- within Tax topic(s)

- with readers working within the Banking & Credit industries

- with readers working within the Securities & Investment industries

- within Government, Public Sector and Energy and Natural Resources topic(s)

AT A GLANCE

BACKGROUND

- Safe Harbour Rules ('SHR') were first introduced in Indian Transfer Pricing ('TP') regime by the Central Board of Direct Taxes ('CBDT') in September 2013 under Section 92CB of the Income-tax Act, 1961 ('the Act'). Designed as a litigation-reduction mechanism, SHRs allow tax authorities to accept a taxpayer's declared transfer price for specified international transactions without detailed scrutiny, provided predefined conditions are satisfied.

- Over successive years, the CBDT had been extending the applicability of SHRs on a year-by-year basis, an approach that created compliance uncertainty for multinational enterprises ('MNEs') operating in India. Further, in general taxpayers have found the safe harbour margins to be on a higher side.

- In her recent budget speech, the Hon'ble Finance Minister announced a comprehensive overhaul of the SHR framework, particularly for Information Technology ('IT') services. Pursuant to this, the CBDT released the Draft Income Tax Rules, 2026 for public consultation, which contains the revised SHR provisions under Rules 86 to 93.

- Key updates include an extension of safe harbour period, consolidation of various services into a single category of IT Services, expansion of threshold, introduction of new safe harbour for data center services and an automated rule-based process for IT services safe harbour. SHRs for non-IT transactions remain unchanged from the Income Tax Rules, 1962.

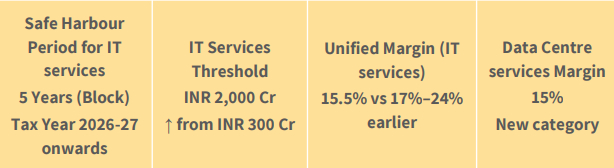

Extension of Safe Harbour Block Period

Earlier, SHRs were notified separately for each year by CBDT. Now, as per draft rules SHRs will apply for a 3-year block period starting from Tax Year 2026-27 and will continue for subsequent blocks unless modified.

Introduction of New Safe Harbour – Data Centre Service

A new dedicated SHR for 'Data Centre Services' has been introduced, covering the provision of physical infrastructure–based services by a data center to overseas Associated Enterprises ('AEs'), with a target operating margin of 15%. Further, the draft rules clearly specify that 'data hosting services' shall not be covered under this SHR.

Rationalisation of IT Service related SHR

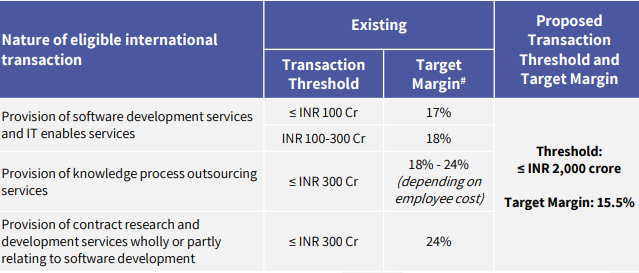

- The draft rules prescribe a single, uniform operating profit margin of 15.5% on operating costs for all eligible IT service transactions - significantly lower than the previously applicable range of 17% to 24% across various categories.

- The applicable transaction value threshold has been substantially increased from INR 300 crore to INR 2,000 crore, making the SHR accessible to a larger universe of IT service providers, including mid to large-sized Global Capability Centers (GCCs)

