- within Energy and Natural Resources topic(s)

- with readers working within the Technology and Oil & Gas industries

- within Energy and Natural Resources, Strategy and Real Estate and Construction topic(s)

Across Nigeria's producing assets, the flare stack has long been a visible symbol of a deeper structural tension: Nigeria is richly endowed with natural gas yet continues to face acute constraints in reliable energy supply. Routine gas flaring sits at the intersection of these realities.

It is environmentally damaging, economically wasteful and, under Nigeria's petroleum framework, broadly prohibited save in defined exceptions. And yet, material flare volumes have persisted, shaped by infrastructure gaps, market and pricing frictions, and an enforcement model that has often been easier to administer than to deter.

For operators, investors, and financiers, the central question is no longer whether Nigeria has rules on flaring. It does. The more important question is whether those rules, together with reliable measurement and investable utilisation pathways, can consistently convert waste into value.

This article examines gas flaring as an environmental and regulatory liability, and the diligence, structuring, implementation, and enforcement issues that explain why compliance outcomes have lagged behind the sophistication of the rulebook, and why the current implementation cycle under the Nigerian Gas Flare Commercialisation Programme (NGFCP) may mark a shift towards documented allocation, permits, and project implementation.

The NGFCP is best understood as both a compliance tool and an investment platform. It reallocates flare gas to third-party project companies that are incentivised to monetise it, aligning emissions reduction with commercial returns. As the programme moves from allocation into implementation, it provides a practical lens for assessing what is changing in Nigeria's approach to flaring, and what that change could mean for upstream operations, midstream build-out and gas-to-power in a market defined by persistent power deficits.

From "ban on paper" to bankability

Nigeria's attempt to end routine flaring is not new. The Associated Gas Re-Injection Act 1979 contemplated a practical end date of 1st January 1984, subject to ministerial permission to continue flaring where utilisation or re-injection was not feasible. Over time, low flare charges, limited infrastructure and broad administrative discretion converted what was framed as an exception into a de facto operating norm.1

The policy cycle shifted materially in the last decade. Nigeria endorsed the World Bank's Zero Routine Flaring by 2030 initiative in 2016, published the National Gas Policy in 2017, which criticised low flare penalties as a weak disincentive, and enacted the Petroleum Industry Act 2021 (PIA), which recast flare reduction within a modern governance and sanctions framework.2

What is different now is implementation momentum. The NGFCP has progressed from bidding architecture to permit issuance and project documentation, while regulators increasingly align flare reduction with Nigeria's energy-transition narrative, domestic gas utilisation agenda and demand for investable gas infrastructure.

Importantly, the recent NGFCP milestone is not merely that Permits to Access Flare Gas have been issued. NUPRC has stated that the relevant awardees had executed key commercial agreements, including connection agreements, milestone development agreements and gas sales agreements, before receiving the permits. That moves the discussion from prohibition and penalty towards allocation, documentation and implementation.3

For investors, the bankability question is therefore not simply whether flare gas has been allocated. It is whether access rights, metering, host-facility interfaces, gas quality, delivery obligations, offtake and payment support can be documented in a form that financiers will recognise as durable.

When flaring becomes liability

For upstream operators, gas flaring is not merely an environmental externality. It is a multi-dimensional legal risk that can crystallise across statutory offences, regulatory sanctions, civil exposure and rights-based litigation.

The principal obligations sit within petroleum legislation and subsidiary regulations, but they also interact with broader environmental statutes, investor and lender ESG expectations, host-community relations and financing conditions.

The Petroleum Industry Act 2021

The PIA provides the statutory foundation for Nigeria's current flare-reduction framework. Section 104 establishes the offence of flaring or venting natural gas, subject to limited exceptions for emergency, an exemption granted by the Commission, or acceptable safety practice under established regulations.

