- within Finance and Banking topic(s)

- in Ireland

- with readers working within the Securities & Investment and Law Firm industries

- within Strategy, Antitrust/Competition Law and Insolvency/Bankruptcy/Re-Structuring topic(s)

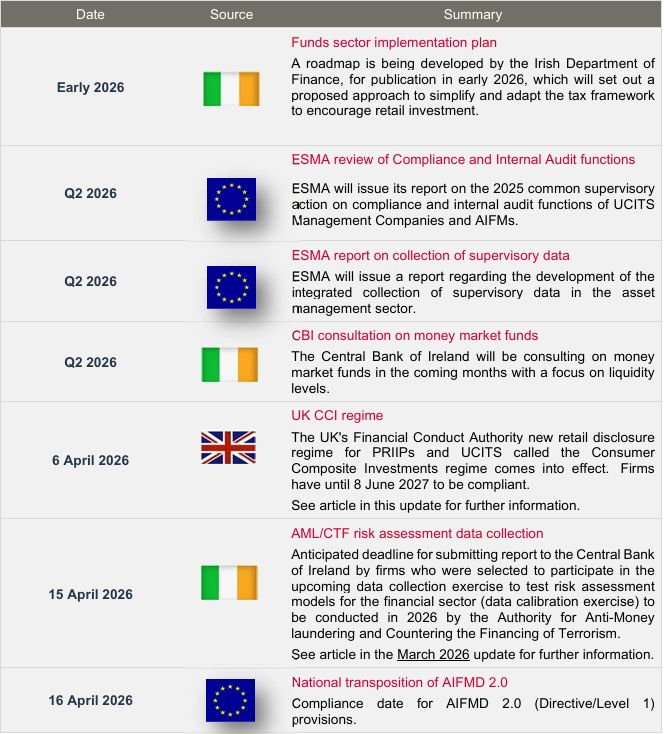

Key Dates & Deadlines: Q2 2026

The following are key dates and deadlines in Q2 2026 and some key forthcoming dates in the legal and regulatory calendar

Central Bank of Ireland fund authorisation workshop

A fund authorisation workshop between industry representatives and the Central Bank of Ireland (CBI) took place on 24 March 2026. The session offered a detailed walkthrough of the fund authorisation process and explored practical opportunities to enhance efficiency in line with the ongoing simplification agenda at both domestic and EU levels. Industry had the opportunity to underline the drivers and factors involved in delivering a successful fund product to market in timely manner.

Discussion points

The workshop covered a wide range of fund authorisation issues such as current trends in volume of applications, how applications are prioritised, the review process, fast-track and clone applications, expectations around disclosure quality and transparency, making material changes to fund products mid-filing, novel products and asset classes and pre-submission engagement. There was significant discussion on expectations for SFDR disclosures. The post-authorisation process was also discussed.

Central Bank system upgrade

Central Bank system upgrade The CBI will be updating its system that processes fund authorisations, with an expected date of implementation in 2027. Solutions are under development to address existing limitations and improve overall process efficiency.

Central Bank of Ireland tokenisation discussion paper

The CBI issued its Discussion Paper 12 on Distributed Ledger Technology (DLT) & Tokenisation in financial services (DP12) on 5 March 2026. The CBI highlights the benefits and opportunities DLT and tokenisation presents for financial services, identifies key enablers to leverage such benefits and sets out potential risks and challenges associated with such innovative technologies. There is a specific section in DP12 considering issues for investment funds and tokenisation.

What is DLT and tokenisation?

DLT is a technology that achieves a single, shared ‘source of truth’ through a common ledger, aiming to replace multiple independent ledgers with a synchronised digital record. DLT nodes are independent computer servers that join and maintain the shared ledger based on the common rules of the network.

In the context of DP12, tokenisation refers to the issuance or representation of assets in the form of digital tokens, using technology such as DLT. Tokens can take the form of “digitally native” tokens issued directly on a DLT or “non-native” tokens that are digital representations of assets originally issued elsewhere.

What does the discussion paper cover?

DP12 covers the benefits of tokenisation, the risks associated with DLT and tokenisation and how to enable tokenisation.

Tokenisation in Funds

Ireland is a leading EU domicile for funds, particularly money market funds (MMFs) and exchange-traded funds (ETFs). Tokenisation presents a transformative opportunity for such funds.

Tokenisation may allow certain elements of workflows in a fund, such as subscriptions, redemptions, transfers and corporate actions, to be automated through programmable rules embedded in tokenised fund units. However, tokenisation does not alter the need for independent valuation, liquidity management, depositary oversight and investor disclosure obligations. DP12 focuses, in particular, on the application of liquidity management tools in a tokenised environment.

Initial use cases for Irish authorised funds have tended to focus on the digital representation of an investor’s holding in the form of a token, typically using a digital twin model.

DP12 sets out 4 illustrative potential use cases for MMFs and ETFs.

Next steps

The CBI has requested written responses from stakeholders to the queries raised by the CBI in DP12 to be submitted no later than 5 June 2026. The CBI will publish a feedback statement and will also assess whether existing policy and regulatory approaches are fit for purpose to enable the realisation of the benefits, and management of the risks relating to, the integration of tokenisation and DLT in financial services.

A new UK KIID: the FCA's CCI regime

The UK's Financial Conduct Authority (FCA) published a policy statement on 8 December 2025 on the UK's new retail disclosure regime for PRIIPs and UCITS called the Consumer Composite Investments (CCI) regime. The CCI regime came into effect on 6 April 2026. Firms have until 8 June 2027 to be compliant.

Firms selling into the UK will need to digest the requirements and determine what extension of their current product approval processes will be required in order to ensure their products can be sold to UK retail investors in compliance with the CCI regime.

