- with Senior Company Executives, HR and Finance and Tax Executives

- with readers working within the Accounting & Consultancy, Advertising & Public Relations and Insurance industries

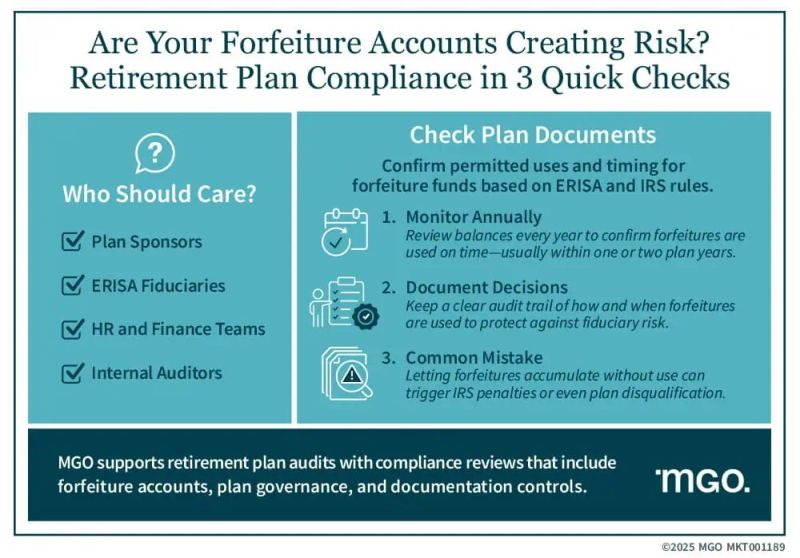

Key Takeaways:

- ERISA plan forfeiture accounts must be used within IRS timelines to adhere to retirement plan compliance.

- Improper forfeiture accounts used in 401(k) plans can raise fiduciary risk and potential ERISA legal exposure.

- An annual review of forfeiture account balances and plan documents can support fiduciary oversight and IRS compliance.

Forfeiture accounts are a normal feature of defined contribution plans, including 401(k) and 403(b) arrangements. These accounts accumulate when employees leave before becoming fully vested in employer contributions. While common, forfeiture balances that are not managed in line with regulatory requirements can present significant compliance risks.

Plan sponsors and fiduciaries must take an initiative-taking approach to managing these funds. At MGO, we have seen how proper oversight of forfeitures supports long-term plan integrity.

Understanding the Role of ERISA, IRS, and DOL

The Employee Retirement Income Security Act (ERISA), along with rules from the IRS and the Department of Labor (DOL), defines how forfeiture accounts should be treated.

Key requirements include:

- ERISA fiduciary standards mandate that all decisions about plan assets, including forfeitures, be made in the best interest of participants and beneficiaries.

- IRS regulations generally allow forfeitures to be used for:

- Paying administrative plan expenses

- Reducing future employer contributions

- Reallocating to participant accounts

Although the IRS issued proposed regulations in February 2023 to clarify forfeiture usage, these have not yet been completed. Nonetheless, fiduciaries are expected to follow current guidance and apply it by their specific plan documents.

Risks Associated With Forfeiture Account Mismanagement

Forfeiture balances must typically be used by the end of the year they arise, or no later than the end of the following year. If these timelines are not met, the plan risks losing its qualified tax status.

Beyond compliance, litigation is an increasing concern. In recent years, more than 70 lawsuits have challenged how forfeitures are used, particularly when used to offset employer contributions. These cases often raise questions about whether such use serves the interests of plan participants.

Not monitoring and use forfeiture appropriately can result in audit findings, reputational concerns, or broader regulatory scrutiny.

Best Practices for Oversight and Use

Plan fiduciaries can minimize risk by adopting a structured, transparent approach to managing forfeitures. MGO encourages plan sponsors to consider the following practices:

- Review plan documents to confirm allowable uses and required timing for forfeitures.

- Monitor account balances regularly to prevent unnecessary accumulation.

- Document fiduciary decisions and discussions about forfeiture usage during committee or board meetings.

Integrating forfeiture oversight into routine plan administration helps reduce the potential for noncompliance and improves operational consistency.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.