- with readers working within the Healthcare industries

- within Intellectual Property topic(s)

Spring 2026 AlixPartners–FDRA footwear survey finds out-of-stocks now rival price (65% vs. 67%) as key reason for purchase abandonment, and shows “casual” is still winning, but the definition has shifted

NEW YORK (April 23, 2026) — Stockouts have surged as a leading driver of abandoned footwear purchases, according to the Spring 2026 U.S. Consumer & Executive Footwear Survey from AlixPartners, conducted in partnership with the Footwear Distributors and Retailers of America (FDRA). Sixty-five percent of consumers said they abandoned a purchase because their size was out of stock, a 91% increase year-over-year. Price is still number one at 67%.

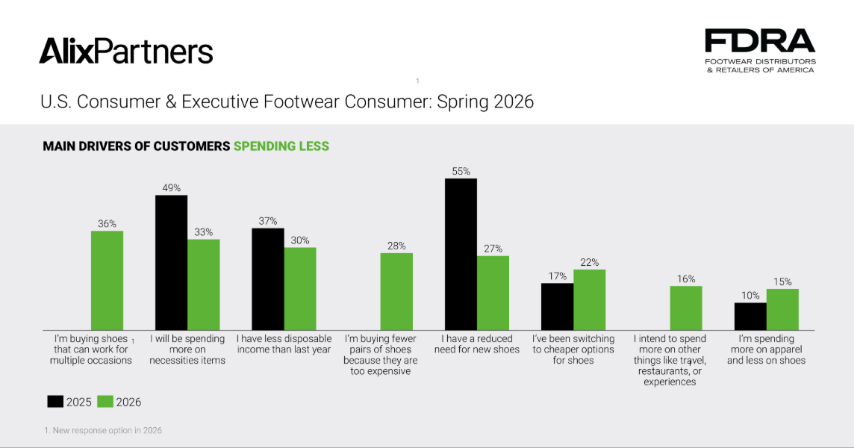

The surge in stockout-driven abandonment marks a notable shift from 2025, when price overwhelmingly dominated purchase decisions amid tariff-driven cost pressures, with 78% of consumers walking away due to cost. Retailers’ more cautious, wait-and-see approach to inventory that took hold last year appears to be translating into reduced shelf-level availability at a time when demand remains active. But retailers are increasingly losing ready-to-buy customers at the point of purchase.

The survey findings arrive against a backdrop of deteriorating consumer confidence. Consumer confidence has plummeted to a record low of 47.6 in April 2026, according to the preliminary University of Michigan Consumer Sentiment Index, marking an 11% decline from March. Fielded in March 2026, the AlixPartners–FDRA survey similarly found that 45% of consumers expected economic conditions to worsen over the next six months. A follow-up pulse survey in mid-April showed that figure rising to 61%, a 16-point increase in a single month amid mounting geopolitical uncertainty and tariff-related cost pressures. The deteriorating outlook is translating directly into changed behavior at the shelf.

“Demand for footwear remains strong, but consumer tolerance for friction has collapsed,” said Bryan Eshelman, Partner & Managing Director and Americas Retail Leader, AlixPartners. “Consumers are doing the research and showing up ready to buy, but too often they are leaving empty-handed because the product is not available in their size or does not meet their price expectations.”

Matt Priest, President and CEO of the Footwear Distributors and Retailers of America (FDRA), said retailers are facing a more challenging operating environment than last year. “As we look ahead, the footwear industry is bracing for continued pressure as tariffs and trade uncertainty weigh on costs and consumer sentiment,” Priest said. “We’re already seeing signs of strain—households are becoming more selective, price sensitivity is intensifying, and purchasing decisions are being delayed or reduced altogether. Our latest consumer and executive survey data confirm what our members are experiencing on the ground: confidence is softening, and affordability concerns are now front and center for both businesses and American consumers.”

Casual is winning, but redefined

Casual footwear is the only category holding relatively steady, and the definition of “casual” has shifted materially. Shoes that fall under this label registered just a 1% net decline in purchase intent, outperforming all other categories. Work shoes and boots fell 16%, fashion and dress declined 8%, and athletic and athleisure dropped 5% and 8%, respectively. More than 9 in 10 consumers plan to purchase casual footwear this year, with half identifying it as a must-buy category.

Shoppers apply the label more broadly than the industry does. Nearly two-thirds (65%) consider athletic sneakers casual footwear, 58% say the same of non-athletic sneakers, and 56% include sandals. Clogs and loafers are also increasingly classified as casual.

“Consumers have redefined casual around versatility and everyday use,” said Sonia Lapinsky, Partner & Managing Director and Fashion Retail Leader, AlixPartners. “Traditional category definitions are losing relevance as shoppers look for footwear that works across occasions and activities. Brands that align their assortment accordingly are better positioned to capture that demand.”

AI investment misaligned with consumer behavior

Despite continued investment in AI-powered consumer tools, footwear shoppers show limited engagement with them for fit decisions. AI-powered fit tools ranked last among six methods consumers use to assess sizing, behind brand size charts, sales associates, comparison tools, the Brannock device, and 3-D foot scans. This pattern held across income levels, with only the highest-income consumers showing modestly higher engagement.

- Consumers instead favor practical, utility-driven tools:

- Price comparison tools (57%)

- Image search (49%)

- Restock alerts (45%)

This aligns with executive sentiment. Ninety percent of footwear leaders cited data analytics and forecasting as top AI priorities, compared to 30% focused on customer-facing applications.

About the Survey

The Spring 2026 U.S. Consumer & Executive Footwear Survey was conducted online from March 9 to March 23, 2026, among 1,006 adult U.S. footwear consumers ages 15 and older, representing a nationally representative audience across all regions, demographics, and income levels. Executive survey methodology was conducted online in Q1 2026, among nearly 100 U.S. executives across footwear brands, retailers and manufacturers in the FDRA membership. For more information about the survey, follow this link to our report, https://www.alixpartners.com/insights/us-consumer-footwear-survey/

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]