- within Tax topic(s)

- in United States

- in United States

- within Government and Public Sector topic(s)

Original content provided by

Overview of the SbS System

The SbS system provides a framework that effectively exempts US-parented MNEs—and their foreign subsidiaries—from the income inclusion rule (IIR) and under-taxed payment rule (UTPR) on domestic and foreign profits. It also introduces measures to reduce compliance burdens for in-scope MNE groups. The SbS package reflects the G7’s June 2025 “shared understanding,” which called for three main amendments to the Pillar Two rules:- Development of the SbS system;

- Material simplification of Pillar Two administration and compliance; and

- Revised treatment of tax credits and incentives, particularly substance-based non-refundable tax credits.

The OECD’s work was accelerated by the expiration of the temporary UTPR safe harbour at the end of 2025, which essentially exempted US multinational enterprises from the UTPR.

Although the SbS system is the main political driver, most of the technical detail in the package focuses on the simplified ETR safe harbour.

Simplified ETR Safe Harbour

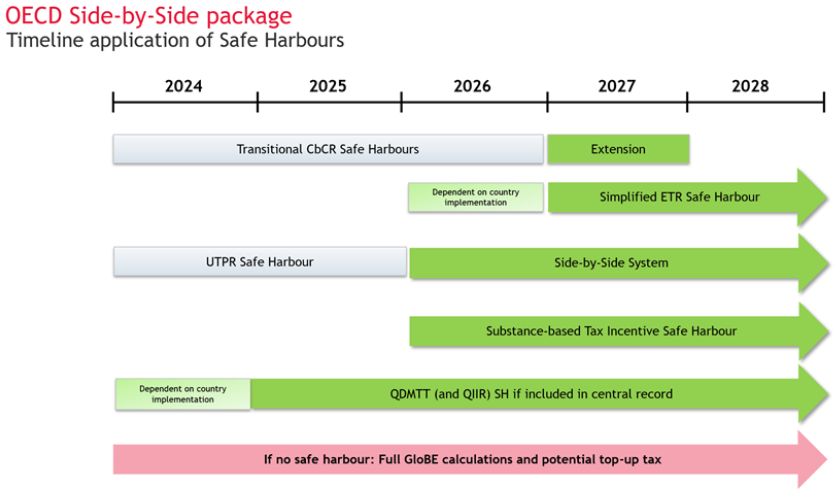

The current transitional CbCR safe harbour—previously set to expire at the end of 2026—has been extended by one year. The OECD has introduced a permanent simplified ETR safe harbour to replace the CbCR safe harbour, the latter of which is intended to reduce administrative burdens by allowing MNEs to demonstrate a sufficient ETR using simplified data rather than full GloBE calculations.Under the new safe harbour, an MNE group may deem the top-up tax in a fiscal year in a jurisdiction to be zero if:

- That jurisdiction’s simplified ETR is at least 15%; or

- The jurisdiction reports a simplified loss.

Key features of the permanent simplified ETR safe harbour are:

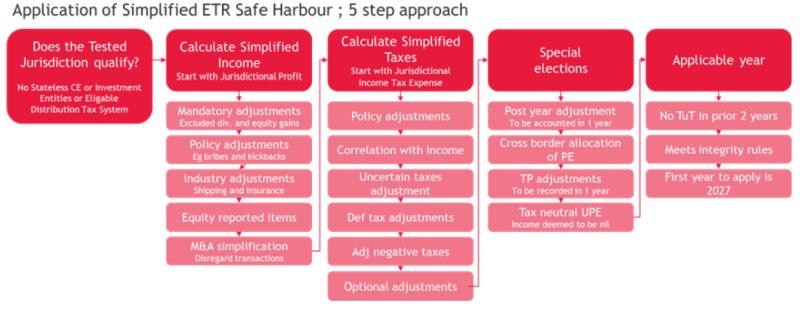

- Tested Jurisdiction Requirements: The simplified ETR safe harbour can only be applied in a “tested jurisdiction” and per subgroup instead of an entity-by-entity analysis, which is a simplification compared to a full GloBE calculation. Entities that qualify as a stateless constituent entity (CE), investment entity or that apply an eligible distribution system in the jurisdiction are generally excluded from qualifying for the simplified ETR safe harbour, though there are exceptions.

- As a result, there will be entities that may qualify under the simplified ETR safe harbour that were not capable of applying the transitional CbCR safe harbour.

