- within Family and Matrimonial topic(s)

- with readers working within the Aerospace & Defence industries

- with readers working within the Aerospace & Defence industries

- within Tax topic(s)

- with Senior Company Executives, HR and Inhouse Counsel

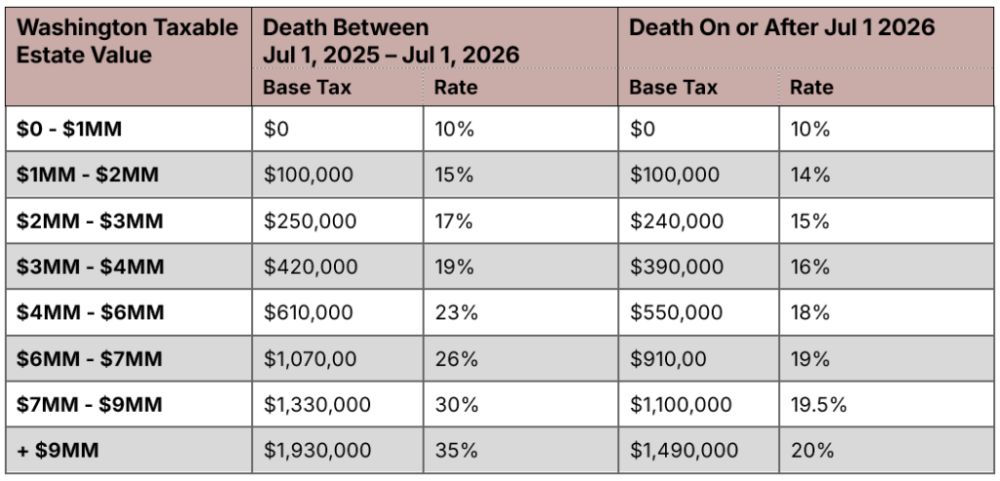

Governor Ferguson has signed into law Engrossed Senate Bill 6347, rolling back last year’s estate tax rate increase to pre-July 2025 levels and effectively freezing Washington’s estate tax exemption at $3 million.

The new law reduces the Washington estate tax rates for decedents dying on or after July 1, 2026. This marks a significant reversal for families with taxable estates (those estates with assets exceeding the Washington estate tax exemption amount) and is particularly impactful for those estates at the top rate levels, as illustrated below. (Note that last year’s estate tax rate increase remains in effect for estates of decedents dying between July 1, 2025, and July 1, 2026.)

While the new law reinstates the lower estate tax rates for Washington taxpayers, it also unwinds last year’s estate tax exemption inflation adjustment. While retaining an inflation adjustment in theory, the new law reverts to basing such adjustment on the Seattle – Tacoma – Bremerton consumer price index, which no longer exists. As a result, the estate tax exemption of $3 million is effectively frozen for the estates of decedents dying on or after July 1, 2026. The current inflation-adjusted exemption amount of $3,076,000 remains in effect for the estates of decedents dying between January 1, 2025, and July 1, 2026.

We will continue to track the effects of this new law and other legislation impacting Washington residents.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]