- with readers working within the Advertising & Public Relations and Aerospace & Defence industries

Overview

The apparel industry has navigated plenty of advancements and disruptions — fast fashion, e-commerce, the COVID-19 pandemic-era athleisure boom. But GIP and GLP-1 medications (collectively, “GLP-1”) represent something categorically different: a biological shift in the American body, happening at scale, faster than the industry’s planning and size-curve systems were designed to accommodate.

For the first time in decades, the obesity rate in the U.S. has declined, dropping from a peak of 39.9% in 2022 to 37% in 2025. Typical weight loss of 10%-20% of body weight equates to one-to-five clothing sizes (Bernstein, 2026). The implication is not a minor recalibration of size curves. It is a structural reset of the demand landscape.

What is accelerating adoption faster than most brands have modeled is the rapid expansion of access. GLP-1 medications were historically limited to diabetic patients, keeping the covered user base narrow. That is now changing on multiple fronts simultaneously:

- In 2021, at the height of the pandemic, Wegovy received the first weight loss indication from the FDA expanding the covered base of semaglutide users beyond Type II diabetic patients.

- Oral Wegovy launched in January 2026 with a temporary offer at $149-$299/ month for qualifying patients, removing the “needle fright” barrier with a pill form replacement. Eli Lilly followed soon after with Foundayo in April 2026, with prices starting around $149/month for cash-pay customers.

- Beginning in February 2026, several GLP-1 drugs became available through the direct-to-patient channel advertised via TrumpRx, potentially further reducing access barriers.

- From July 1 to December 31, 2026, the CMS “Medicare GLP-1 Bridge” program will provide coverage for Wegovy for weight loss with a $50 monthly copayment, aimed at eligible Medicare Part D beneficiaries.

- FDA approvals for new indications — obstructive sleep apnea (Zepbound in December 2024), cardiovascular disease (Wegovy in March 2024, Rybelsus oral pill in October 2025), and weight-related comorbidities— mean a far broader set of patients’ insurance may now cover prescriptions.

The demographic profile of GLP-1 users has undergone a fundamental shift. No longer confined to those with Type 2 diabetes or the ultra-wealthy paying out-of-pocket, these treatments have entered the mainstream “commercial” workforce.

In 2026, according to a study by the American Academy of Procedural Medicine (AAOPM) roughly 45% to 48% of large employers now include anti-obesity medications in their health plans—nearly doubling the coverage rates seen in 2023. This expansion, coupled with the introduction of direct-to-consumer “self-pay” tiers as low as $299/month, has bridged the gap between the low-income (Medicaid) and high-income populations, potentially making these drugs a staple of middle-class healthcare. The demographic change may also spill into their wardrobes.

KEY FACTS

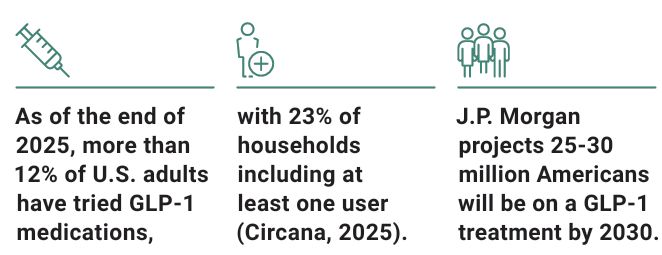

Over 12% of U.S. adults have tried GLP-1 medication (Gallup, 2025).

80% of GLP-1 users anticipate needing new clothing due to size changes (Circana, 2025).

Sizing Is the New Fault Line

Apparel brands have historically adjusted their size curves once a year — a rhythm built around slow-moving demographic trends. GLP-1 adoption is rendering that cadence obsolete. Industry analysts note that brands are now revising size mix models more often than they have before. The classic 1-2-2-1 ordering ratio (one part S-two parts M-two parts L-one part XL) is giving way to a 2-2-1-1 model. Brands that clung to their legacy ratios through 2024 are now facing the compounding pressure of overstocked large sizes and shortages of small sizes. Circana’s September 2025 data confirms the shift is now national, with larger bra band sizes (over 42) and D cups losing market share to smaller sizes — intimate apparel is emerging as a leading indicator for broader assortment categories.

“Overstock in large sizes and stockouts in small sizes. Brands that do not update their size curves might pay for it in both directions.”

The financial consequences are already in earnings reports. A leading men’s plus-size retailer reported a 6% year-over-year (YoY) sales decline and $29.6 million net loss in Q4 2025, attributing pressure to GLP-1 usage among approximately 25% of its customer base. A major women’s plus-size retailer reported a 14% Q4 sales drop and closed 151 stores throughout 2025. One important nuance: Height does not change with weight loss. Tall women losing two or three sizes still need the same inseam and sleeve length — creating an underserved small-but-tall segment that most assortments do not yet accommodate.

