- within Government and Public Sector topic(s)

- in United States

- within Wealth Management and Intellectual Property topic(s)

The missile supply chain crisis in numbers

The U.S. missile industrial base is attempting something it hasn't done since the Reagan-era buildup: scaling production across virtually every priority weapons program simultaneously. This ramp also has a larger scale and magnitude than the surge of the 1980s.

Record OEM backlogs, multi-year framework agreements unprecedented in the post–Cold War era, and over $74 billion in dedicated munitions funding in the current budget request signal the largest and most durable demand cycle the sector has seen in decades.

The complexity of these missiles and the supply chain through which those dollars flow was not built for events like potentially expending more Patriot missiles in three days than have been built in a single year. Two decades of consolidation reduced the supplier base from roughly 5,000 firms to approximately 1,000, compressed solid rocket motor production to two incumbent manufacturers, and created over 100 identified single points of failure at the sub-tier level.

Over the past four years, the U.S. missile and precision-munitions supply chain has experienced a demand shock that the post–Cold War industrial base was never designed to absorb. A production ecosystem optimized for efficiency and relatively low peacetime throughput is now being asked to support simultaneous consumption in Ukraine and the Middle East while also preparing for a potential Indo-Pacific conflict.

Secretary of State Marco Rubio framed the asymmetry directly: Iran produces over 100 missiles per month, while the U.S. produces six to seven interceptors. One of the key issues is how complex and exquisite these missiles are, yet the most recent Ukraine conflict has demonstrated that you don't need the exquisite; rather, simpler, easier-to-produce products are needed.

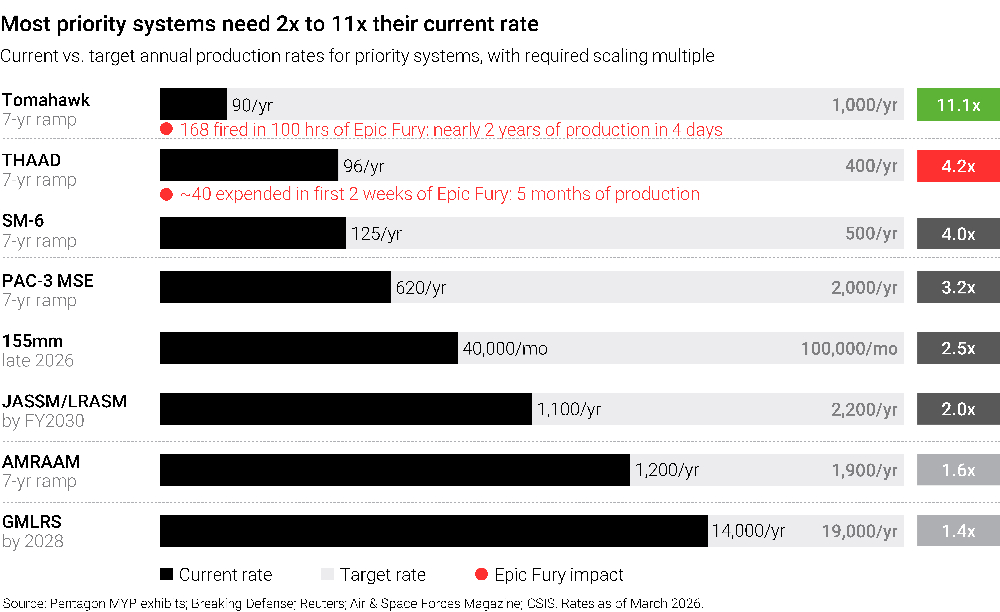

Every priority system faces a two- to six-fold scaling challenge relative to its pre-Middle East crisis baseline. The capital is being committed. The U.S. government is investing in new production capacity alongside primes. The contracts are signed. What remains unresolved is whether the production base can convert those commitments into delivered hardware at the rates required.

