- with Finance and Tax Executives

- with readers working within the Accounting & Consultancy, Business & Consumer Services and Construction & Engineering industries

Overview

Since 28 February 2026 when U.S. and Israeli strikes on Iran triggered the closure of the Strait of Hormuz, African economies have absorbed a multi-dimensional economic shock from the disruption of energy supply, food systems, export corridors and financial conditions.

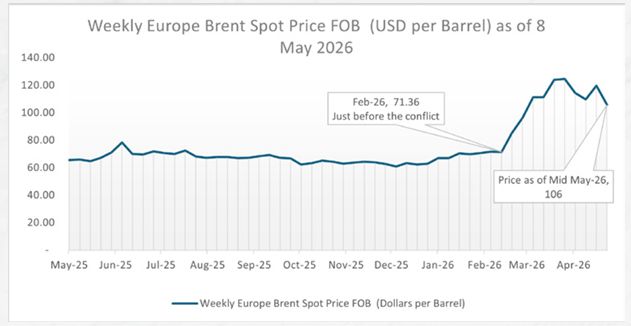

Brent Crude prices moved above USD 100 in mid-March for the first time since 2022, hitting USD 115 by the final week of March. A short-lived ceasefire announcement in early April knocked prices back to just above USD 110 by end-April, more than 50% above where it started the year. May has brought a modest retreat, with price easing at USD 105 as of the 8 May. Source U.S. Energy Information Administration

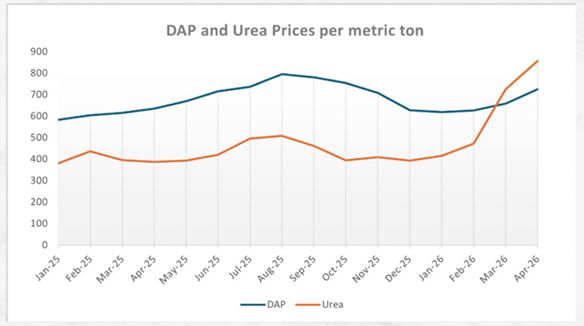

On a monthly basis, prices in March 2026 reached their highest level since 2022. The recent surge in the index largely reflects the impact on exports of fertilizers and inputs from the closure of the Strait of Hormuz. Price increases have been most pronounced for urea, with more moderate gains for other fertilizer types. World Bank Commodity Markets Outlook

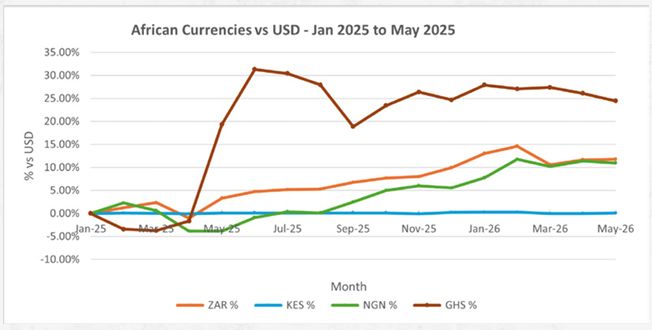

Major African currencies saw good performance in the first quarter of the year, with the fuel shocks resulting in marginal decreases in February and March before stabilizing in April and May of 2026. Source CBK, BOG, CBN and SARB.

The Shocks

There are three major transmission channels that have the most impact for African economies: Energy, fertilizer and logistics.

The energy channel is the most visible. Brent Crude Oil rose from USD 81 per barrel before the start of the conflict to a high of USD 122 by start of April 2026, before settling to just above USD 100 per barrel, once a cease fire was announced. For net importers, where energy and transport carry 15-25% weight in Consumer Price Index (CPI) baskets, the pass-through is mechanical. Kenya, Nigeria, Tanzania, Ghana, and South Africa have all seen pump prices rise 15-30% since late February. Electricity generation costs are expected to rise for systems that rely on thermal power plants.

Oil-producing economies sit in a paradoxical position. Nigeria, Angola, Algeria, Gabon, Congo, and Equatorial Guinea gain revenue from crude prices hovering above $100, but most remain net importers of refined products, so domestic pump prices are still expected to rise. The group with durable strategic upside is the energy producers such as Nigeria via Dangote Refinery and, Algeria and Mozambique via LNG, which can step into gaps left by Gulf producers, and that is where the lasting opportunity lie.

