- within Insolvency/Bankruptcy/Re-Structuring topic(s)

- in China

- with readers working within the Technology industries

- within Criminal Law, Wealth Management and Intellectual Property topic(s)

As we move into the second quarter of 2026, it is increasingly clear that disruption is no longer a cyclical event businesses can ride out – it has become a structural feature of the operating environment.

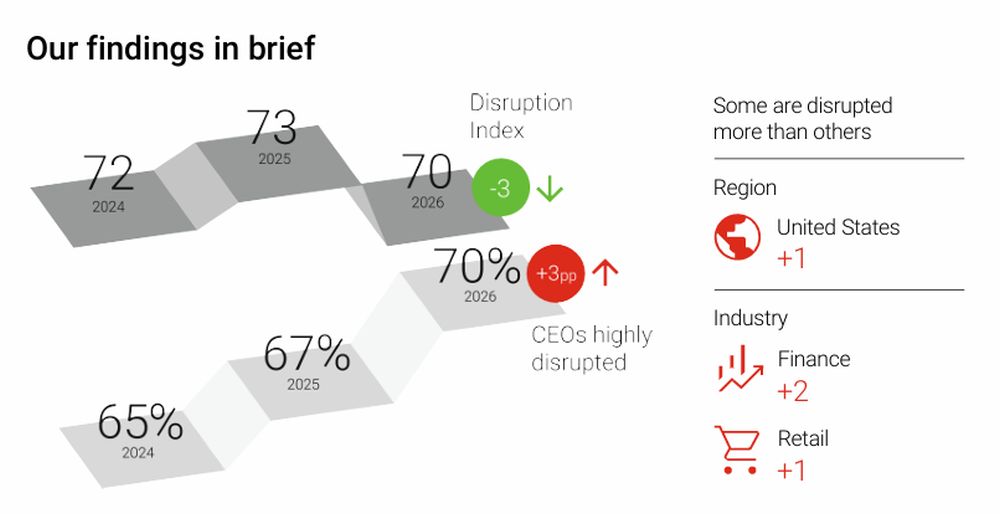

The latest findings from our 2026 Disruption Index reinforce a crucial shift: disruption has normalised. Leaders are not facing fewer shocks; rather, they have developed a higher tolerance for volatility. The danger is that this masks growing internal fragilities in capability, alignment, and resilience – the fault lines that often precede distress.

One of the most striking signals is the widening pressure at the top. CEOs report significantly higher levels of disruption and anxiety than the rest of the C-suite, highlighting a growing leadership disconnect. In our experience, this misalignment can act as a precursor to underperformance: decisions slow, execution weakens, and organisations struggle to keep pace with the risks their leaders can already see. Restructuring is rarely triggered by flawed strategy alone, but by an inability to translate urgency into action.

TECH, ENERGY, AND A TURNAROUND MINDSET

Technology is another major source of strain. While AI investment continues at pace, value realisation lags behind. Only a minority of use cases are delivering measurable impact today, creating exposure to write downs, failed transformations, and stranded assets. Where AI is working, it is doing so in practical, operational applications – from finance optimisation to predictive maintenance – reinforcing the importance of focusing on near-term value rather than ambition alone.

Energy is emerging as the next systemic constraint. Volatility in pricing, grid limitations, and surging demand from AI and electrification are now directly affecting cost bases, planning assumptions and location strategies. Increasingly, facility footprints are being reshaped by energy economics rather than labour or logistics.

Across all of this, one theme stands out: resilience is defined by response, not exposure. The organisations that stay ahead act early, build flexibility into their operating models, and adopt a permanent turnaround mindset – balancing stability with bold, decisive change in an age of continuous disruption.

Restructuring is rarely triggered by flawed strategy alone, but by an inability to translate urgency into action.

THE REALITIES OF DISRUPTION TODAY

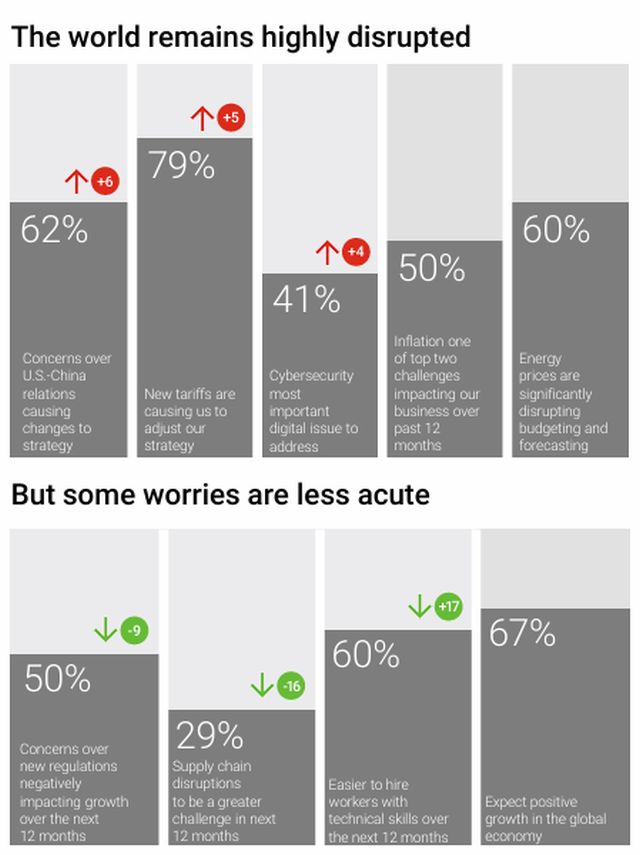

Many of these themes will have contributed to what has been an extremely busy quarter for our practice across EMEA to date in 2026. In addition, the escalating conflict in the Middle East has already heightened economic concerns for the remainder of this year, with the ripple effects related to supply chains, transportation and logistics, inflation, and interest rates very much front of mind for business leaders as they once again rapidly seek to adapt and adjust to this shifting scenario.

Sectors already experiencing varying degrees of contraction across the Eurozone will be buffeted by any spikes in energy costs as gas and oil prices rise.

The chemicals industry in particular – already at risk due to the underperformance of downstream sectors such as automotive and construction – was already facing a challenging future through to 2030, as we explore in our in-depth feature in this newsletter. This pressure may intensify further due to recent events, reiterating the realities of disruption in these times, and the critical need for agility and bold action to emerge safely from distressed situations.

I hope you find the content of this edition informative. Please feel free to contact me or any of the wider team if you would like to discuss these topics in more detail.

IN THIS EDITION:

- Disruption Index: Our findings in brief

- European chemicals sector in focus

- Our thinking across Telecoms, Transport, PE, Risk, and Retail

AlixPartners Disruption index

AI, automation, and robotics are largest opportunities

80% of executives are optimisticabout the impactof AI on theirbusiness

65% are primarily focused on using AI to drive revenue growth (with 35% primarily focused on cost reduction)

77% of CEOs envisioning the deployment of humanoid robots at scale within the next five years

95% of CEOs expect AI to lead to layoffs at their organisation within the next 5 years, including almost half (44%) who expect AI to lead 10% or greater reductions in their workforce

To view the full article, click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]