- within Finance and Banking topic(s)

- in United States

- with readers working within the Banking & Credit industries

- within Finance and Banking topic(s)

- in United States

- with readers working within the Banking & Credit industries

- within Finance and Banking, Real Estate and Construction and Insolvency/Bankruptcy/Re-Structuring topic(s)

On March 3, 2026, the International Swaps and Derivatives Association, Inc. (“ISDA”) and the Emerging Markets Traders Association (“EMTA”) published the 2026 FX Definitions (the “2026 FX Definitions”), 28 years after the publication of the currently applicable 1998 FX and Currency Option Definitions (the “1998 FX Definitions”). The implementation date for the new definitions is November 22, 2027, after which Swift is no longer expected to support the 1998 FX Definitions. Market participants should begin transitioning to the 2026 FX Definitions as soon as possible.

Introduction

The 1998 FX Definitions, together with its Annex A and related Supplements1 are widely used by market participants to document foreign exchange (“FX”) and currency option transactions. Since 1999, EMTA has in parallel developed and published standard forms of confirmations for various FX transaction types, together with updated standard definitions, market practices and guidance notes, each facilitating the use of the 1998 FX Definitions in evolving FX and currency markets. Over 75 Emerging Markets Template Terms have been published over the years for non deliverable FX and currency transactions (most recently in January 2025), together with various additional sample language and provisions2.

The latticework of the existing publications, supplements and confirmation forms demonstrates the responsiveness of ISDA, EMTA and market participants to the development and expansion of the FX and currency markets over the past three decades. However, this piecemeal evolution has become unwieldy and was due for modernisation3. Indeed, the size of the market for over-the-counter (“OTC”) FX instruments (excluding spot transactions) has grown from around $860 billion in 1998 to $6.6 trillion in 2025.4 Publication of the 2026 FX Definitions is a welcome update to support the trading of this increasingly active asset class.

Market participants can start using the new definitions in their bilateral OTC FX derivatives immediately. From November 22, 2027, the 2026 FX Definitions will replace the 1998 FX Definitions as the standard booklet for all cleared and uncleared FX derivatives transactions.

Overview of the 2026 FX Definitions

Consolidation of the EMTA and ISDA documentation architecture under one umbrella

The 2026 FX Definitions Main Book has been published in digital modular form on the ISDA MyLibrary platform (consisting of 20 Sections), together with the following Matrices:

- Currencies/Financial Centers Matrix;

- Developed Markets Currency Matrix;

- Emerging Markets Currency Matrix;

- Offshore CNY Disruption Fallback Matrix (applicable in respect of Chinese yuan traded outside mainland China, primarily in Hong Kong and Singapore); and

- Settlement Rate Options Matrix.

It is worth noting that the columns in the Emerging Markets Currency Matrix correspond to the fields in the relevant EMTA Template Terms, and the Matrix has separate sections for FX Transactions and FX Option Transactions. This Matrix will automatically apply to the covered Transaction types (unless otherwise specified by the parties in the Confirmation) if Non-Deliverable settlement and a Currency Pair in the Emerging Markets Currency Matrix are specified. Helpfully, certain provisions which are consistent across the various EMTA Template Terms (e.g., Valuation Postponement for Price Source Disruption and the definition of Unscheduled Holiday) have now been included in the 2026 FX Definitions Main Book.

In addition, there are twenty Exhibits to the 2026 FX Definitions which set out the consolidated confirmation templates and certain additional provisions. For example, these include:

- Confirmations for Deliverable and Non-Deliverable FX Transactions and Options;

- Confirmation of a Variance Swap or a Volatility Swap;

- Additional Provisions for Deliverable and Non-Deliverable Disruption Events and Disruption Fallbacks;

- Additional Provisions for Mandatory and Optional Early Termination;

- Additional Provisions for Averaging the Forward Rate, Settlement Rate or the Strike Price; and

- Additional Provisions for a Barrier Transaction.

The 2026 FX Definitions also include Currency Pair Quoting Conventions for use in conjunction with the above. This is a vast improvement over the status quo. The 2026 FX Definitions Main Book, together with the Matrices and centralised confirmation templates, provisions and conventions, serve as the single “golden source”. The online user friendly architecture will make the relevant documentation landscape easier to navigate. As and when further updates are required, ISDA and EMTA can publish a revised version of the 2026 FX Definitions in full (via ISDA’s MyLibrary platform), avoiding fragmented layering of different amendments and/or supplements. Worth noting that EMTA Members who are not ISDA members will have complimentary access to the MyLibrary area of the ISDA website where the 2026 FX Definitions (including the related Matrices and Exhibits) are posted.