The fertilizer channel is being underweighted, and it is the one we are most concerned about. Gulf countries supply approximately 35% of global urea, 53% of sulphur, and 64% of ammonia. Hormuz dry bulk traffic collapsed by 83% between February and March according to AXS Marine. The timing is what makes this dangerous as the period between March and May is the primary planting season across East and Southern Africa, and fertilizer accounts for 35-50% of grain production costs. Yield drops of 20-30% on maize, wheat, and rice are now plausible for Kenya, Ethiopia, Tanzania, Mozambique, Sudan, and Somalia. The resulting food-price shock would land in Q3 2026 with a three-to-four-month lag, precisely when energy prices might start to ease.

The logistics channel completes the picture. With Hormuz and Bab al-Mandab both effectively closed, the Cape of Good Hope is now the default corridor for Europe-Asia freight. Cape Town and Durban have already seen a significant rise in container arrivals. However, port inefficiencies and infrastructure limitations will hinder full monetization of the increased volumes of shipping.

The second-order effects are already visible. The dollar has strengthened as investors moved to safety, and African currencies have weakened. Kenya's Central Bank spent $941 million, nearly 7% of total reserves, defending the shilling in a single month. Bond yields in Kenya and South Africa rose within weeks of the shock. The IMF has cut its 2026 African growth forecast from 4.5% to 4.2%, while the World Bank's Sub-Saharan Africa projection is now 4.1%. Regional inflation will likely land at 4.8%, up from 3.7% in 2025.

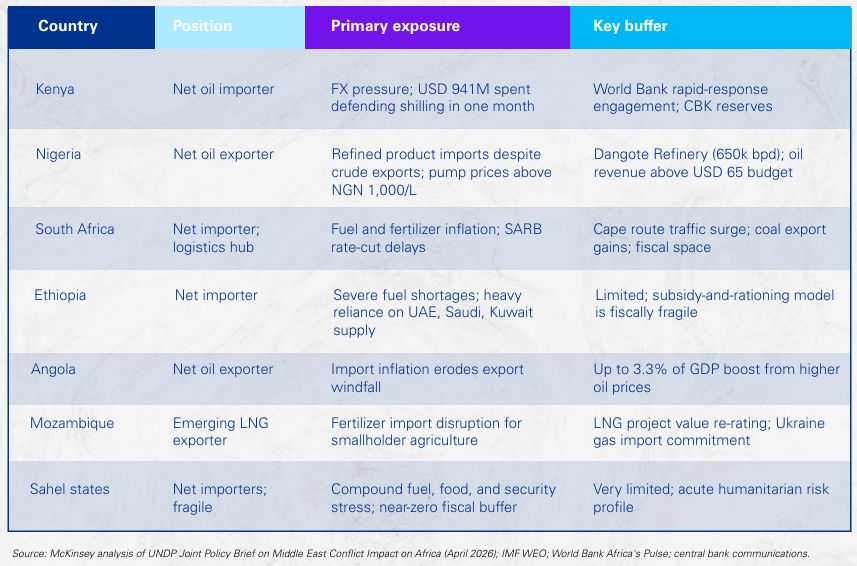

Country exposure matrix: position, primary risk, and available buffer

What it means for businesses?

Supply chains have been severely distorted, with inventory lead-times needing to be revised from the assumptions made in 2024/2025. Just in time supply chain models need to be hedged, especially for clients sourcing capital equipment, pharmaceuticals, or specialized chemical inputs from the Gulf or East Asia. Insurance premiums for freight must be renegotiated and passed on to the final consumers by increasing final prices.

The aviation industry in Africa is in acute stress, with African airlines being geographically intertwined with the Middle East through migration corridors, labour traffic, and global transit routes. The continent’s largest airline, Ethiopian Airlines, lost approximately USD 137 million within the first few weeks of the conflict after having to cancel over 100 flights per week the airline has been operating in the Middle East.

The opportunity

Four openings provide real potential, and they have timelines short enough to act on.

