financial Crisis (~45,000 cases in 2009).

Financing costs are on the rise

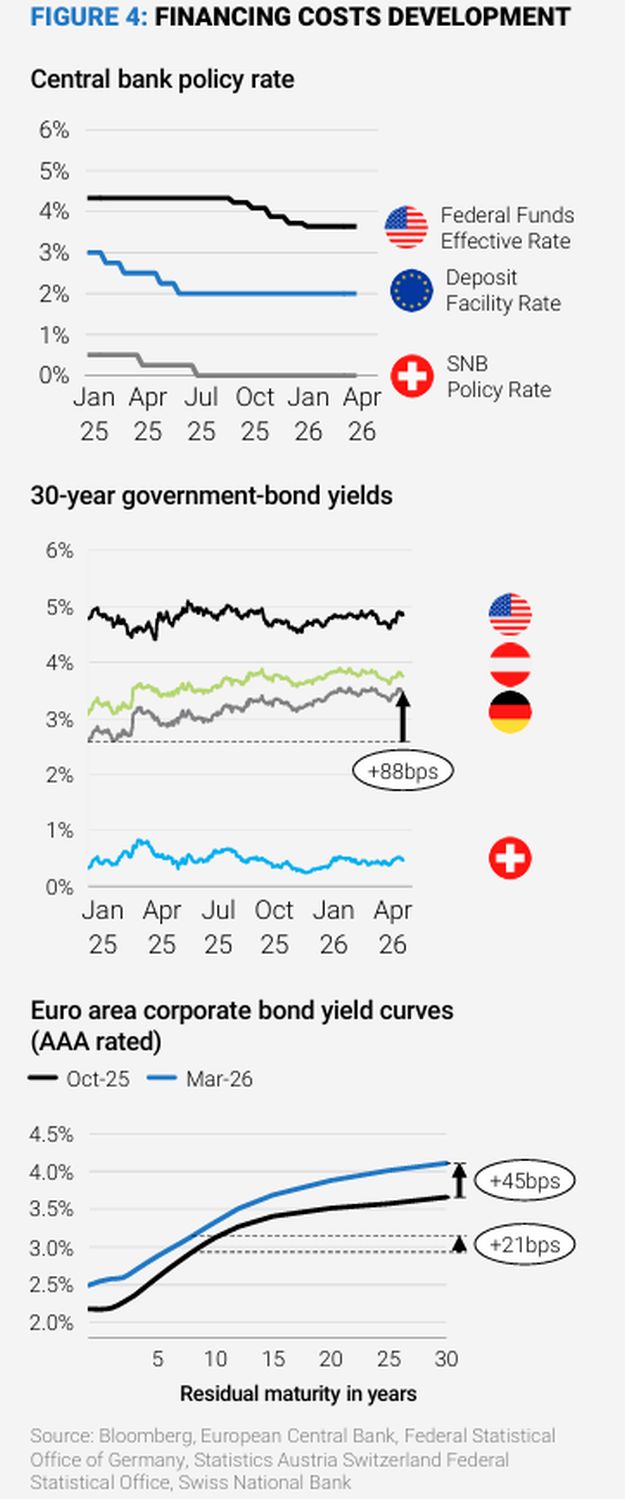

During 2025, the European Central Bank cut its key lending rate, the Deposit Facility Rate, by 1.0 percentage point, while the Swiss National Bank cut its rate by 0.5 percentage points. However, these short-term interest reductions have not affected longer-term interest rates paid by corporates and governments. On the contrary, long-dated government bond yields have risen since January 2025. Across many EU countries, including Germany and Austria, 30-year yields have increased by up to 88 basis points, with the sharpest moves occurring since mid-2025. The key driver of higher yields on long-term government debt is the United States: the scale of U.S. sovereign borrowing, together with persistent inflation uncertainty, elevated risk premia, and the fallout from the U.S. administration's new trade barriers and tariffs, is raising the global cost of capital.

