- with readers working within the Retail & Leisure industries

Many corporate transformations, particularly those aimed at reducing costs or reallocating resources, often have negative impacts on employee engagement.

Carve-outs, which become new standalone companies and/or spin-offs, are typically the opposite—they unlock new opportunities and can generate a wave of energy within the employee team. Nevertheless, like any major transformation, carve-outs come with their own set of people-related challenges and opportunities. To catch the wave of energy, these topics must be addressed effectively.

From our experience in hundreds of complex carve-outs, we see five typical people-related topics that are critical to "get right."

One: Select top leaders to be the voice of CarveCo – the sooner the better

Setting the direction for CarveCo and ensuring its success from day one requires hundreds of decisions – best made by a focused and dedicated leadership team.

In our experience, the minimum team necessary to begin meaningful planning (and credibly speaking to potential buyers, if necessary) includes the CEO, CFO, all operational direct reports, head of sales, and IT leaders. This group can define a path forward for the business, knowing it will own the outcomes. While active HR and legal support is important, it is not typically mandatory to have these leaders in their seats far in advance of close, if targeted RemainCo functional support is available.

Despite the above, there is often tension between focusing on RemainCo's core business and appointing leaders for CarveCo. Some companies believe that CarveCo appointments may become a distraction to the core business, and therefore delay assigning CarveCo leaders.

In a recent experience, a company tried to "get by" with appointing only the CEO and CFO during the pre-close carve-out period. The selected leaders ultimately resorted to using "back channels" to seek core functional input for developing their plans, thereby creating the very distractions the company had hoped to avoid. In parallel, functional workstreams lacked sufficient guidance on key CarveCo design decisions, resulting in delays and missteps. In our view, selecting top leaders early in the design phase would have reduced distractions and led to a smoother carve-out.

Two: Build CarveCo roster – fair share of talent for an exciting opportunity

In heavily entangled functions such as IT, Finance, HR, and Legal, a core question is always "who gets the best people?"

The principle to adopt here is "fair share of relevant talent." If CarveCo represents one-third of the company, it should receive one-third of the top talent. Selections should favor individuals who have historically supported and best understand the CarveCo business.

In large, less entangled operational functions, such as R&D/Engineering and Customer Service, frontline staff may clearly align with CarveCo based on product alignment or similar criteria. Within those same functions, however, there may be highly entangled sub-groups (e.g., functional standards, testing, training), and it may not be feasible to agree on specific staff names prior to deal signing. In these cases, the key principles should be codified in the transaction agreements, including a fair share of talent, target numbers of staff, percentages of mid- and senior-management levels, and average costs.

Joint CarveCo/RemainCo teams, with HR's oversight of a compliant, data-driven process, should make roster decisions without asking employees to "raise their hands," thereby avoiding a messy political or popularity contest.

In every deal we have supported, buyers are deeply interested in "are we getting the good people," and quickly get to the bottom of this through both formal and informal discussions with CarveCo and RemainCo leaders; it is not feasible to "hide" an imbalanced roster.

Similarly, employees want assurance that they are moving to the "good" part of the company with a solid role, manager, benefits, etc. While RemainCo is already well-known, CarveCo has many unknowns—ranging from ownership and strategy to culture, growth opportunities, and compensation/benefits. Well before employee assignments are announced, it is crucial to start an internal campaign highlighting the exciting opportunities awaiting those who join CarveCo.

In a recent carve-out of a set of legacy products, many employees were concerned that CarveCo would not have the "legs" to survive in the long term and were informally lobbying not to be offered roles there. After multiple town hall discussions with the new CEO – someone who was well known within RemainCo – and positive impressions of other leaders appointed to the Executive team, these concerns were alleviated, and the hallway discussions shifted to the opportunity to grow/take on new challenges at CarveCo.

