- within Employment and HR topic(s)

- with readers working within the Advertising & Public Relations and Aerospace & Defence industries

The Widening Wage Gap and The Forces Reshaping U.S. Labor Costs in 2026

The federal minimum wage has not moved since 2009 — but the actual cost of labor has. In 2026, 88 jurisdictions are raising their wage floors, automatic Consumer Price Index (CPI) indexing is locking in permanent increases in the nation's largest markets, and a contracting labor market is squeezing operators from both sides. This spotlight examines the forces reshaping U.S. labor costs and the strategies multi-unit businesses and manufacturers need to respond.

2026 Minimum Wage Landscape

The regulatory environment in 2026 is defined by a "patchwork" of state-level mandates that have effectively rendered the federal minimum wage a localized floor rather than a national standard. For multi-unit operators, this fragmentation creates immense compliance complexity, particularly for those with footprints spanning multiple time zones and legislative jurisdictions.

The federal minimum wage environment in 2026 continues to be characterized by the longest period of legislative inaction in the history of the Fair Labor Standards Act (FLSA). The value of the $7.25/hour rate has eroded by over 30% since its inception, positioning the federal floor below the poverty line for many working families. Twenty states still adhere to this federal baseline, creating a significant competitive gap between "low-cost" states and those aggressively pursuing living-wage mandates.

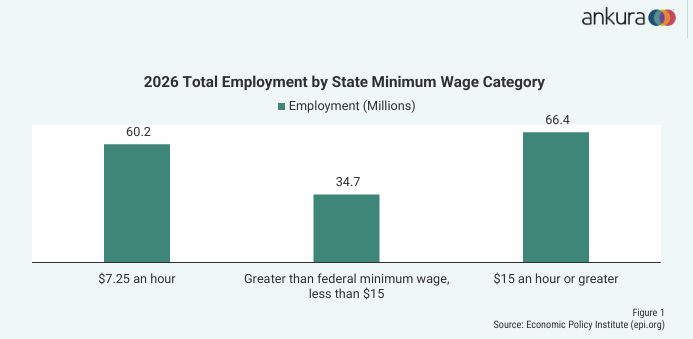

By the end of 2026, 88 jurisdictions (22 states and 66 localities) will have implemented increases to their minimum wage floors. Of those, 79 jurisdictions (14 states, 65 localities) will reach or exceed a $15 minimum wage. This movement is driven by three primary mechanisms: ongoing phased legislation, automatic annual adjustments for inflation (Cost-Of-Living Adjustments (COLAs)), and specific ballot measures approved by voters in recent years. According to the Economic Policy Institute, for the first time, as of 2026, more American workers live in jurisdictions with a minimum wage of at least $15/hour than in those stuck at the federal $7.25 baseline (Figure 1). Over 8.3 million workers benefit from the January 2026 increases alone, adding an estimated $5 billion in annual earnings — and an equivalent payroll burden on operators.

2026 Minimum Wage Overview

The federal minimum wage has not moved since 2009 — but the actual cost of labor has. In 2026, 88 jurisdictions are raising their wage floors, automatic Consumer Price Index (CPI) indexing is locking in permanent increases in the nation's largest markets, and a contracting labor market is squeezing operators from both sides. This spotlight examines the forces reshaping U.S. labor costs and the strategies multi-unit businesses and manufacturers need to respond.

