- within Corporate/Commercial Law topic(s)

- in United Kingdom

- within Corporate/Commercial Law, Litigation, Mediation & Arbitration and Real Estate and Construction topic(s)

M&A momentum returns in a more complex market

Global M&A activity is regaining momentum. Pipelines are rebuilding and financing conditions have stabilised, prompting renewed portfolio action. Yet this recovery is unfolding in a materially more complex environment shaped by geopolitical fragmentation, regulatory volatility, shifting tax policy, and accelerating technological change. This is not a conventional rebound cycle. It reflects a structural recalibration of how portfolios are built, separated, and governed — one in which execution discipline is becoming as critical as strategic intent.

In this environment, carve-outs are moving to the centre of portfolio strategy, and execution capability is emerging as a defining institutional advantage.

A disciplined approach to growth

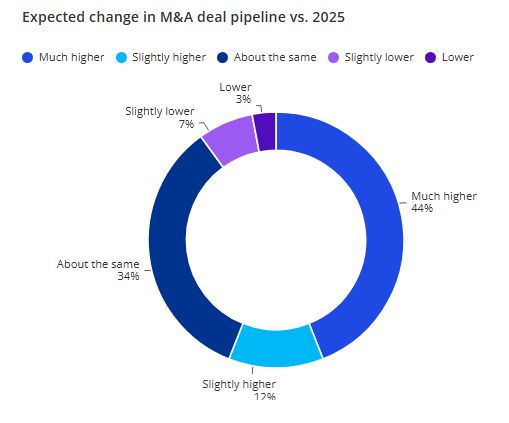

Transaction volumes are expected to increase in 2026 — but this cycle is defined by selectivity rather than exuberance. Most anticipate between three and ten transactions, with deal sizes remaining concentrated below US$1 billion.

Activity is strengthening unevenly across regions, with U.S.-based organisations reporting the highest expected deal volumes, supported by comparatively resilient capital markets and transaction infrastructure. EMEA and APAC remain active, but more measured, reinforcing a multi-speed market rather than a synchronised rebound.

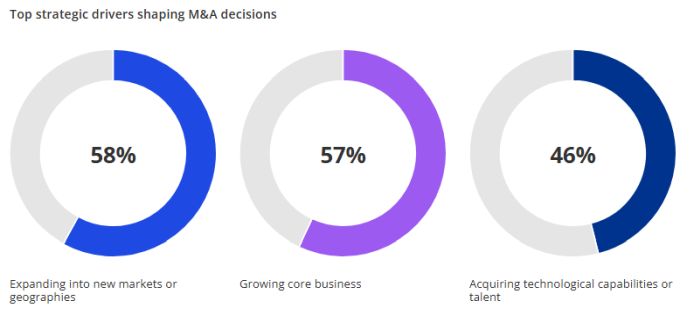

Strategic intent shapes dealmaking

M&A activity in 2026 is anchored in clear strategic priorities, with organisations concentrating capital around durable advantage and long-term positioning. Expansion into new markets and strengthening core businesses are the most cited motivations, alongside the acquisition of technological capabilities and talent. These drivers indicate that dealmaking is being used to sharpen strategic positioning and reinforce long-term advantage — not simply to add scale.

2026: the year of the carve-out

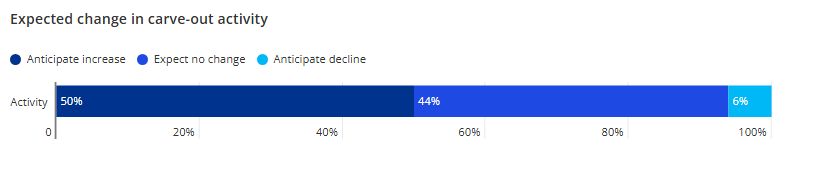

Portfolio reassessment is accelerating, with half of respondents expecting moderate to significant growth in carve-out activity over the next 12–24 months and only 6% anticipating decline. What was once viewed primarily as a tactical pestiture tool is evolving into a defining mechanism of portfolio strategy. Separation is being used to simplify operating models, unlock capital for reinvestment, and sharpen strategic focus.

As this activity intensifies, differences in governance, operational readiness, and execution discipline are becoming more visible — and increasingly consequential.

AI becomes infrastructure — reshaping execution and redefining advantage

AI adoption across the M&A lifecycle has moved beyond experimentation into infrastructure. In competitive intelligence and market analysis — a leading use case — 66 percent of organisations report at least early efficiency gains from generative AI. Yet most of these gains remain incremental rather than transformative, with fewer than one in four organisations reporting significant efficiency improvements.

Adoption remains concentrated in the early stages of the deal lifecycle, where AI supports screening, market analysis, and risk identification. As analytical capacity expands, informational asymmetry narrows — exposing execution gaps earlier in the process.

With deeper integration across valuation, diligence, and post-deal planning, the basis of competitive advantage is shifting. Speed alone may not determine outcomes; durable conviction matters more — the confidence to commit capital based on earlier risk assessment, more rigorous moderlling, and tighter alignment to value creation plans.

Five structural forces reshaping M&A in 2026

Our research identifies five structural drivers shaping portfolio construction, deal strategy, and value capture:

- Strategic focus in a fragmented world

- perging risk appetites between buyers

- Portfolio simplification as a value lever

- AI-driven transformation of deal execution

- Execution discipline as a decisive advantage

Together, these forces are helping to elevate execution capability from an operational function to a defining source of competitive advantage.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.