- Simplified Income: The starting point for calculating simplified income is the jurisdictional income (i.e., jurisdictional profit before tax or JPBT), which is the MNE’s aggregated income in the tested jurisdiction, with adjustments:

- Allocation rules broadly reflecting the GloBE rules for allocation of profits of permanent establishments and flow-through entities (subject to some differences)

- Mandatory adjustments, such as removing excluded dividends and equity gains or losses and policy-disallowed expenses (e.g., bribes and kickbacks)

- Potential adjustments (subject to election / circumstances): Asymmetric foreign exchange gain or loss, accrued pension expense, transfer pricing

- Industry adjustments to exclude insurance income and shipping income

- Adjustments for equity reported items

- M&A simplification adjustments: To exclude the impact of certain M&A transactions.

- Simplified Taxes: The simplified taxes calculation is based on the income tax expense reported in the financial accounts and incorporates deferred tax accounting to address the impact of timing differences and to minimise recordkeeping burdens. In particular, this calculation starts from jurisdictional income tax expense (JITE), which is the aggregate amount of income tax expense in the financial accounts, with adjustments for:

- Non-covered taxes and tax refunds

- Alignment with simplified income

- Removal of uncertain tax positions

- Deferred taxes at the 15% minimum rate

- Negative taxes

- Optional inclusion of accrued covered taxes that are not included in the financial statements.

- Special Elections: The simplified ETR safe harbour introduces new elections that MNEs can make to mitigate the administrative burden:

- Post-year adjustments recognised when reflected in the financial statements;

- An option to include the income and tax of a permanent establishment in the head office calculation; and

- Any of the GloBE elections permitted under Chapter 3 of the GloBE model rules and commentary.

Because domestic implementation will take time, the transitional CbCR safe harbour is extended through the end of 2026 and the permanent simplified ETR safe harbour becomes available in 2027 (or 2026 where adopted early). For example, the UK has already announced that the permanent simplified ETR safe harbour will be applicable with effect from 1 January 2026. Where both that safe harbour and the transitional CbCR safe harbour are available for a territory, there may be a preference to apply the transitional safe harbour where it is available, given its relative simplicity and its “once out always out” principle.

The following table summarises the application of the simplified ETR safe harbour, but note that certain specific exceptions may apply, which were not included here in the interest of conciseness.

Impact on Business

The new permanent simplified ETR safe harbour takes a different approach than the transitional CbCR safe harbour and is intended to provide a practical alternative to full GloBE calculations. Similar to the GloBE calculation, the starting point of the simplified ETR test is financial statements but fewer adjustments are required and many GloBE principles are not imported (e.g., there is no reference to the GloBE definition of an entity, permanent establishment, etc.). The simplified ETR safe harbour also allows for a simplified deferred tax calculation. The business community has raised concerns that the simplified method still requires additional computations, and in many cases may not be significantly less complex than a full GloBE calculation.The data needed for the simplified ETR safe harbour can no longer be based on available data from the CbCR. For many MNEs that have already invested in a Pillar Two tax engine, a full GloBE calculation is not substantially more complex than the simplified ETR safe harbour requirements. For MNEs that have not yet invested in a sophisticated Pillar Two tax engine, the simplified ETR safe harbour provides for a simplification and for many MNEs a large part of the group will qualify under a safe harbour.

One disadvantage is that after a year with top-up tax liability, two consecutive years of no top-up tax are required before the simplified ETR safe harbour can be re-elected for that tested jurisdiction. If the safe harbour no longer applies, MNEs will need to rework their deferred tax calculation based on GloBE criteria.

However, the advantages of reduced deferred tax liability tracking, fewer prior-year ETR recalculations, less monitoring of GloBE-to-book differences, avoiding complex tax allocations and the optimisation by opting in or out of elections could make a focus on data collection systems aimed at the simplified ETR safe harbour attractive for entities that are expected to qualify for this safe harbour for longer periods of time.

The simplified ETR safe harbour also allows for certain simplifications through elections but MNEs should assess their potential benefits, which will require further preparatory work and may not always be directly transferable to the GloBE calculations. Moreover, most tax engines today focus on GloBE calculations and adapting them for simplified ETR calculations may take some time.

For fiscal year 2026 and 2027, many MNEs will have the transitional CbCR safe harbour as the preferred approach for jurisdictions where the IIR, the UTPR or a domestic minimum top-up tax (DMTT) applies, as data and compliance processes are already aligned with these calculations. The “once out always out” nature of the that safe harbour should also be taken into account (i.e., if the transitional CbCR safe harbour is not applied in 2026, it cannot be applied in 2027, thereby limiting optionality).