A Potential Margin Uptick Tailwind

The size shift is not just a demand story — it is a margin story. Fabric usage increases approximately 4%-5% per size step, and fabric represents 50%-70% of garment production cost. Since virtually all mainstream brands hold retail prices constant across sizes, every consumer sizing down reduces cost of goods sold (COGS) while revenue stays flat.

A one-step average size shift across a brand’s mix reduces total COGS by 2.4%-3.5% — flowing directly to gross profit. For a $500 million COGS brand, which is $12-$17.5 million in annual margin expansion, moving operating profit by 100-200 basis points, without changing a single retail price. In an industry averaging 10%-15% net margins, a sustained 1%-2% COGS tailwind represents a 7%-20% improvement in bottom-line profitability. This is a structural edge hiding in plain sight for brands that plan ahead.

“A single size step down could add $12-$17.5 million to your bottom line — without changing a single price tag”

Who Is Winning

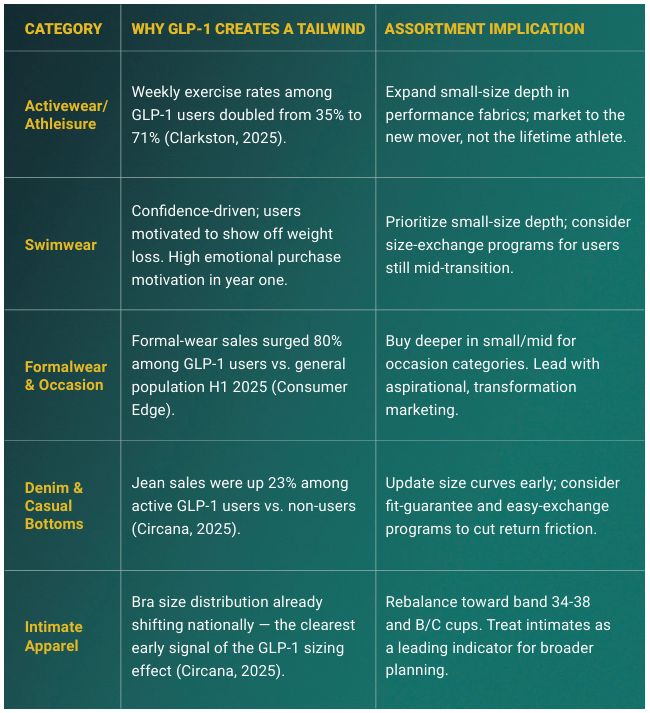

The opportunity is not evenly distributed. GLP-1 users carry larger apparel baskets for one to three years as they overhaul their wardrobes, and 50% report shopping more often since starting the drugs. The categories best positioned to capture that spend:

What To Watch

Access Acceleration

Lower price tiers for D2C self-pay, oral GLP-1 pills (which Medicare is purchasing at $245/month through a demonstration program and the BALANCE model), and telehealth platforms growing 59% YoY are simultaneously collapsing cost and friction barriers. Research analysts at JP Morgan estimate that roughly 25 million Americans will be on a GLP-1 by 2030, up from 5 million in 2023. Brands planning 12-18 months ahead must model the 2027 consumer, not who their customer was in 2025 (CNBC, 2026)

Inclusive Sizing: Do Not Overcorrect

68%-72% of American women wear plus sizes, yet plus-size clothing is only 12%-18% of apparel revenue — chronically undersupplied before GLP-1. Pulling back aggressively risks alienating a still large segment. The answer is a more dynamic size curve, not a retreat from extended sizing.

The Returns Spiral

Consumers cycling through two to three sizes in 12-18 months buy multiple sizes and return what does not fit. Simultaneously, brands are sitting on growing large-size overstock while stocking out in small. Retailers without dynamic assortment planning face both problems at once.

Clear and Informative Sizing Communication

Consumers who have bought the same size for years may suddenly find themselves less certain about what fits. As bodies shift mid-cycle, clear fit guides, detailed size charts, and diverse model representation can go a long way toward reducing friction at the point of purchase.

The Feel-Good Wardrobe Refresh

For many GLP-1 users, meaningful weight loss may prompt an entirely new wardrobe — not just everyday basics, but body-contouring categories like swimwear, intimates, and underwear that need to fit precisely to feel right.

The Strategic Imperative

The brands that win in this environment will not be those that react fast to today’s size data, they will be those that build planning systems sophisticated enough to anticipate where demand is heading. GLP-1 adoption is not slowing down, and the structural forces it has set in motion — shifting size curves, rising returns, identity-driven purchasing, and the athleisure surge — are compounding.

“The question for every apparel executive is no longer whether GLP-1 will affect their business. It already is. The question is whether their assortment strategy reflects it.”

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]