- within Corporate/Commercial Law topic(s)

- within Media, Telecoms, IT, Entertainment, Real Estate and Construction and Insurance topic(s)

- with readers working within the Accounting & Consultancy industries

INTRODUCTION

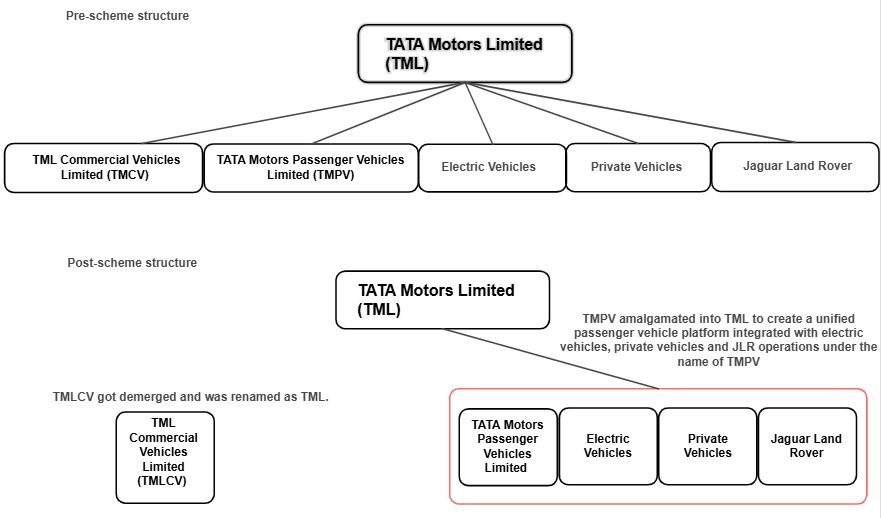

Over the past few years, the Commercial Vehicles Business ("CVB") and the Passenger Vehicles Business ("PVB") have demonstrated strong and consistent performance, driven by the successful execution of distinct and focused business strategies. In order to build on this momentum and enable sharper strategic and operational focus, Tata Motors Limited ("TML") undertook a significant strategic reorganisation and separated the CVB from the PVB, resulting in the creation of two independent and focused entities.

STRUCTURE OF THE DEAL

The composite scheme of arrangement ("Scheme") became effective on 1 October 2025, being the Effective Date and is structured as a single, integrated transaction comprising of two limbs, as described below:

1. Demerger of the Commercial Vehicles Business1

Under the first limb of the Scheme, the CVB of TML was separated and transferred, as a going concern, to TML Commercial Vehicles Limited ("TMLCV.") The transfer included all assets and liabilities, employees, contractual arrangements, intellectual property, licences, permits, approvals, and associated investments relating to the CVB. All contracts, obligations, and legal proceedings (excluding tax proceedings) relating to TML were transferred in the name of TMLCV, with all statutory and regulatory approvals in force. Further, as consideration for the demerger, equity shares of TMLCV were issued to the shareholders of TML in a 1:1 entitlement ratio, resulting in a mirrored shareholding structure in both entities.

2. Amalgamation of the Passenger Vehicles Business2

The second limb of the Scheme provided for the amalgamation of Tata Motors Passenger Vehicles Limited ("TMPV") into TML, to create a unified passenger-vehicle platform integrated with the electric vehicle business, private vehicle and JLR operations. Pursuant to the Scheme, TMPV was dissolved without winding up. All assets, liabilities, employees, contracts, and legal proceedings of TMPV vested in TML as the continuing entity. Given that TMPV was a wholly owned subsidiary of TML, no shares were issued as consideration for the amalgamation. Consequently, the equity shares of TMPV held by TML, stood cancelled in the books of TML, reflecting the consolidation of the PVB within a single legal entity i.e. TMPV.