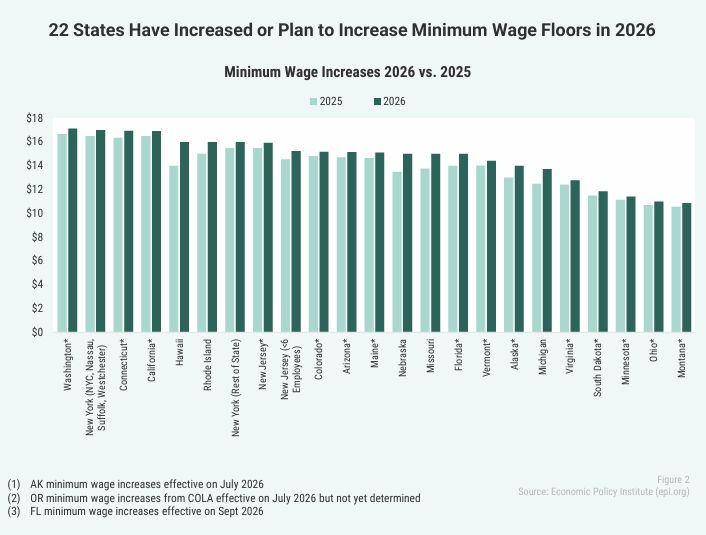

- 22 states and 66 localities increased or increasing minimum wages by end of 2026 (Figure 2)

- 15 states implementing minimum wage increases by way of ongoing and automatic inflation adjustments (COLAs) (“*” on Figure 2)

- 4 states (New York, Hawaii, Rhode Island, Michigan) implementing wage increases as state legislation

- 3 states (Minnesota, Nebraska, Arkansas) implementing wage increases through ballot measures, resulting in strong pay increases

- 48 localities have also already raised their minimum wage in January 2026 (Figure 3) and 18 localities planning increases for later in 2026; all are above state required minimums

- 20 states still operate at the federal minimum wage of $7.25/hour, representing a material share of the U.S. workforce (Figure 4)

In jurisdictions like California and Washington, the local rates for specific sectors — such as hotel, fast food, or healthcare workers — can be significantly higher than the municipal standard rates listed above

While state mandates set the baseline, municipal ordinances have created high-cost “islands” that significantly disrupt regional pricing and labor parity. Multi-unit operators with locations in Seattle, Denver, or the San Francisco Bay Area face localized labor costs that exceed state floors by as much as 25%. The phenomenon of internal wage compression is most acute in these jurisdictions — when the entry-level wage rises above $21.00/hour, the differential between a new hire and a tenured supervisor often collapses, threatening organizational hierarchy and supervisor retention. (Figure 3)

The Indexing Era: Permanent Wage Pressures

The most important wage development of 2026 is not the size of the increases. It is the mechanism. Across the country, states are locking in automatic CPI-based escalators that decouple minimum wage growth from the legislative calendar. Once a state adopts indexing, future increases require no vote and no political capital. The wage floor simply ratchets upward each January, tied to the CPI.

Fifteen states are already operating on this automatic model (Figure 2) but 2026 marks a tipping point. Three of the nation's most influential labor markets are about to cross the threshold into automatic and permanently increasing wages:

- New York completes its final legislative step increase in 2026 ($17 in New York City, $16 statewide) and transitions to annual CPI indexing starting January 2027.

- Florida reaches its $15 milestone on Sept. 30, 2026, and starting in 2027, Florida’s minimum wage becomes CPI indexed, permanently embedding automatic increases into the state’s labor cost structure.

- Michigan will reach $15 by January 2027 under a court-ordered schedule and then transitions to CPI indexing in 2028.