We expect that only a few groups will experience major benefits from the simplified ETR safe harbour over the transitional CbCR safe harbour in fiscal year 2027, but there are some groups in specific industries or sectors that may benefit from the industry-specific adjustments permissible under the simplified safe harbour or the ability for certain flow-through or investment entities to apply the that safe harbour. For fiscal years 2027 and beyond (and potentially 2026 when a jurisdictions chooses earlier adoption), the benefits of a simplified ETR calculation versus a full GloBE calculation will have to be assessed per jurisdiction subgroup: when relatively few GloBE adjustments and related data collection would apply, a full GloBE calculation may remain a good option, particularly when the benefits of the substance-based tax incentive can be reaped.

Extension of the Transitional CbCR Safe Harbour

Because the permanent simplified ETR safe harbour is unlikely to be enacted in 2026, the transitional CbCR safe harbour is extended to fiscal years beginning on or before 31 December 2027, provided they do not end after 30 June 2029. The transitional ETR threshold remains at 17% for both 2026 and 2027. The SbS package mentions that the extension also applies to the routine profit test and the de minimis test.

Substance-Based Tax Incentives Safe Harbour

Effective for fiscal years beginning on or after 1 January 2026, certain qualifying tax incentives (QTIs) may be included in covered taxes (or simplified covered taxes when the simplified ETR safe harbour is applied), similar to the treatment of qualified refundable tax credits (QRTCs). This can reduce or eliminate top-up tax that would otherwise arise solely from the incentive lowering the local tax liability.QTIs are capped at

- 5.5% of the higher of payroll expense or depreciation; or

- 1% of the carrying value of eligible tangible assets (if a five year election is made).

Impact on Business

The QRTC regime was generally viewed as too narrow. With few jurisdictions offering qualifying incentives, the broadened scope is expected to bring many existing tax incentives within the safe harbour and encourage jurisdictions to design new ones, particularly those supporting R&D activities or green initiatives.

SbS System

The SbS system introduces a mechanism for situations where an MNE group is headquartered in a jurisdiction with a “robust” international tax system, i.e., one that imposes minimum tax requirements with respect to domestic and foreign income. The SbS system provides a safe harbour for such MNE groups to minimise compliance and administration costs.At the election of the filing CE, the top-up tax for a jurisdiction will be deemed to be zero for purposes of the IIR and UTPR where the CEs of the MNE group are eligible for the SbS safe harbor if the UPE is located in a jurisdiction with a qualified SbS regime.

The SbS regime applies for fiscal years commencing on or after 1 January 2026, depending on local implementation and as listed in the OECD’s central record. As of the date of this alert, the US is the only such jurisdiction.

SbS Safe Harbour

The SbS safe harbour provides relief from Pillar Two top-up taxes on an elective basis for MNE groups where the UPE is located in a jurisdiction with a qualified SbS regime.To qualify for the SbS safe harbour, a jurisdiction must:

- Have an eligible domestic tax system;

- Have an eligible worldwide tax system;

- Provide a foreign tax credit for QDMTTs on the same terms as other creditable covered taxes; and

- Have enacted its eligible domestic and worldwide tax systems before 1 January 2026.

- A statutory nominal corporate income tax rate of at least 20% after taking into account preferential adjustments and subnational corporate income taxes;

- A QDMTT or corporate alternative minimum tax based on financial statement income at a nominal rate of at least 15%; and

- No material risk that covered MNE groups headquartered in a jurisdiction will be subject to an ETR below 15%.

- A comprehensive tax regime applicable to all resident corporations on foreign income and that is imposed on a broad base, which (i) includes the active and passive income of foreign branches and controlled foreign companies (CFCs), regardless of whether that income is distributed; and (ii) is only subject to limited income exclusions that are consistent with the minimum tax policy objectives;

- Incorporates substantial mechanisms that operate unilaterally to address BEPS risks; and

- Has no material risk that in-scope MNE groups headquartered in a jurisdiction will be subject to an ETR below 15% on foreign operations.

UPE Safe Harbour

The UPE safe harbour applies as from 1 January 2026 and replaces the transitional UTPR safe harbour that expired at the end of 2025. The top-up tax for the UPE jurisdiction for a fiscal year will be deemed to be zero for the purposes of the UTPR where the CEs located in the UPE jurisdiction are eligible for the UPE safe harbour.A jurisdiction has a qualified UPE regime if it has an eligible domestic tax system that was enacted and in effect at 1 January 2026. The criteria for an eligible domestic tax system are the same as that outlined above for an eligible domestic tax system.