It also provides that fines are not eligible for cost recovery or tax deduction, making flare penalties a direct economic cost rather than a recoverable operating expense.4

Section 105 reinforces the prohibition framework and, importantly for commercialisation structures, empowers the Commission to take natural gas destined for flaring free of charge at the flare stack. Sections 106 to 108 then complete the architecture. Section 106 requires the installation of metering equipment on facilities from which gas may be flared or vented. Section 107 preserves a limited exemption regime, and section 108 requires gas producers to submit flare elimination and monetisation plans within the statutory framework.4Taken together, these provisions treat associated gas as an asset to be conserved and commercialised, not as an operational waste stream. The design is incremental rather than absolutist: flaring is restricted, exceptions are regulated, measurement is required, penalties are economically hardened, and the statutory emphasis shifts towards monetisation pathways that can be supervised and financed.

Flare Gas (Prevention of Waste and Pollution) Regulations 2018

The Flare Gas (Prevention of Waste and Pollution) Regulations 2018 were important in establishing the earlier flare-gas commercialisation architecture, including flare capture, payments, permits, metering and allocation.

A current analysis should not, however, treat the 2018 Regulations as the sole operative reference point. The framework must now be read through the PIA, the Gas Flaring, Venting and Methane Emissions (Prevention of Waste and Pollution) Regulations 2023, relevant NUPRC guidelines and the NGFCP implementation documents.5

Older references to ministerial certificates and legacy petroleum regulators should be treated carefully in post-PIA commentary. Under the current framework, permissions, permits and enforcement interfaces should generally be framed by reference to the Commission or NUPRC, unless the discussion is expressly describing the pre-PIA historical position.

Routine flaring or venting remains tightly restricted, and the policy objective remains the minimisation and ultimate elimination of non-essential flaring. Where flaring is permitted or occurs, the regulatory framework imposes mandatory flare payments, with rates linked to production levels.

The framework also imposes monitoring and reporting obligations. Producers and permit holders are expected to maintain records of flaring and venting activities, supported by metering equipment installed in accordance with applicable regulatory standards, and to submit prescribed reports to the regulator.

In practical terms, the legacy 2018 architecture remains useful for understanding the commercialisation policy, but the post-PIA position should be stated with care. Permits, approvals and compliance obligations now sit within a regulatory architecture administered principally through NUPRC for upstream petroleum operations.

Non-compliance may expose operators and permit holders to sanctions, including where there is failure to maintain records, install metering equipment or provide accurate flare data.

The point for operators and investors is that the regulatory framework is no longer only about charging a fee for continued flaring. It is increasingly about measurement discipline, transparent reporting, flare elimination planning and the legal architecture for third-party commercialisation.

The 2023 Gas Flaring, Venting, and Methane Emissions Regulations

The Gas Flaring, Venting and Methane Emissions (Prevention of Waste and Pollution) Regulations 2023 are central to the current post-PIA regulatory analysis. NUPRC lists the 2023 Regulations among its gazetted regulations, and international regulatory tracking describes them as replacing the 2018 flare-gas regulations for purposes of the current emissions framework.5

The 2023 Regulations are significant because they place flaring within a broader waste, pollution and methane-emissions framework. They address not only gas flaring, but also venting and fugitive methane emissions. Their stated objectives include reducing the environmental and social impact associated with gas flaring, venting and fugitive methane emissions, preserving and protecting the environment, preventing waste of natural resources, enhancing Nigeria's energy transition, creating social and economic benefits from gas capture, and setting out the procedure through which the Commission may exercise its right to take gas at a flare point.5

This matters commercially. The issue is no longer simply whether an operator has paid a flare charge. The more important questions are whether flare volumes are accurately measured, whether emissions are accurately reported, whether flare elimination and monetisation plans are realistic, and whether third-party access to flare gas can be implemented without operational uncertainty at the host facility. In this respect, the post-PIA framework links compliance, data integrity and project finance.

Environmental and rights-based exposure

Gas flaring also engages broader environmental statutes. The Environmental Impact Assessment Act is relevant to projects likely to have significant environmental effects, including where flaring impacts are not properly assessed or mitigated. The National Environmental Standards and Regulations Enforcement Agency (Establishment) Act 2007 is also relevant to environmental governance generally.

