- within Tax topic(s)

- within Tax topic(s)

- within Tax, Media, Telecoms, IT, Entertainment and Real Estate and Construction topic(s)

- in India

If you’re investing in Spain, how your withdrawals are taxed can make a huge difference to how much you actually keep. Even when everything else stays the same – the investment, the growth, and the withdrawals – the final outcome after tax can vary significantly.

To understand how this works, let’s look at a simple example:

- Initial Investment: €200,000

- Growth: 5% annually for 15 years

- End Value: €415,786

- Withdrawal: €20,000 per year

This sets the foundation for comparing how different tax treatments affect your income.

There are TWO main ways your investment could be taxed in Spain:

Regular Investment (Standard Tax)

- Taxed on the full €20,000

- Spanish tax bands apply (19%–21%)

Tax: €4,080

Net income: €15,920

Alternatively, consider a different structure:

Spanish-Compliant Investment (Capital-Based)

Each withdrawal is proportionally split between:

- Return of capital (tax-free)

- Gain (taxed only on the profit proportionally against the original capital invested)

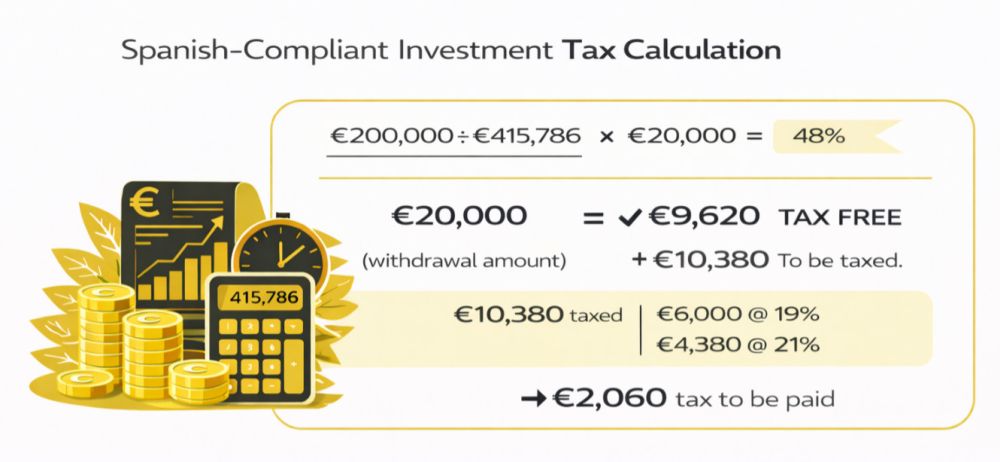

Example (Year 1):

- €200,000 ÷ €415,786 × €20,000

- €9,620 tax-free

- €10,380 taxed

Tax to pay:

- €6,000 @ 19%

- €4,380 @ 21%

Total tax €2,060

Net income: €17,940 per year

15-Year Results

Over time, these differences compound – lets look at how the two approaches compare over 15 years:

| Regular Investment | Spanish-Compliant | |

| Net per year | €15,920 | €17,940 |

| Total received | €238,800 | €269,100 |

| Total tax paid | €61,200 | €30,900 |

The Difference

As you can see, the impact is substantial. The structure alone can lead to around €32,000 in tax savings and more than €2,000 extra income per year.

Why This Works

This outcome is not due to higher returns, but rather a more efficient tax structure. The key principles are:

- You withdraw your own capital first

- Only the gain is taxed ‘proportionally’ against the original amount invested

- Over time:

-The taxable portion decreases

-The tax paid decreases

-Your net income increases

Bigger Investment = Bigger Savings

Naturally, the larger the investment, the greater the potential benefit. For example, with a €400,000 investment using the same parameters of a 5% return per year:

After 15 years, withdrawing €30,000 per year:

| Regular Investment | Spanish-Compliant | |

| Net per year | €23,820 | €26,851 |

| Total received | €357,300 | €402,765 |

| Total tax paid | €92,700 | €47,235 |

Bigger Difference

With a larger portfolio, the savings become even more pronounced – around €45,465 in tax saved and over €3,000 additional income per year.

Key Insight

At this point, an important takeaway becomes clear. Most investors focus on returns, but in Spain, the tax structure can be just as important in determining your final outcome.

Conclusion

In summary, by using a Spanish-compliant structure, you can significantly improve your financial results. This approach allows you to:

- Save tens of thousands in tax

- Increase your annual income

- Improve long-term outcomes

There are also other potential benefits such as mitigating tax for inheritance planning and passing on gains/wealth to children.

I’m here to help you get organised and take those financial worries away.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]