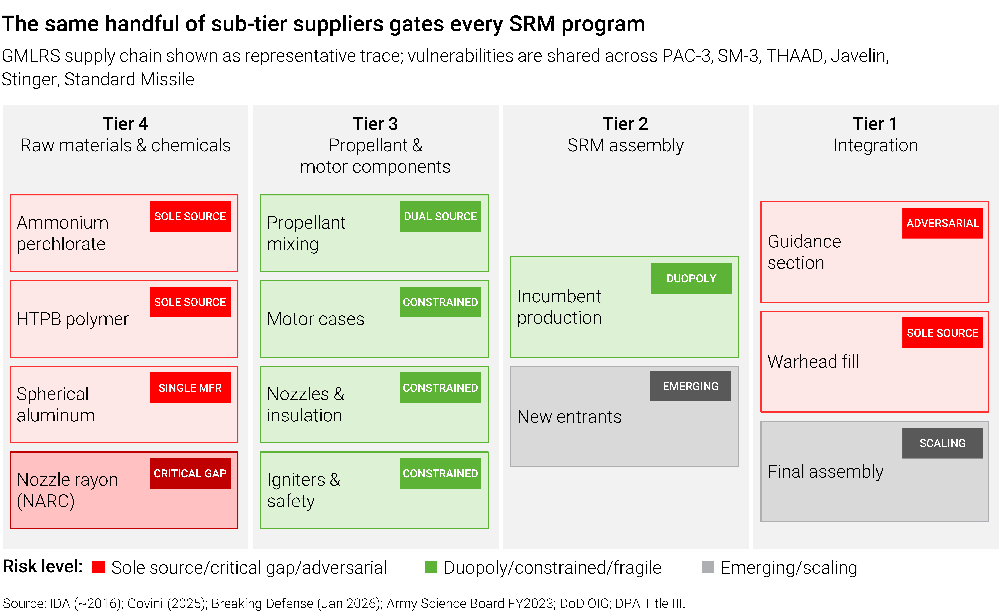

To understand where the binding constraints actually sit, we traced a single weapon system from raw material to delivery. The GMLRS rocket, the workhorse of U.S. precision fires, now scaling from roughly 6,000 to 14,000 units per year, provides the clearest illustration of how demand at the OEM level cascades into fragility at every tier below.

Tracing the vulnerability: from raw chemistry to OEM delivery

A GMLRS rocket is built around a solid rocket motor. That motor begins as raw chemistry: an ammonium perchlorate oxidizer, aluminum powder fuel, and a polymer binder, mixed into composite propellant, cast into a filament-wound motor case, cured, fitted with a nozzle and igniter, and static-tested before shipment to Lockheed Martin for final integration with a guidance section, warhead, and airframe.

At each node in that chain, the supply base is thinner than most stakeholders realize. The ammonium perchlorate, which constitutes roughly two-thirds of the propellant by weight, comes from a single domestic facility. The polymer binder comes from a single supplier whose product quality has measurably degraded, a Navy SBIR solicitation noted that hydroxyl values have decreased from historical levels and funded second sources have stalled in contracting. The spherical aluminum powder comes from a single qualified manufacturer. The nozzle throat material has no current domestic production; the U.S. operates on a limited and diminishing stockpile.

These are not GMLRS-specific vulnerabilities. Each of those upstream suppliers feeds every composite-propellant solid rocket motor in the U.S. inventory: Javelin, PAC-3, THAAD, Standard Missile, Stinger, and the Minuteman III strategic deterrent all flow through the same narrow set of material nodes.

At the motor production tier, two incumbent OEMs produce the vast majority of U.S. tactical and strategic rocket motors. Both are investing aggressively to scale, combined propellant capacity is rising from approximately 30 million to 50 million pounds per year, and one incumbent has increased PAC-3 motor deliveries more than 400% through automation and line consolidation, but both depend on the same constrained materials, and expansion timelines are measured in years, not quarters.

Further downstream, the guidance section introduces adversarial dependency. The rare-earth permanent magnets used in missile fin actuators, seeker stabilization motors, and inertial measurement unit components rely on a supply chain in which China accounts for over 90% of global rare-earth magnet manufacturing capacity. A DFARS prohibition on Chinese-origin samarium-cobalt and neodymium-iron-boron magnets takes effect in January 2027, and no assured domestic alternative at scale exists. The warhead fill stage routes through a single WWII-era government facility, the Holston Army Ammunition Plant, which simultaneously serves the 155mm shell ramp, the insensitive munitions transition, and the broader precision-guided weapons inventory.

GMLRS is among the strongest performers in terms of production among the programs reviewed for this assessment. That is what makes the pattern so striking: the constraints are not program-specific; they are structural. At the OEM level, capacity is expanding in response to an unprecedented inflow of funds driven by significant geopolitical volatility. But below that top layer, the supply chain cascades through a remarkably small number of facilities, any one of which, if disrupted, would cascade across multiple programs simultaneously.

Where risk and opportunity concentrate

The deepest value-creation opportunities in this cycle are unlikely to lie at the prime contractor level, where backlogs are visible and priced accordingly. They concentrate on Tier 2–3 suppliers of SRM components — nozzles, motor cases, insulation — where lead times of 7 to 10 months create pricing power; at propellant raw material producers, where sole-source status creates structural scarcity; and at energetics precursor and guidance subcomponent suppliers, where the identified bottlenecks are most acute. These are also the nodes where operational improvement has the highest production throughput leverage: a 10% yield improvement at a sole-source sub-tier supplier can unlock more delivered missiles than a new assembly line at the prime.

This assessment traces the demand signal from its geopolitical origins through OEM order books and into the sub-tier supply chain, identifying where the binding constraints lie, how long they will persist, and where the resulting gaps create both operational risk and investment opportunities.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]