Downstream investment, anchored on the Dangote case

Dangote Refinery is running at or near its 650,000 barrels per day capacity. Exports to African markets rose from roughly 38,000 to above 200,000 barrels per day between February and March 2026, reaching Côte d'Ivoire, Cameroon, Tanzania, Togo, and beyond. Ghana's President Mahama is pursuing a formal supply agreement. Nigerian National Petroleum Company Limited (NNPC) has increased crude allocations to stabilize the refinery's feed. The real-time demonstration is that downstream capacity is a continental strategic asset, not just a Nigerian national one. The investment thesis for greenfield refineries in Angola, Mozambique, Tanzania, and Uganda has strengthened materially, as has the thesis for modular refinery clusters serving the Sahel and landlocked East Africa.

African Liquefied Natural Gas (LNG) as a replacement, not a bridge

Qatar Energy's repair timeline for damaged LNG infrastructure is expected within three to five years. Algeria has agreed to raise LNG exports to Spain while Ukraine has committed to increasing gas imports from Mozambique. Sub-Saharan LNG exports are projected to grow 175% by 2034, from 30.9 to 44.5 billion cubic metres. Mozambique's previously stalled projects, TotalEnergies' Area 1 in particular, have a materially different investment case today than they did six months ago. For African LNG developers, the question is no longer whether demand will exist, but whether capacity can be built fast enough to lock in contracts before Qatari volumes return.

Renewable acceleration, driven by security rather than climate

At CERAWeek in March, energy executives argued explicitly that energy security anxieties are accelerating, rather than slowing, the renewable shift. Masdar's $10 billion Africa renewable program appears to be holding. The African Private Capital Association is tracking capital flows toward businesses less dependent on raw material imports. Countries with strong domestic resource endowments, notably Kenya on geothermal, South Africa, Tanzania, and Morocco, now have a hard energy-security rationale attached to the climate case for renewable scale-up. Solar, wind, geothermal, and battery storage produce energy from local, untradeable resources, and that fact alone reframes the investment thesis.

AfCFTA as crisis infrastructure, not trade agreement

During the Russia-Ukraine shock, intra-African fertilizer trade rose to 39% of the continent's fertilizer imports, absorbing an 8% drop in Russian and Ukrainian supply. That is a real-world demonstration, and the opportunity now is to operationalize the same channel for urea: North African producers, Morocco's OCP in particular, plus Algeria and Egypt, can serve Sub-Saharan markets under AfCFTA preferential tariffs faster than Gulf suppliers can resume. PAPSS, now in force since 2025, settles these flows in local currencies and reduces the dollar amplification that has made this shock worse. The EU-AfCFTA MoU signed April 20, backed by €1.2 billion of Team Europe financing, provides the capital to build the corridor infrastructure (ports, cold chains, one-stop border posts) that converts signed protocols into real trade flows.

For African LNG developers, the question is no longer whether demand will exist, but whether capacity can be built fast enough to lock in contracts before Qatari volumes return.

Our recommendations

Four openings provide real potential, and they have timelines short enough to act on.

Sovereigns and central banks

African Central Banks need to engage multilateral emergency facilities now, before market conditions tighten further. Kenya's approach is the most prudent template - pausing rate-easing cycles but avoiding aggressive tightening, being cognizant that this shock is supply-driven and temporary, and that the credibility is the currency that matters most. They could also replace universal fuel subsidies with targeted cash transfers and VAT reductions as universal subsidies may not survive a six-month shock fiscally, as Ethiopia's position might soon demonstrate. There is also a need to build 30-day strategic petroleum reserves through regional pooling under ECOWAS, EAC, and SADC and to operationalize pooled procurement for urea and diesel immediately.

Development finance institutions and sovereign wealth funds

DFIs should redirect capital toward downstream energy infrastructure (refining, LNG export, power pool integration) and fertilizer production in North Africa. Gulf sovereign funds are reviewing African commitments, which means capital slots are opening for African and European institutional money. African pension funds and sovereign wealth funds collectively manage over $1 trillion and even 5% redirected toward continental infrastructure would exceed the capital at risk from Gulf retrenchment. Green bonds and blended finance instruments for solar and wind are expected to be more attractive today than at any previous point.

