- within Tax topic(s)

- with Senior Company Executives and HR

- with readers working within the Accounting & Consultancy, Banking & Credit and Business & Consumer Services industries

- with readers working within the Securities & Investment industries

- within Government, Public Sector and Energy and Natural Resources topic(s)

AT A GLANCE

Deeper Disclosures

Benchmarking details, comparables, range & comparability adjustments now disclosed in the form itself not just the TP report

APA Mapping — First Time

Mandatory mapping of APA-covered transactions to Form 48 disclosures, with date, acknowledgeme nt no. & coverage extent

TP Doc Confirmation

Taxpayers must confirm in Form 48 whether a TP study has been maintained introduced as a new statutory obligation

Effective AY 2027-28

Cross Verification Risk Data can be cross verified with other tax and regulatory filings and may be shared with foreign tax authorities BACKGROUND Applies to international transactions & SDT for Tax Year 2026-27 onwards start preparing now

BACKGROUND

- Sinceitsintroduction in 2013, Form 3CEBhasservedasprimary TransferPricing ('TP') disclosure form in India. Taxpayers having international transactions or specified domestic transactions ('SDT') are required to obtain Accountant's Report in Form 3CEB and file the same electronically on or before the prescribed due date (31st October). While Form 3CEB captured basic transaction details, it provided limited analytical depth to tax authorities for the purposeofrisk-basedevaluation

- Recently, Central Board of Direct Taxes ('CBDT') has released draft Income-tax Rules, 2026 for public consultation, wherein existing Form 3CEB is proposed to be replaced entirely with Form 48. Form 48 is a significantly structured and data-rich reporting format built around 6 defined Parts and 11 clauses. Underpinned by the wider goal of enabling risk-based scrutiny of cross-border related-party transactions, Form 48 reflects a decisive shift from narrative disclosure towardstandardised,machine-readabledatasubmission.

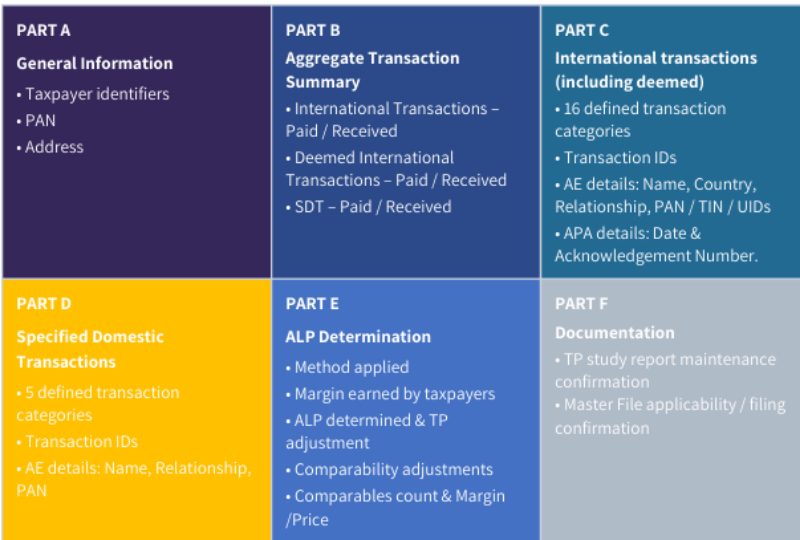

STRUCTURE OF FORM 48

- Since Unlike Form 3CEB, which requires clause-by-clause reporting of each international transaction, Form 48 organizes disclosures into six functional parts. This makes it mores tructured and modular

To view the full article clickhere

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.