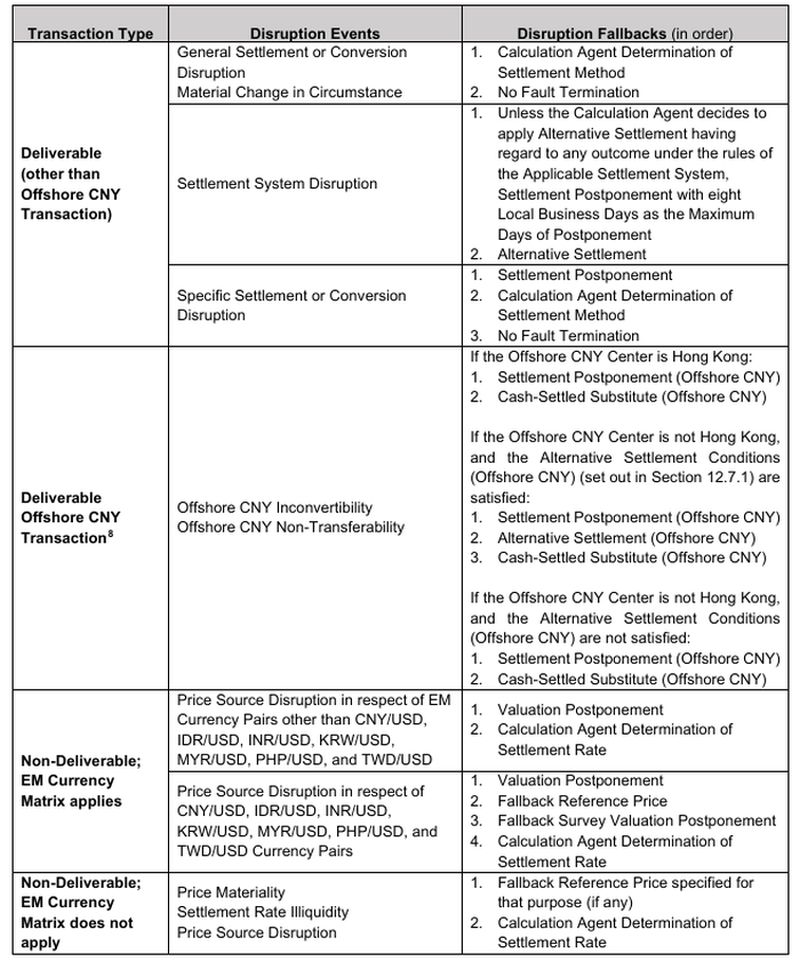

Updates to Disruption Events5 and Disruption Fallbacks6

The 1998 FX Definitions do not include automatic Disruption Events in respect of deliverable FX transactions. By contrast, the 2026 FX Definitions introduce three Disruption Events that apply automatically to deliverable FX Transactions (other than Offshore CNY Transactions)7 (Section 11.3):

- General Settlement or Conversion Disruption (where payment or conversion is impossible across the market after a waiting period of eight Local Business Days);

- Material Change in Circumstance (where payment or delivery is prevented due to a force majeure or act of state after a waiting period of eight Local Business Days); and

- Settlement System Disruption (where payment through the relevant settlement system is deferred such that it would not settle within the specified settlement date).

With respect to Non-Deliverable Transactions (other than Developed Markets Non-Deliverable Transactions), Price Source Disruption continues to apply automatically (Section 11.3.2).

Per Section 11.7, the relevant Disruption Events and presumed Disruption Fallbacks are as follows:

Unless (i) the Disruption Event is Settlement System Disruption, (ii) the EM Currency Matrix applies, or (iii) the Transaction is an Offshore CNY Transaction, if none of the applicable Disruption Fallbacks enable the parties to determine the Settlement Rate or to settle the Transaction, the Transaction will terminate in accordance with the provisions of No Fault Termination provided that the parties have not specified otherwise in the relevant Confirmation (Section 11.7.4).

Other Key Changes

A few other key changes include:

- Full Automated Exercise: New “Full Automated Exercise” provisions for deliverable European FX Options which render ineffective any manual intervention by either party to exercise or to prevent the exercise of that option (Section 6.13). “Automated Exercise” remains the default exercise method.