African corporates

Manufacturers and logistics operators may need to hedge against rising fuel costs, while reassessing dollar-denominated liabilities under a sustained oil-price environment above $100 per barrel. At the same time, they should strengthen liquidity buffers and extend working capital cycles to maintain operational.

There is need to accelerate on-site solar and storage investment, as the shocks expose resilience as well as sustainability. Agribusinesses should secure fertilizer contracts with OCP Morocco, Yara, and Eurochem before the 2026-27 planting season. Logistics operators along the Southern and Eastern African coasts should invest in port capacity, bunkering, and transshipment as the Cape route traffic is likely to persist beyond the current conflict.

Multinationals operating in Africa

The exposure map has changed. Supply chains built on stable Gulf petroleum flows need re-evaluation and restructuring. Regional sourcing under AfCFTA is now a risk-mitigation tool, not an ESG story. Procurement strategies should factor in a persistent 10-15% premium on Hormuz-routed goods for at least the next 18 months and should reassess which African markets can absorb that premium versus which will require localized sourcing to remain viable.

Fiscal and Tax Responses to Oil Price Shocks

African governments can deploy a mix of short-term stabilisation taxes and medium-term revenue rebalancing measures. In the short term, they may use fuel tax smoothing by temporarily reducing excise duties or road levies to prevent sudden spikes in retail fuel prices, although this approach can be fiscally costly.

They may also introduce targeted fuel subsidies focused on public transport, agriculture, and essential logistics, while avoiding broad-based subsidies that are financially unsustainable. In some cases, governments may implement windfall taxes on energy producers to capture excess profits when global oil prices surge, helping to stabilise fiscal positions, particularly in resource-exporting countries.

On the revenue side, governments can carefully adjust indirect taxes, such as broad-based VAT reforms or excise increases on luxury and non-essential goods, though these measures carry the risk of adding to inflation if poorly designed. Additionally, import duty rationalisation can be used by reducing tariffs on critical goods like fuel, fertilisers, and essential commodities while maintaining or increasing duties on non-essential imports to protect fiscal revenues and support economic stability.

On Africa Continental Free Trade Area

The conflict in the Persian Gulf exposes Africa’s extreme dependence on external shipping routes that are controlled by actors that are indifferent to African interests. Further, the slowing of shipping and increased insurance premiums continue to hit African importers hardest. With intra-Africa trade still being relatively low at between 14-16% of total African trade, economies currently have limited domestic and regional alternatives to supply shocks.

Scaling up intra-African trade becomes urgent and prudent as it creates redundancy. While not a silver bullet, the AfCFTA provides a marginal solution to external volatility through import substitution and regional value chains. It presents an opportunity to accelerate the conversation about Africa’s resilience, energy sovereignty, refining capacity, and renewable energy investment in the long run. For the short term, activation of contingency import financing, pooled fuel procurement, emergency food corridors, and diversified fertilizer sourcing should be a priority that could leverage on AfCFTA frameworks. This shock-buffering potential of AfCFTA was demonstrated by the rise in intra-Africa fertilizer imports when imports from Russia and Ukraine fell over 8%.

Hurdles do exist. Rules of origin on key sectors, including automotive, pharmaceuticals, and agriculture, remain unfinished while the infrastructure gap is estimated at $120 billion in transport equipment alone by 2030. The correct framing is that AfCFTA is a medium-term structural insurance policy being paid for today and every year Africa does not act, the externality costs compound. Every shock that hits before implementation accelerates matters more to welfare than the last. The Iran shock should push the timelines forward by two to three years particularly across fertilizer, energy, and logistics corridors. This heavily depends on African governments, and not on the agreement itself.

A closing observation

Africa has faced similar shocks before since the crisis in 1973, and each time produced the same policy papers recommending the same things. Little changed because the tools we have now didn't exist. Dangote is refining at 650,000 barrels per day. PAPSS is settling cross-border transactions in local currencies, cutting the dollar dependency that makes every external shock more expensive. AfCFTA has binding tariff schedules across 24 state parties. The infrastructure is live. The window is the next two quarters, while Gulf supply is disrupted and the pressure to act is real. Once supply chains normalize and fuel prices ease, the urgency dissipates and the tools go back to sitting on a shelf. Decision makers who wait for the pressure to pass will have missed the only moment that changes behaviour.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.