The CCI regime applies to any firm that manufactures or distributes a CCI to UK retail investors. The FCA has confirmed that the scope of the CCI regime is not intended to extend beyond the perimeter established by the current UK PRIIPs and UCITS regimes.

Summary should be a stand-alone, consumer-friendly document about the CCI, made available to distributors. The Product Summary must include information relating to:

- costs and charges;

- risk and return;

- past performance; and

- general product information.

Distributors are also subject to a range of new key obligations under the CCI regime.

CBI findings on outsourcing risk for administrators and depositaries

The CBI has issued a letter setting out its findings following its Thematic Inspection of Outsourcing Risk on Fund Administrators and Depositaries (FSPs).

While outsourcing can deliver efficiencies, an overreliance on external providers can dilute local management’s control over key activities. Risks are heightened in the absence of effective oversight and control of outsourced activities and/or deficiencies in outsourcing governance and risk controls. Robust due diligence, governance and ongoing oversight are essential to manage concentration, dependency and conduct risks. A less than robust outsourcing oversight framework also exposes FSPs to the risk that they are not fulfilling their regulatory obligations.

Thematic inspection overview

The inspection assessed the outsourcing oversight frameworks established by FSPs taking into consideration the good practices for the effective management of outsourcing risk, as outlined within the CBI’s Cross-Industry Guidance on Outsourcing. For Fund Administrators, the inspection also considered the Outsourcing Regulations set out in Part 4 Chapter 2 of the Investment Firms Regulations 2023 and the CBI’s related guidance.

The letter sets out what the CBI considers good practices by a FSP in the establishment and maintenance of a robust outsourcing oversight framework including:

- Establishment of outsourcing forums / committees.

- Dedicated Outsourcing Manager.

- Clear role for second line of defence.

- Defined internal outsourcing risk appetite limits.

- Multi-layered outsourcing risk metrics.

- Due diligence and risk assessments periodically and on a proportional basis.

- Specific tailored outsourcing oversight documentation such as an Outsourcing Oversight Framework, Outsourcing Policy.

- Prime Brokers in Depositary outsourcing registers.

- Strong and senior-led NAV oversight controls at Administrators.

ESMA report on simplifying the retail investor journey

ESMA has released a report following a call for evidence with the purpose of gathering input from stakeholders on key aspects of the retail investor journey. It focuses on the MiFID II regulatory requirements that impact retail investors when engaging with capital markets. ESMA sought to assess whether these requirements effectively support investor protection while also ensuring accessibility and ease of engagement. Non regulatory barriers – such as lack of trust, high fees, lack of comparability, lack of financial literacy and risk aversion - to retail investor participation were also examined.

The outcome from this workstream is likely to ultimately feed into work underway at European level on the Retail Investment Strategy.

Executive summary

Taking into account the input from stakeholders, ESMA outlines a number of actions and operational improvements it will take forward to make it easier for retail investors to access suitable investment opportunities.

ESMA will focus on three areas:

- streamlining disclosure requirements and tackling information overload for investors;

- reducing complexity in suitability and appropriateness assessments;

- simplifying MiFID II requirements on sustainability preferences.

ESMA will also strengthen monitoring and oversight of emerging (social) media channels and affiliate marketing models (including influencers). As part of this follow up work, consumer testing will be used to inform and validate improvements to disclosures and digital investor journeys, including for mobile-first users.

Updating ESMA guidelines and other legislative guidance will be undertaken once the legislative process on the Retail Investment Strategy is concluded.

Central Bank of Ireland research on Irish households' investment in investment funds

The CBI released a report in April 2026 focused on investment fund holdings by Irish households. It also looked through those investment funds holdings to the underlying assets. The report is timely in light of the current focus of European and Irish policymakers and regulators on retail investors and their participation in capital markets.

Financial market participation

Irish households’ participation in financial markets has increased in recent years however it remains modest by international standards, despite relatively high saving rates. Policy efforts to increase retail participation in capital markets are intensifying, with discussions around fiscal reforms in Ireland and potential tax-incentivised investment schemes. These measures could help redirect household savings away from bank deposits and towards the financial markets.

Investment fund holdings

As of Q3 2025, total financial assets of Irish households stood at €589bn, with the largest share of this held in insurance and pension entitlements (46 per cent), and currency and deposits (37 per cent). Irish households’ holdings of investment fund shares were €11.2bn in Q3 2025. At 2 per cent, the share of investment funds in total financial assets of households in Ireland is well below the euro area average of 11.1 per cent. Irish households mainly invest in investment funds domiciled in the main European financial centres of Luxembourg and Ireland.

Ireland's Savings and Investment Forum

On 31 March 2026, the first annual Savings and Investment Forum was held in collaboration with the CBI and Irish Department of Finance.

Funds sector 2030 report

In alignment with the key recommendations of the Funds Sector 2030 report, this forum was established to bring together policymakers, industry and consumer stakeholders with a focus on the development of a framework for a Personal Investment Account in Ireland designed to support greater public engagement with saving and investing.

The aim is to legislate for the framework in 2026 and to allow accounts to be offered from 2027.

Taxation of retail investment in Ireland

The framework will also be a key part of a broader rethink of the taxation of retail investment.

As part of Budget 2026, the Government already reduced the tax rate on investments in funds and life assurance policies from 41% to 38%. Further work on a retail investment tax roadmap is ongoing and will be published in the coming months.

The roadmap will set out an approach to simplify and adapt the tax framework to further support retail investment, while retaining proportionate necessary and important anti-avoidance protections.

The recommendations of the Funds Sector 2030 report, including in relation to deemed disposal, are now being worked on as part of the development of the roadmap, as well as the European Commission’s recommendation on Savings and Investment Accounts.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]