The Labor Paradox of 2026

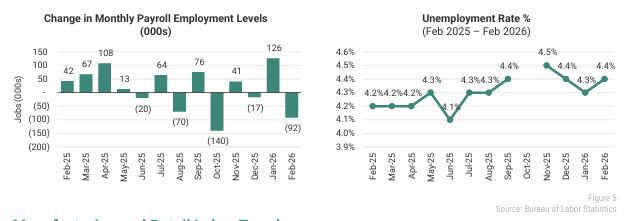

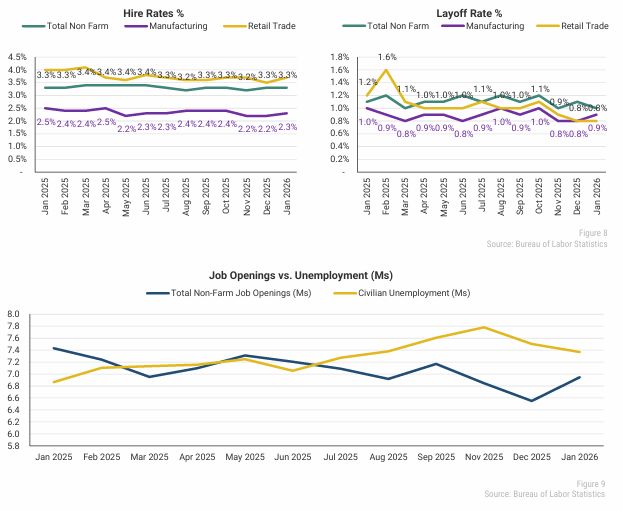

Rising mandated wages are colliding with a labor market that is no longer expanding. The February 2026 Employment Situation report from the Bureau of Labor Statistics (BLS) delivered the sharpest jolt in months: A net loss of 92,000 filled nonfarm payroll jobs, against a consensus expectation of a 50,000-60,000 gain. The unemployment rate edged up to 4.4% and according to the BLS, labor force participation fell to 62.0%, its lowest level since December 2021. February marked the third time in five months that filled payroll employment declined (Figure 5).

Manufacturing and Retail Labor Trends

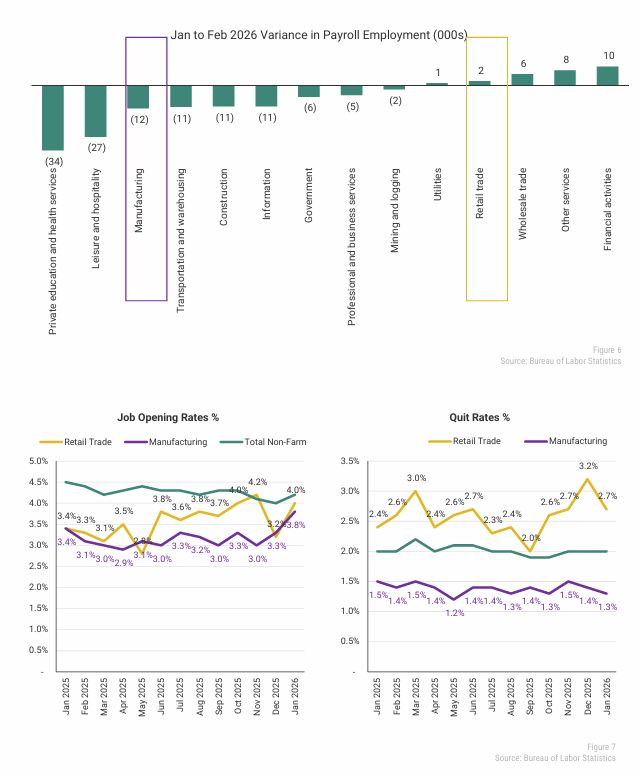

Manufacturing lost 12,000 jobs in February alone, extending a cumulative decline of approximately 98,000 positions since February 2025. The sector is shedding workers even as domestic production incentives are meant to be adding them (Figure 6). In a healthy economy, job openings and quits usually move in the same direction. When companies are hiring aggressively (high openings), workers feel confident that they can find a better-paying or more fulfilling role elsewhere, so they quit their current jobs more frequently. However, job open rates have been steadily increasing since November 2025 while quit rates have steadily declined in the same period for Manufacturing (Figure 7). This divergence suggests workers prefer the safety of their current position in this economic climate and/or the new openings require a growing need for a more specialized skillset as companies invest more in artificial intelligence (AI) and automation.