The Climate Change Act 2021 adds a further layer. It establishes a national carbon-budget and emissions-reduction framework and requires private entities meeting prescribed thresholds to designate climate change officers and to report annually on greenhouse gas emissions. This creates a statutory architecture into which methane and flare-related disclosures will increasingly be aligned and frames the MRV reforms discussed below.6

NESREA's role should not, however, be overstated in the petroleum-sector context. The NESREA Act repeatedly frames several of the Agency's enforcement, monitoring, permitting and standards-related functions by reference to matters "other than in the oil and gas sector".

Accordingly, while broader environmental legislation may be relevant to environmental governance, upstream petroleum operations and gas flaring are principally governed through the specialised petroleum regulatory framework administered by the relevant petroleum regulators.7

There is also a rights-based dimension. Section 20 of the Constitution of the Federal Republic of Nigeria 1999 requires the State to protect and improve the environment, although it is non-justiciable under section 6(6)(c).

In Jonah Gbemre v Shell Petroleum Development Company of Nigeria Ltd & Ors, the Federal High Court treated gas flaring as capable of implicating fundamental rights to life and dignity. Gbemre should, however, be framed carefully. It is an important Federal High Court decision illustrating how gas flaring may be pleaded as a rights-based environmental claim. It should not be overstated as settled appellate authority, particularly given its appeal history.

For operators, investors, and financiers, the practical point is that flare exposure is not merely regulatory; it can also carry litigation, reputational and ESG consequences.8

independently. Without reliable measurement, reporting and verification (MRV), penalties, emissions accounting and flare-gas allocation all become less financeable.

Finally, domestic market frictions complicate utilisation

. Pricing, payment discipline, offtake credit, pipeline access, security logistics and grid constraints can make gas capture projects harder to finance than continued flaring. The persistence of flaring therefore reflects a combined failure of deterrence, verification and investability, not simply the absence of rules. International experience also suggests that flare reduction is most effective where enforcement, infrastructure and market outlets move together. Nigeria's challenge is to align all three.

Why data matters

Quantification matters because flare policy is enforced through measurement. What cannot be measured consistently cannot be priced, penalised or commercialised.

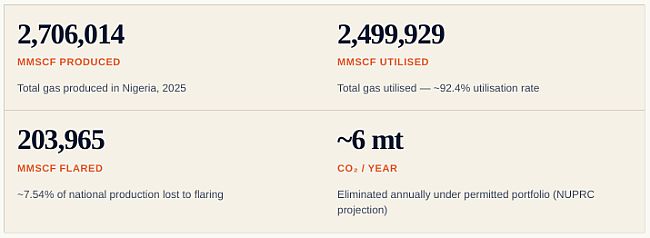

For 2025–2026, Nigeria's flare position should be assessed by reading across official domestic reporting, satellite-derived estimates and industry transparency data. NUPRC's Gas Production Status reporting provides the closest available official domestic series for produced, utilised and flared volumes. NUPRC's 2025 Gas Production Status Report records total gas production of 2,706,014 MMscf, total gas utilised of 2,499,929 MMscf, and total gas flared of 203,965 MMscf, representing 7.54% of total gas produced.

The fourth-quarter data is marked as provisional and may change slightly after reconciliation. The 2025 flare volume is above the approximately 192.9 billion scf reported for 2024, demonstrating that flare volumes remain material even where utilisation percentages are high.9

The World Bank's Global Flaring and Methane Reduction Global Gas Flaring Tracker provides a satellite-based benchmark for flare volumes and flaring intensity. Its 2025 Global Gas Flaring Tracker reported that global gas flaring rose to 151 bcm in 2024, the highest level since 2007, with an estimated 389 million tonnes of CO₂ equivalent emissions, including unburnt methane emissions.

NOSDRA's Nigerian Gas Flare Tracker

provides Nigeria-specific satellite estimates, although it expressly states that its displayed flare volumes are indicative estimates rather than empirical measurements. NEITI reporting remains useful in assessing enforcement credibility, particularly where it highlights outstanding or unremitted liabilities, including gas flare penalties.10

The point is not to force artificial convergence between datasets. It is to distinguish reported figures from independent estimates and to emphasise why MRV discipline is central to enforcement credibility and project bankability.

