- within Cannabis & Hemp topic(s)

- in Europe

As part of its work on online pricing claims, the CMA has issued guidance for traders when selling optional extras (like insurance or faster delivery). This is alongside its price transparency guidance, which, among other things, covers mandatory extras.

The key takeaway is you must not charge customers for optional extras, unless the consumer has expressly agreed to it. This requirement isn't new — it is set out in the Consumer Contracts (Information, Cancellation and Additional Charges) Regulations 2013.

Getting express consent

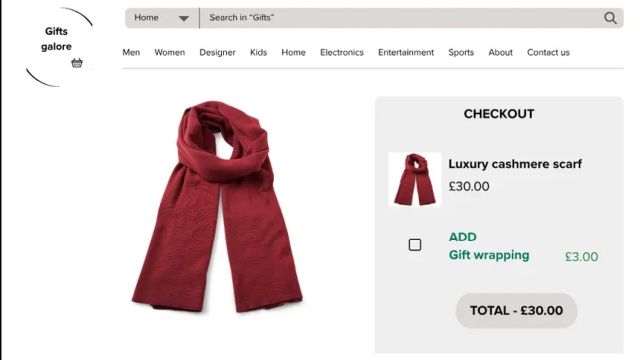

If you are offering optional extras linked to the main product you are selling, you should not charge for those extras by default.

Consumers must have genuine choice over whether to pay for an extra product or service they may or may not wish to choose. You can't use pre-ticked boxes or other forms of automatic opt-in for optional extras, if that means the customer will have to pay for them unless they take action to opt out.

Optional extras can include things like insurance, express delivery or making donations to charity.

You need to get your customer's express consent for any additional payment – they must actively choose to make the payment.

Businesses must:

- clearly explain any additional payments that consumers can choose to make

- make sure that customers expressly consent to additional payments before they are charged

- give customers a way to check and confirm what they are paying for

The CMA makes clear that a customer can't provide express consent by not changing a default option, for example by not removing a tick from a pre-ticked box; or opting out of an extra, for example if they are required to tick a box to avoid paying.

The guidance includes various useful examples of what is and what isn't allowed.

Customers' rights

If a customer does not expressly agree to an additional payment, they do not have to pay it.

Refunds

If a customer did not give express consent to pay an additional charge, then they may claim a refund from the trader.

As we mentioned in our webinar on pricing claims last week, this is an easy area for the CMA to enforce – as the CMA can locate pre-ticked boxes for optional extras in an online customer journey without requiring any information from the business. The CCRs say that traders should reimburse consumers for such payments, which makes this type of case an attractive option for the CMA to require redress. Therefore, we strongly advise that you check your websites and make sure that you are not pre-ticking boxes.

We have lots of information on our Consumer Law Hub, which we are constantly updating. If you need help, or you would like a recording of the webinar, please contact a member of the team.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.