Retail trade added a modest 2,300 jobs in February, but the broader data shows a more unstable historical trend. While the general market is in a "Big Stay," the retail sector has experienced more volatility as retailers were uniquely exposed to:

- Reduced hiring rates from margin management efforts due to tariff surge exposure and shift to automation

- Spike in quit rates due to burnout from increased workloads associated with the hiring freeze and labor supply constraints

In December 2025, total retail job openings saw a sharp decline to 3.2% while quit rates jumped to a new annual high of 3.2% in the same period, suggesting that workers were leaving even as employers pulled back on new postings. January 2026 reports show the reverse trend with a rebound in job open rates and a decline in quit rates (Figure 7).

These sector-level disruptions are symptoms of a broader structural shift in the labor market; one where neither employers nor employees are making moves.

The Low-Hire, Low-Fire ‘Big Stay’

The labor market is not broken, it is frozen. Layoffs and involuntary separations remain near historic lows, but hiring has stalled alongside them (Figure 8). Workers feel the cost pressures as real wage growth is just 1.4% after inflation but lack the confidence to leave, creating a static and expensive workforce that operators cannot easily reshape through natural attrition. At the same time, net new job openings have continued to decrease since January 2025 and the gap between openings and those unemployed has widened (Figure 9). For operators, this creates a distinct challenge:

- Finding workers is easier than in 2022 as the frenzy of the post-pandemic labor shortage has subsided.

- However, finding the right worker remains difficult as the pool of workers whose skills may not match the available roles continues to grow and as states with the highest wage floors attract and retain labor, while lower-wage states that may have more open factory positions cannot compete for the same workers.

- According to the BLS February 2026 Employment Situation Report, average hourly earnings rose 3.8% year-over-year (YoY) to $37.32 in February. However, with CPI inflation at 2.4%, real wages only grew 1.4%, meaning workers’ purchasing power is barely improving even as payroll costs climb.

Key Challenges for Multi-Unit Businesses and Manufacturers

The convergence of permanently rising wage floors, automatic CPI indexing, and a frozen labor market creates a set of compounding operational challenges for multi-unit businesses and manufacturers. The cost pressures documented in this spotlight — from the 25% locality premiums in Seattle and Denver to the wage compression threatening supervisor retention — share a common structure that demands a strategic, not reactive, response.

1. Workforce Alignment and Productivity

- Increased wages may lead to pressure to make blanket reductions to labor hours overall vs. identifying opportunities to align labor to demand and maximize labor productivity.

- With real wage growth at just 1.4% after inflation, every unproductive labor hour carries a higher cost than it did a year ago.

2. Growing Cost of Inefficiencies in Store and Unit Level Process Execution

- Inefficient processes and workflows become more expensive and harder to justify.

- Too many administrative tasks, manual processes, and inconsistencies in execution will hinder efficiency in operations.

- Businesses oftentimes push non-critical tasks to individual stores or units, burdening on-site teams with work that detract from customer service, sales, and core operations. Centralizing such tasks can allow on-site teams to focus on driving sales and delivering value to the business. In jurisdictions where entry-level wages now exceed $19-21/hour, every minute spent on non-revenue-generating administrative work carries a measurable margin cost

3. Rising Labor Costs and Wage Pressure

- Rising payroll costs squeezes profit margins.

- High competition both within and across industries for the same qualified labor pool contributing to elevated turnover rates and strong push for retention.

- Increased minimum wages create pressures to raise pay for experienced employees. When entry-level wages rise above $21/hour, the pay differential between a new hire and a tenured supervisor collapses — a dynamic already playing out across 48 localities with wages above state minimums

- Shrinking pay differentials create need to restructure performance-based incentives.

- Digital literacy increasingly required in talent pipeline for AI-assisted tasks or advanced manufacturing

4. Technology and Automation Investment

- Understanding where investments in automation and technology need to be made to offset rising labor costs will become more important than ever.

- The growing gap between manufacturing job openings and quit rates suggests that new roles increasingly require specialized or digital skills — making technology investment inseparable from workforce strategy

With these key challenges it is imperative that strategies and improvements are in place to make every labor hour more productive. Though raising prices can be a short-term reprieve, businesses must look to streamline operations and absorb costs elsewhere.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]