In Germany, higher yields also reflect improved growth expectations after plans to spend more on defense and infrastructure, while in Austria long dated yields are also related to significant funding needs: Austria’s debt agency expects to issue approximately €43–47 billion of federal bonds in 2026, while the overall public deficit is projected to be around 4% of GDP. In Switzerland, local yields have risen less than elsewhere due to very low inflation expectations and the SNB has kept its policy rate at zero. Safe-haven demand can reinforce this trend. In recent months, German Corporate bond yields have risen across the full range of maturities. Since we issued our last report in October, financing costs for AAA-rated issuers have risen by approximately 20–45 basis points, creating additional strains on companies’ ability to borrow.

Cash flow meets capital structure

Across more than 350 of the largest companies in DACH that publish financial results, nominal revenue has grown by around 31% since 2019, and EBITDA grew by approximately 32%. These figures compare with cumulative inflation of approximately 18% across DACH during the same period (Germany 20%, Switzerland 5%, Austria 26%).

On the surface, these headline figures suggest solid performance. But free cash flow1 has grown by only 1% over the same timeframe. The gap between earnings growth and cash generation is not a rounding error. It reflects a structural erosion in cash conversion, driven by rising capital expenditure requirements, working capital absorption, and transformation related spending that does not flow through EBITDA but still consumes cash. The sector is generating more revenue, more EBITDA, and almost the same amount of free cash flow as in 2019.