Pursuant to the implementation of the Scheme and to align corporate identities with the restructured business operations, the company formerly known as TML was renamed as TMPV and TMLCV was renamed as TML.3

KEY LEGAL ASPECTS

NCLT Approval

Under Sections 230 to 232 of the Companies Act, any scheme of arrangement whether a merger, demerger, or amalgamation requires the prior approval from the NCLT. In this case, the Scheme involving the demerger of Tata Motors' CVB into TMLCV, followed by the amalgamation of TMPV into TML, was submitted to the NCLT. The scheme was sanctioned by NCLT Mumbai.4

Approval from Stock Exchanges

Since TML is a listed entity, the restructuring required a no-objection letter5 from the stock exchanges under Regulation 37 of the SEBI LODR, read with the SEBI CircularonSchemes of Arrangement.6 Accordingly, both the National Stock Exchange and Bombay Stock Exchange reviewed the Scheme, assessing its compliance with the conditions on mirror shareholding and post-Scheme governance requirements to ensure that the Scheme was implemented in a manner that avoided unfair prejudice, information asymmetry, or disproportionate benefits to any class of shareholders.

Competition Law

From a merger-control perspective, the Tata Motors' restructuring constitutes an intra-group reorganisation and qualifies as an exempt combination under the Competition Exemption of Combination Rules. The Rules exempt (i) merger or amalgamation within the same group, provided that the transaction does not result in a change in control,7 and (ii) demergers where the resulting company issues shares to the demerged company or its shareholders in proportion to their existing shareholding.8 In the present case, both the PVB and the CVB continue to remain within the Tata Group, with no change in ultimate control. Further, TMLCV issued equity shares to the shareholders of TML on a 1:1 mirror basis and satisfied the proportionality requirement prescribed for demerger-related exemptions under the Rules.

Tax Implications

Under the provisions of the Income Tax Act, (i) any transfer of capital assets under a scheme of amalgamation9 and (ii) any transfer of a capital asset pursuant to a demerger10 between Indian companies is exempt from capital gains tax. Accordingly, the demerger of Tata Motors' CVB into TMLCV and the merger of TMPV into TML are treated as tax-neutral transactions.

OUR THOUGHTS

The Scheme represents a deliberate and forward-looking step to align Tata Motors' corporate structure with the distinct strategic, operational, and capital requirements of its businesses. By enabling independent governance while retaining group control, the reorganisation enhances strategic flexibility, improves transparency, and lays a robust foundation for sustainable growth across both business segments.

Footnotes

1. Part II (Transfer and Vesting of the Demerged Undertaking into the Resulting Company) of the scheme of arrangement (can be accessed here at Annexure2.pdf) ↩︎

2. Part III (Amalgamation of the Amalgamating Company with the Amalgamated Company) of the scheme of arrangement (can be accessed here at Annexure2.pdf) ↩︎

3. Name Change information (can be accessed here at bece4d69-3276-4305-88a5-440ed2a2660e.pdf). ↩︎

4. NCLT Mumbai Order (25 August 2025) (can be accessed here at https://nclt.gov.in/gen_pdf.php?filepath=/Efile_Document/ncltdoc/casedoc/2709138071692025/04/Order-Challenge/04_order-Challange_004_175612431034595096668ac54969a494.pdf) . ↩︎

5. Observation letter regarding receipt of "No Adverse Observations" from Exchange in relation to the Scheme of Arrangement (24 February 2025) (can be accessed here at cv.tatamotors.com/assets/cv/files/investors/2025/02/BSE-Observation-Letter-dated-Feb-24-2025.pdf). ↩︎

6. SEBI Circular on Schemes of Arrangement (3 November 2020) (can be accessed here at SEBI | Schemes of Arrangement by Listed Entities and (ii) Relaxation under Sub-rule (7) of Rule 19 of the Securities Contracts (Regulation) Rules, 1957) ↩︎

7. Para 10, Schedule of Competition (Criteria for Exemption of Combinations) Rules, 2024 (can be accessed here at Competition Commission of India, Government of India) ↩︎

8. Para 12, Schedule of Competition (Criteria for Exemption of Combinations) Rules, 2024 (can be accessed here at Competition Commission of India, Government of India) ↩︎

9. Section 2(1B) and other relevant provisions the Income Tax Act ↩︎

10. Section 2(19AA) and other relevant provisions of the Income Tax Act ↩︎

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.