- within Insolvency/Bankruptcy/Re-Structuring topic(s)

- within Immigration topic(s)

Key takeaways

- A private trust company ("PTC") is a company formed solely to act as trustee of a specific trust or group of trusts, and can be established in a bespoke manner.

- Family members or trusted advisers may also serve on the board of a PTC, thus offering more direct control and oversight of trust assets.

- Although a PTC adds an extra layer of structure and cost, it can provide significant administrative and confidentiality benefits in high-value or complex family arrangements.

Jersey PTCs have become an increasingly popular option, particularly for administering family wealth. This guide summarises at a very high level the principal features, advantages and considerations of PTCs in Jersey.

Why are Jersey PTCs used and how are they structured?

Unlike professional trustee companies, a PTC exists purely to act as trustee of one or more connected trusts, often for a single family. The PTC is not a commercial trustee providing services to other clients; rather, it is set up for a particular family’s needs and so can be particularly tailored to and focussed on those needs.

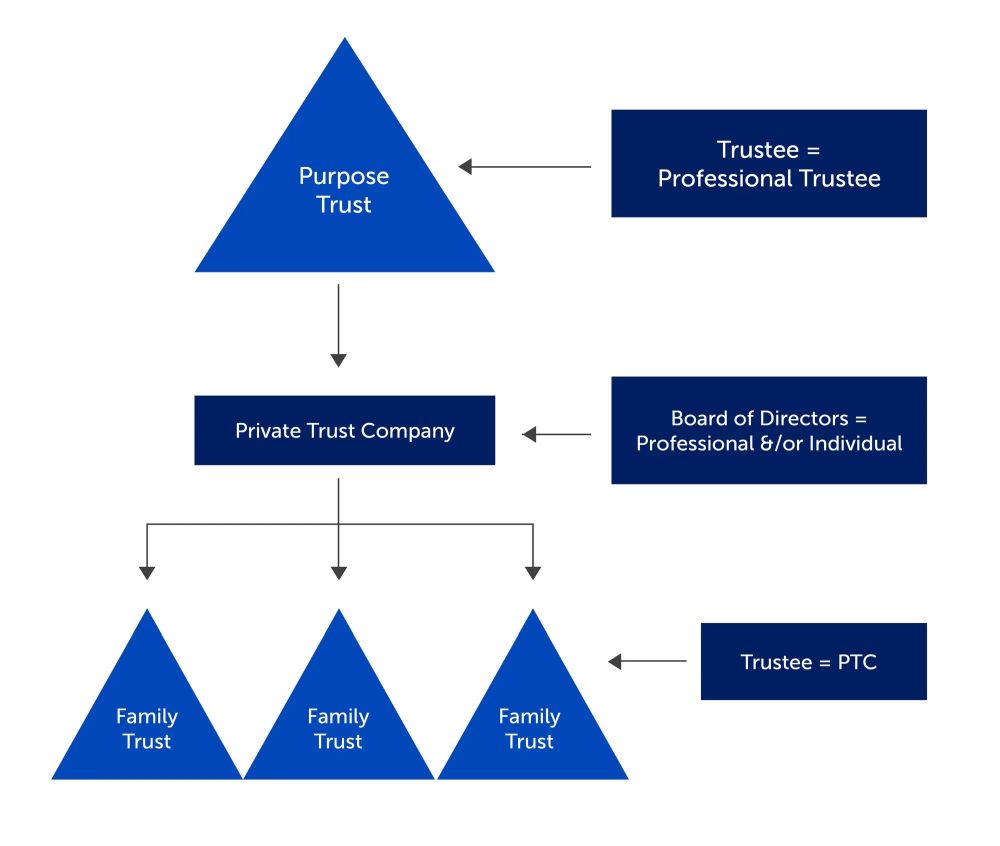

The PTC, being a company, typically has its shares held by a separate orphan vehicle, usually a purpose trust, so that the PTC itself is not ultimately owned by any individual. Usually a professional trustee will act as trustee of the purpose trust. This “orphan” structure is desirable for confidentiality, risk management and ease of administration. However, if the family wish they can retain their interest either as shareholders or through nominee arrangements.

As a corporate entity with its own separate legal personality, the PTC can contract, sue, and be sued in its own name. As trustee, the PTC holds the legal title to the trust assets on trust for the benefit of the beneficiaries, often sitting above more a complicated underlying asset holding structure. A basic PTC structure may look like this:

These underlying structures can be significantly more complicated, possibly with assets separated out into asset classes or by family line.

A PTC is run by its board of directors. These directors may include professional corporate trustees or individuals. Additionally, family members or trusted advisers are often appointed as directors, giving them direct knowledge of, involvement in and influence over how the underlying trusts and assets are managed and bringing special insight to the board.

What are the advantages of a Jersey PTC?

One of the chief benefits of a PTC is the flexibility it offers in governance. Being able to place family members on the board of a PTC means the family can retain an active role in administering the trusts if they wish. This is particularly useful in circumstances where family assets, such as a privately held business, require specialised knowledge or oversight.

In contrast to a traditional trust structure, a PTC simplifies the administration when those involved retire or resign. Instead of changing trustees with the consequent transferring of the legal title of the trust assets into the name of the new trustee, only the board of the PTC is altered. This means there is continuity of legal title to those trust assets with the PTC throughout.

If a purpose trust is used own the shares in the PTC, an orphan structure can provide confidentiality, restricting external parties from easily tracing beneficial ownership of assets to a particular individual. This feature can be especially helpful for families seeking privacy and to protect personal or commercial information from the public domain.

What are the considerations and costs in having a Jersey PTC structure?

While PTCs present many advantages, they do introduce additional costs compared to a straightforward trust arrangement. The PTC must be incorporated as a company with its own directors, and often placed under the umbrella of a purpose trust or foundation, all of which carries set-up and ongoing fees. Consequently, families must weigh the expense against the benefits, which typically justifies using a PTC only where there are substantial or complex assets.

The liabilities of directors of a PTC are assessed in accordance with normal company law principles rather than the stricter trust principles, and the directors' duties are to the PTC itself rather than to the underlying trusts.

The PTC itself might have significant potential liabilities in the event of a breach of trust claim being brought by a beneficiary or other claim being brought by a third party, but it is more difficult for that liability to flow back up through to the directors of the PTC themselves. While this can be attractive to those appointed as directors, it can be less attractive to any beneficiary who later brings a claim.

How are Jersey PTCs regulated?

A PTC does not need to be registered with the Jersey Financial Services Commission ("JFSC") for the purpose of being licensed as a trust company business. This exemption requires:

- a licensed trust company business to act as administrator of the PTC;

- the PTC cannot solicit business from the public;

- the PTC is to act as trustee solely for a specific trust or group of trusts; and

- the name of the PTC to be notified to the JFSC.

Following changes to Schedule 2 to the Proceeds of Crime (Jersey) Law 1999 ("Schedule 2") in 2023, a PTC will now have to register with the JFSC to comply with local obligations for anti-money laundering, countering the financing of terrorism and counter-proliferation financing protections. This registration will require each PTC to undertake activities such as:

- performing customer due diligence;

- appointing key persons for money laundering protections;

- conducting risk assessments, and preparing and enacting policies and procedures to prevent money laundering; and

- relevant record keeping.

However, in light of the positive MONEYVAL report for Jersey, the JFSC is considering changing the guidelines to Schedule 2. The aim is "to review and enhance the existing guidelines to ensure they are clear and effective, whilst also striking a balance between the needs of industry and Jersey’s international obligations".

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]