Impact on Business

None of the rules in the SbS package affects years 2024 and 2025, and MNE groups should continue their compliance activities for those years as planned. Certain rules may have retroactive effect from 1 January 2026 (such as the SbS and UPE safe harbour and, potentially, the simplified ETR safe harbour if adopted for 2026) and governments will need to address the associated legislative challenges. In some jurisdictions, constitutional grounds or other superior law constraints may require a later effective date. Over the coming months, particularly for groups preparing Q1 reporting and provisioning, these uncertainties are likely to prompt significant discussions especially given that the UTPR is already effective as from 1 January 2025 in some jurisdictions while the SbS and UPE safe harbours are not yet in place.MNE groups are expected to respond differently to the new rules. US-headquartered groups will likely focus primarily on DMTT calculations and compliance for their non-US operations, as well as the creditability of DMTTs against US income tax. US group entities—whether the UPE or any US subsidiaries—may be excluded entirely from Pillar Two calculations.

Non-US headquartered groups may also benefit from the SbS safe harbour depending on the location of their UPE. It is difficult to predict how many jurisdictions currently meet the comprehensive requirements for qualification. At present, the OECD has only identified the US regime as a qualified SbS regime. A key question is whether CFC regimes with substance-based carve-outs, which are common in many jurisdictions, will meet the eligibility criteria. The OECD notes that an eligible regime should have implemented BEPS measures, citing CFC rules as an example. This raises the broader question of whether other jurisdictions—including those that have already implemented Pillar Two—will seek SbS status. The rules suggest that obtaining such status would switch off the IIR entirely, enabling groups headquartered in those jurisdictions to compete in low-taxed, non-implementing jurisdictions without incurring top-up tax. However, the OECD has indicated that the level of Pillar Two implementation will be considered in the upcoming “stocktake exercise,” implying jurisdictions withdrawing Pillar Two rules wholescale could prompt a reassessment of the SbS system itself.

Where jurisdictions do not pursue SbS status, reliance may shift to the UPE safe harbour, as the requirements for an eligible domestic tax system appear less stringent than those for an eligible worldwide system. This safe harbour, however, shields only against the UTPR. The IIR and UTPR would continue to apply to all jurisdictions other than the UPE jurisdiction where the UPE jurisdiction has not implemented Pillar Two.

Groups with UPEs in jurisdictions that do not qualify for either the SbS or UPE safe harbour may remain fully exposes to the IIR and UTPR. Pillar Two calculations in implementing jurisdictions will continue to include non-implementing jurisdictions even if where subsidiaries in those jurisdictions would have qualified for the SBS or UPE safe harbour had the UPE been located elsewhere.

BDO Takeaways and What is Next

The SbS package is widely expected to help secure the long-term viability of the Pillar Two regime. It offers welcome clarity for in-scope MNE groups and supports more effective planning around resourcing, compliance models and the use of technology. That said, some stakeholders may feel that the proposed “simplifications” do not go far enough. The guidance references additional workstreams on simplifications, but it remains unclear what further measures may ultimately emerge. In the meantime, although the simplified ETR safe harbour will be less burdensome than a full GloBE calculation for many groups, it is still considerably more complex than the transitional CbCR safe harbour. Detailed review and modelling will be essential.

Since the OECD released the SbS package, the European Commission issued a notice on the arrangement formally acknowledging it and confirming its application in the context of the EU global minimum taxation directive. The UK government plans to implement key provisions in the side-by-side package, as set out in a 7 January 2026 statement by the Exchequer Secretary to Parliament and on the next day, Cyprus announced its consent to the side-by-side package even though Cyprus is not a member state of the OECD.

The new simplified ETR safe harbour offers several advantages, including the ability to incorporate certain industry-specific adjustments and to make a number of elections that mirror those available under the full GloBE rules. In addition, certain flow-through entities and investment entities may qualify—an option not available under the transitional CbCR safe harbour. This should reduce instances where high-tax businesses fail to qualify for a safe harbour due to book-to-tax differences or because profits are fully taxed in the hands of another person at a high tax rate. However, many of the elections are long term in nature and apply for multiple years once made, meaning forward-looking modelling over time will be critical.

The SbS package also reinforces the primacy of QDMTT regimes, and compliance obligations under those regimes will continue. It remains to be seen whether the US will be the only jurisdiction with a qualified SbS regime and how other jurisdictions will respond from a domestic, international and tax incentive perspective.

For now, in-scope groups should reassess safe harbour eligibility, revisit their ETR modelling and map interactions between the QDMTT, IIR and UTPR under the new package. We expect reporting updates as authorities align GIR/schema and validation rules with the package, but the international reaction, including the effective date of the measures in each territory, will need to be monitored.

Finally, members of the Inclusive Framework that have implemented all or part of the GloBE rules will need to update their domestic legislation. This process is expected to take time and few jurisdictions are likely to permit retroactive application of the revised rules. Unlike earlier rounds of administrative guidance, the OECD has not provided model legislative text (other than for the transitional safe harbour), which may result in divergent implementation across jurisdictions.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]