- within Tax topic(s)

- with readers working within the Aerospace & Defence industries

- with readers working within the Aerospace & Defence industries

- within Antitrust/Competition Law topic(s)

On February 24, the Florida House and Senate released their initial tax proposals for the 2026 Regular Session. Both initial bills decouple from the corporate tax relief provisions contained in Trump's One Big Beautiful Bill Act, although in different methods.

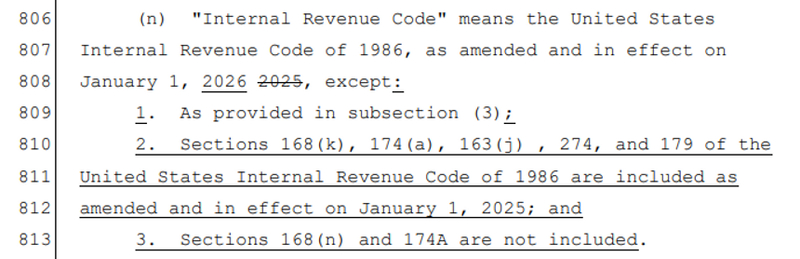

House Bill 7031 from the Ways and Means Committee includes corporate income conformity tax provisions in Sections 23-25. While the House bill updates the January 1, 2026, version of the Internal Revenue Code, it then excepts all the One Big Beautiful (OB3) provisions:

- Section 168(k) – will be implemented as of January 1, 2025

- Section 174(1) – will be implemented as of January 1, 2025

- Section 163(j) – will be implemented as of January 1, 2025

- Section 274 – will be implemented as of January 1, 2025

- Section 179 – will be implemented as of January 1, 2025

- Section 168(n) – not included for Florida

- Section 174A – not included for Florida

Senate Bill 7048 also updates the Florida corporate income tax code to January 1, 2026, then provides specific decoupling for each of the federal provisions.

As initially proposed, SB 7049 would have required:

- For bonus depreciation, the proposal would "disregard" the changes in OB3 for tax years beginning before January 1, 2027. For taxable years beginning on or after 1, 2027, bonus depreciation taken at the federal level would be added back and subtracted 1/7th for seven years (in line with Florida's historic treatment of federal bonus depreciation).

- For qualified production property, the Senate bill would require any federal deduction taken on or after January 1, 2026, to be added back and subtracted 1/7th for seven years.

- For domestic research and experimental expensing under IRC section 174A, the Senate bill would require any federal deduction taken on or after January 1, 2026, to be added back and subtracted as if the changes in the OB3 had not occurred.

- For 163(j) limitations, the Senate bill would require any federal deduction taken on or after January 1, 2026, to be added back and subtracted as if the changes in the OB3 had not occurred.

- For section 179 deduction limitations, the Senate bill would require any federal deduction taken on or after January 1, 2026, to be added back and subtracted 1/7th for seven years.

- For business meals, the Senate bill requires any deduction to be added back and subtracted as if the changes in OB3 had not occurred.

Update: On February 27, an amendment was filed to SB 7048, which would match the House's proposal to fully decouple from the federal tax relief changes.

The 2026 Florida Regular Session is scheduled to conclude March 13, 2026.

While the House bill updates the January 1, 2026 version of the Internal Revenue Code, it then excepts all the One Big Beautiful (OB3) provisions

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.