- Calculation Agent:

- Updated Calculation Agent standard, which requires the Calculation Agent to act and make any determination in good faith and “using commercially reasonable procedures to produce a commercially reasonable result” (Section 1.2.3; now aligned with 2021 ISDA Interest Rate Derivatives Definitions and consistent across New York and English law governed agreements);9 and

- Joint calculation agent dispute resolution provision, which provides that if the parties have elected to act as joint Calculation Agent but are unable to agree on a determination within one Business Day, they would mutually select and be bound by the determination of an independent leading dealer whose fees shall be split equally by the parties (Section 1.2.2).10

- Calendar Adjustment Events: New terms to address the consequences of Calendar Adjustment Events for FX Forwards (Section 19), which, upon the occurrence of an unscheduled market event resulting in an additional non-business day that extends the term of the FX Forward (by postponing the settlement date), allows the parties to choose to either enter into an offsetting transaction or agree to an offsetting fee to neutralise any consequential economic impact.

Implementation Timeline

Overhaul of the Market Infrastructure

As mentioned above, parties can start using the 2026 FX Definitions in their bilateral OTC transactions immediately. The expectation is that Swift, the global financial messaging services provider, will no longer support the 1998 FX Definitions from the November 2027 implementation date. In that sense, adoption of the 2026 FX Definitions is a mandatory market-wide update. Swift expects to publish new Swift Messaging Standards aligned with the 2026 FX Definitions at the end of 2026 (in line with its annual standards release cycle), with the related 2027 Standards User Handbook to be published in July 2027. Other financial market infrastructure providers are also expected to publish implementation plans ahead of the implementation date. Similar to the adoption of the 2021 ISDA Interest Rate Derivatives Definitions, the switch to the 2026 FX Definitions will be a major overhaul of the derivatives market infrastructure. With just under two years until the go-live date, market participants should begin preparing for the corresponding legal, operational and technical shift to ensure efficient and effective transaction lifecycle management.

What’s Next?

It is important to note that, unlike when the 2021 ISDA Interest Rate Derivatives Definitions were being effected, ISDA is not currently planning to issue a protocol for updating legacy FX transactions. However, ISDA has indicated that if there is strong market demand, they will consider:

- Publishing a “bridge” for counterparties to retain bespoke terms in existing Master Confirmation Agreements;

- Providing amendment templates to add the disruption events and fallbacks for deliverable transactions to legacy transactions; and/or

- Including a clause in the ISDA Clause Library to clarify that references to the FX Definitions are to the 2026 FX Definitions.

In addition to webinars, presentation materials and training videos, market participants can expect the following related publications from ISDA in the coming months:

- A “plain English” guide to differences between the 1998 FX Definitions and the 2026 FX Definitions;

- Detailed redlines or comparison tables explaining certain changes for deliverable transactions; and

- Colour-coded annotated template confirmations to highlight modifications.

ISDA members are encouraged to refer to the ‘2026 FX Definitions Industry Implementation Roadmap’ and other resources available on the FX Definitions Update InfoHub (accessible via ISDA.org).11

Footnotes

1. Including, among others, the 2005 Barrier Option Supplement, May 2022 Barrier Event Supplement and the 2011 Non Deliverable Cross Currency FX Transactions Supplement. The provisions of these various supplements have now been incorporated into the 2026 FX Definitions, as further discussed below.

2. For example, the Additional Provisions for Use with a Deliverable Currency Disruption and ISDA Deliverable Currency Disruption Fallback Matrix.

3. Consider that 1998 was the same year Google was launched, plans for the Euro (€) were finalised and Windows 98 was released!

4. See BIS Triennial Central Bank Survey of OTC Foreign Exchange Turnover in April 2025, available here.

5. These are external events that prevent, or ‘disrupt’, the ordinary-course calculation, trading, settlement, or valuation of FX transactions.

6. These are the pre-agreed, automatic solutions to handle disruption events and reduce legal and market risk. Standardized fallbacks typically provide a replacement mechanism and maintain contract continuity.

7. Per Section 11.3.1(i) of the 2026 FX Definitions, unless otherwise specified in a Confirmation, the only Disruption Events applicable in respect of an Offshore CNY Transaction are the “Offshore CNY Disruption Events” as set out in Section 12.2.6, and listed below.

8. See Section 12 (Disruption Events and Disruption Fallbacks for Offshore CNY Transactions) of the 2026 FX Definitions.

9. Under Section 1.3 (Calculation Agent) of the 1998 FX Definitions, the Calculation Agent is required to act in good faith and “in a commercially reasonable manner”.

10. There is a further fallback if the parties are unable to agree on the substitute Calculation Agent: they would each select an independent leading dealer who will agree on an independent third party to act as the substitute Calculation Agent.

11. FX Definitions Update InfoHub – International Swaps and Derivatives Association.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]