Three: Hire pre-close to fill key CarveCo gaps – launch searches early

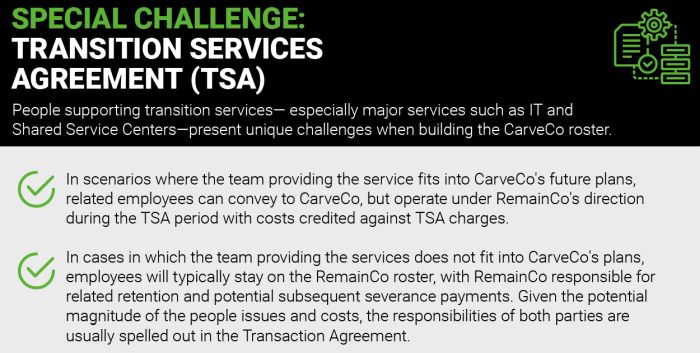

As the CarveCo roster is built out, there will inevitably be some gaps where RemainCo staff are not available and/or qualified. While many of these gaps can remain open post-close (e.g., until the ramp-down of a related Transition Service Agreement), others (e.g., Treasury leadership) may need to be in place and operational at close – and therefore will need to be hired between signing and close. Standalone cost models will have identified the need/role, timing, and cost ranges, so there should be no surprises for either the buyer or the seller.

If the deal Interim Operating Covenants (IOC) specifies, the buyer should be engaged in reviewing the job spec(s), interviewing final candidates, and approving offers for any senior roles.

Experience suggests that CarveCo should initiate these searches early, as market conditions and candidate availability are unpredictable. In a recent deal, top candidates for two critical senior Finance roles went all the way to receiving offers before ultimately dropping out, and the searches had to be re-launched. Had they not started these searches early, the transaction close would likely have been delayed.

Four: Transition long-term incentive plans – follow the market, tailor the plan, and communicate

Top of mind for staff who may be joining CarveCo is always "what does this mean for my total compensation?" While this question encompasses a range of topics, from base/bonus to health/other benefits and long-term incentives, our experience suggests that long-term incentives often pose the most challenging issues, so we will focus on those here.

The typical challenge is how to "make whole" for future / yet to be realized benefits offered by RemainCo for programs that CarveCo does not intend to continue. There are many examples – and details really matter here – but here are two typical examples we have encountered frequently:

- Awarded, but unvested stock / restricted stock units or similar: awarded by RemainCo in prior years but do not vest until after the close of the deal, by which time employees will have joined CarveCo

- Defined benefit pension plans: retirement benefit grows with tenure/compensation at RemainCo, but not at CarveCo

In a recent global carve-out, the leaders of RemainCo initially believed that the only "fair" approach was to make employees 100% whole for what they would have received had they remained at RemainCo. The buyer had a different perspective based on pre-signing discussions and long-term incentive assumptions built into the deal model. With deeper thought, however, both recognized that CarveCo would have parallel benefits which would lead to "double dipping" and that there is an active employment marketplace to test what is "at market/fair."

This led to a much more nuanced solution in which seller and buyer agreed on a plan under which employees who were losing a committed benefit were given a "bridge" payment, which covered a portion of what they might have received had they stayed at RemainCo in parallel with the opportunity to join the CarveCo incentive plans.

Note that in the two examples cited above—and more broadly in these types of situations—the impact will vary significantly by individual, particularly in terms of seniority and tenure. Flexibility to tailor these plans/bridge payments to different groups is essential to developing an equitable and cost-effective outcome that employees will understand and support.

In summary, do not fear these situations: understand the financial impacts, develop a plan "at market," and communicate thoughtfully to each impacted group.

Five: Introduce the new CEO – let them tell their own story

It is not unusual for new owners to introduce a new top leader to increase confidence in achieving deal targets and aspirations. While this can be an initial shock to employees, strong communication can make all the difference.

Introduce the new leader as early as possible, even before the deal closes; this is becoming more typical in recent deals, can be squared with gun jumping guidelines, and provides greater opportunities for the new leader to have an impact.

In a recent carve-out, a new CEO was introduced a few weeks prior to close. RemainCo thanked the popular current leader for their contributions and quickly pivoted to introduce the new leader, who shared in his own words his genuine excitement for and perspective on the company and role in an email sent to all employees slated to join CarveCo. He also had opportunities to meet the management team prior to close to hear their perspectives on challenges and opportunities.

Immediately after the deal closed, he was visible in employee town halls and at key sites. His experience profile perfectly fit the opportunity, and it was clear that he had passion and a plan for the business. All of this went a long way in rapidly building employee acceptance and excitement.

Conclusion

Carve-outs are a great opportunity for employees to accelerate personal growth. By thoughtfully managing the topics described above, you will enable your team to focus on opportunities instead of risks. Employees will be actively listening, so help them build the energy and "catch the wave."

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.