SUMMARY OF KEY CHANGES IN SHR FOR IT SERVICES

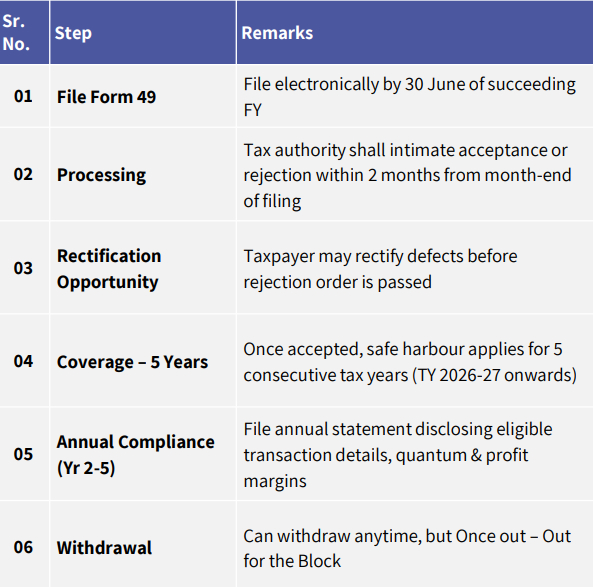

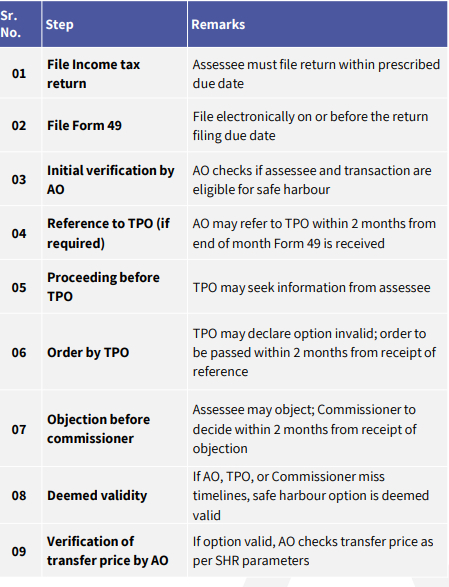

- The draft rules introduce a streamlined, automated, rule-based process for IT services SHR applications, replacing the prior manual assessment process. Process for opting for IT Service SHR is summarised below:

Once out – Out for the Block: Withdrawal from the IT Service SHR is permitted at any time, but once withdrawn, the taxpayer cannot re-enter the SHR during the remaining 5-year block period. This is a significant departure from prior practice and taxpayers should carefully evaluate the decision to opt in and opt out.

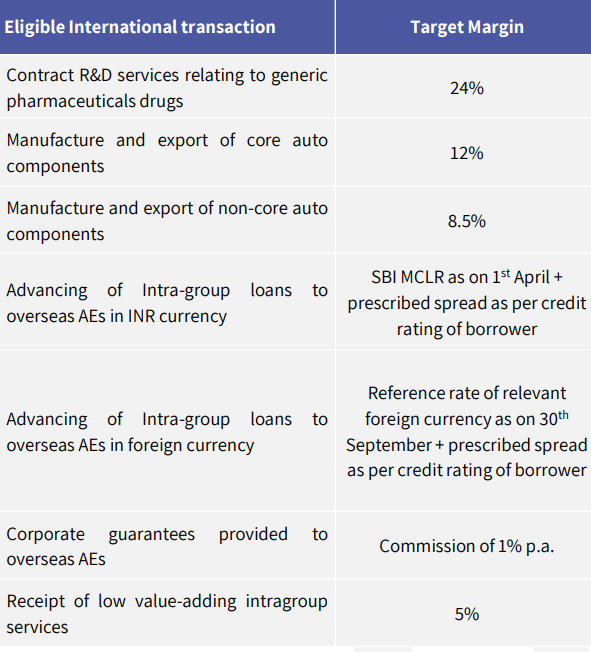

- The draft rules retain the existing SHR framework for non-IT international transactions without any changes. The following categories continue to be governed by the rules as previously notified (subject to applicable thresholds):

PROCEDURE FOR APPLICATION OF SHR FOR NON-IT TRANSACTIONS

Process for opting for Non-IT service transaction SHR is summarised below:

AURTUS COMMENTS

- Reform of Safe Harbour Rules has been a long-standing demand of the industry as well as professionals. This could not have been better timed, considering significant push towards making India as a global GCC hub. Rationalisation of SHR margin to 15.50% under a single category of IT Services, is a very pragmatic view considering the positions finalised in various APAs in this category.

- While the practical impact of implementation will be key, if the proposed changes are integrated effectively, they could offer significant benefits to taxpayers in India. This is particularly relevant in the context of captive service providers delivering 'IT Services' from India, where Transfer Pricing Officers often rely on complex, entrepreneurial entities as comparables and use a comparable set with higher margins during assessment proceedings.

- Currently, the draft rules do not provide clarity on how SHR applications with AE specific segment financials for IT services would be processed in case the taxpayer is engaged in providing services to AEs as well as to Non-AEs or is into an India centric business as well. While for low value-added services, the requirement includes certification of cost allocation from an Accountant, if the same requirement is also extended for IT Service SHR applications wherever segment financials are used, it could provide upfront clarity to various taxpayers who would be considering applying for SHR under IT Service category. We eagerly await the issuance of the final rules, which are expected to provide much-needed clarity on these aspects.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.