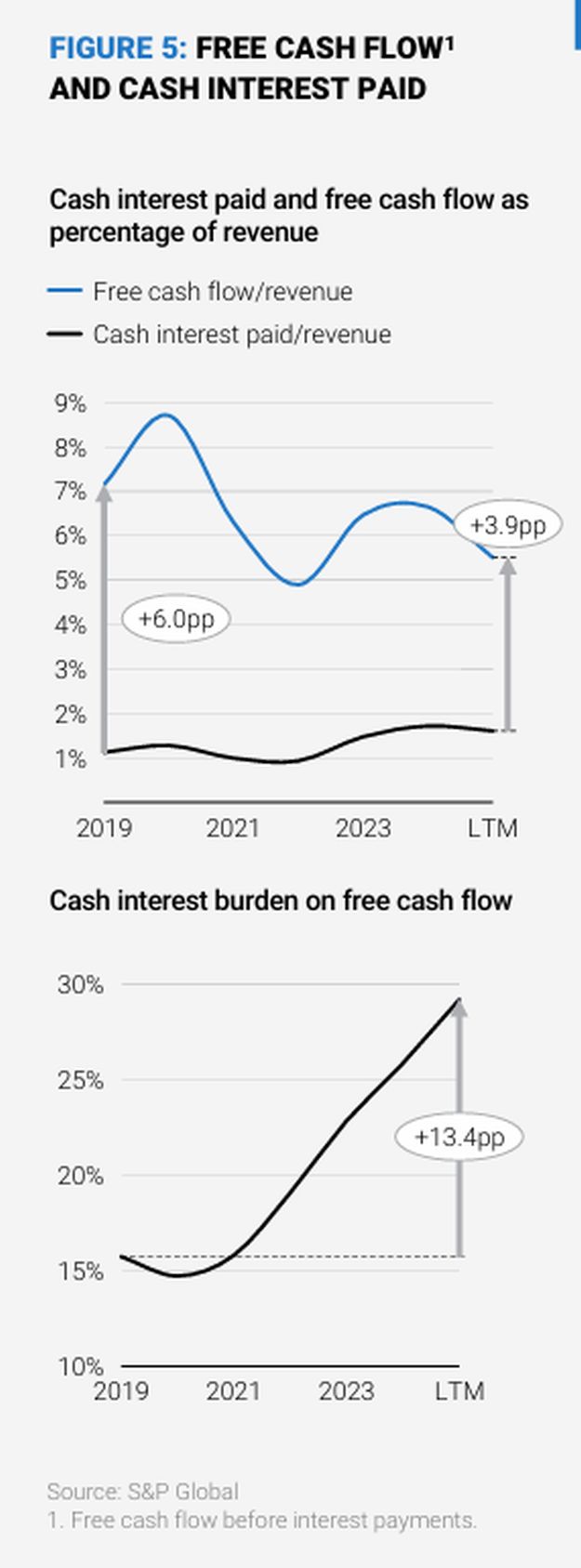

The financing cost trajectory makes stagnation in free cash flow far more significant. Cash interest paid has risen approximately 86% since 2019. The mismatch is stark and worsening. The cash interest burden on free cash flow has nearly doubled from about 15% of free cash flow in 2019 to almost 30% today (see Figure 5). In other words, a large portion of free cash flow is now absorbed by interest payments before any strategic capital allocation decision can be made. For companies in this position, flat free cash flows are not a neutral outcome. It is a compounding problem, because every refinancing cycle today—which replaces cheap debt raised when financing costs were a lot lower—is for much more expensive capital.

The picture that emerges is one of earnings resilience masking genuine cash flow stress. Revenue and EBITDA numbers tell a story of a DACH region that has managed well. The free cash flow and interest burden numbers tell a different story. Shareholders, boards, and management teams risk missing the size of the challenge. In a refinancing environment that scrutinizes cash generation above all else, EBITDA growth that does not translate into free cash flow will offer limited protection when lenders begin asking tougher questions.

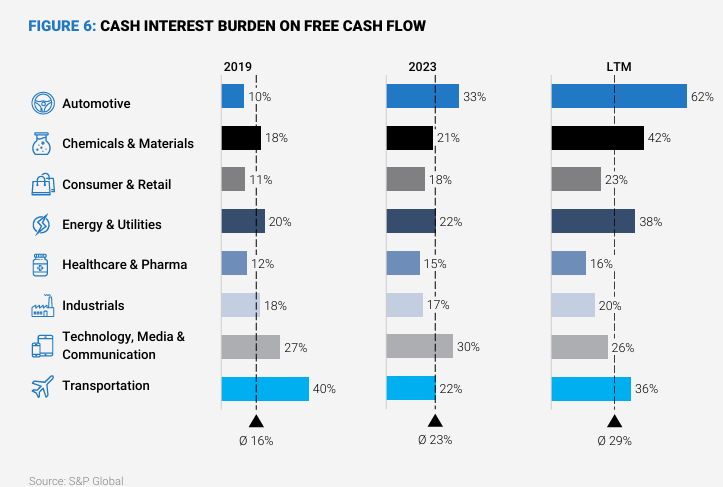

Inflated financial debt positions as an aftereffect of the COVID period further exacerbate this dynamic. While the aggregate picture across all companies in DACH is already striking, some industries are performing far worse than others.

Industry crises intensify

Many DACH companies are facing pressure from structurally low demand and downturn in industrial cycle, while high energy costs remain a local disadvantage. In addition, both the Chinese market and Chinese competitors are disrupting established business models, and China related challenges remain persistent for exporters. At the same time, geopolitical uncertainties, including renewed U.S. trade and tariff shocks, as well as the situation in the Middle East, add another layer of volatility. Together, these factors weigh on financial health by compressing margins, reducing cash generation and slowing deleveraging, leaving leverage metrics weaker and financial buffers thinner. In practice, this translates into refinancing challenges: higher all-in financing costs versus prior years, more limited tenor, stricter covenants, and greater dependence on timing and market access, especially for weaker credits or sectors under structural pressure. The pressure is particularly acute in Automotive, in Chemicals & Materials and in Energy & Utilities as the analysis below shows.

The result is a tightening “interest coverage” dynamic: even where operating performance remains stable, financing costs absorb a growing share of cash generation, leaving less headroom for investment, deleveraging, or shareholder returns.

To view the full article, click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]