Methane and MRV: from reporting to measurement-based compliance

The methane dimension is increasingly important. Gas flaring is often discussed through the lens of CO₂ emissions, but incomplete combustion, venting and fugitive methane emissions can materially affect emissions accounting. This makes measurement-based reporting central to regulatory compliance, emissions disclosure and investor confidence.

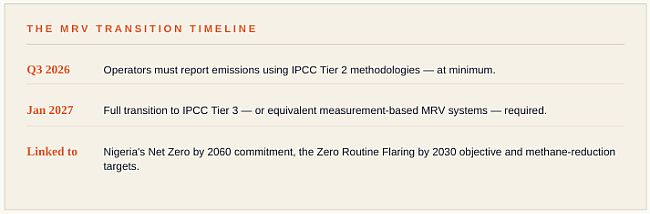

In April 2026, the NUPRC issued a directive requiring upstream operators to adopt standardised templates for greenhouse-gas emissions management plans and methane/GHG emissions accounting.

The directive requires operators, at a minimum, to report emissions using IPCC Tier 2 methodologies from the third quarter of 2026, and to transition fully to IPCC Tier 3 or equivalent high-level, measurement-based MRV systems by January 2027. It also links the reporting transition to Nigeria's Net Zero by 2060 commitment, the Zero Routine Flaring by 2030 objective and methane-reduction targets.11

This development is directly relevant to flare-gas commercialisation. Stronger MRV supports regulatory enforcement, improves emissions accounting and may enhance the credibility of projects seeking climate-linked financing.

Carbon credits and Article 6 opportunities may become relevant for some flare-reduction projects, but they should be treated carefully. Any carbon-credit revenue should depend on additionality, verification, host-country authorisation where applicable, and avoidance of double counting.

For project-finance purposes, such revenue is better treated as upside unless it is properly contracted, verified and capable of being monetised.12

NGFCP in motion: from allocation to execution

Recent developments suggest a shift from framework to execution. In December 2025, NUPRC announced the issuance of Permits to Access Flare Gas to 28 successful awardees under the NGFCP, following the execution of connection agreements, milestone development agreements and gas sales agreements.

The programme has progressed in stages: 42 bidders were awarded 49 flare sites in the bid round, and 28 of those received Permits to Access Flare Gas in December 2025 after executing the required commercial agreements.

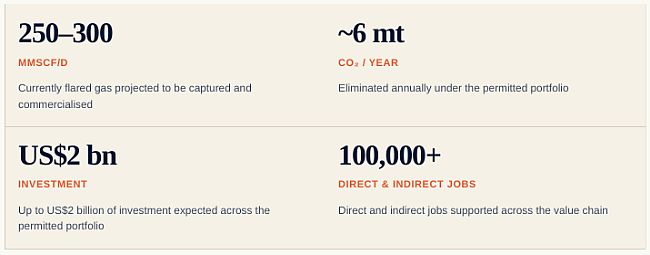

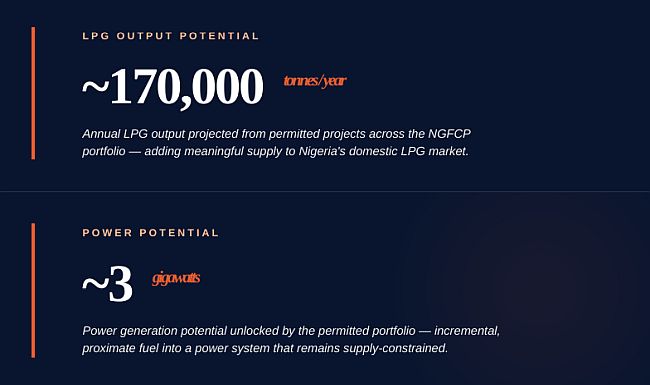

NUPRC has projected that the permitted portfolio, across 49 flare sites awarded to 42 bidders, could capture and commercialise approximately 250–300 MMscf/d of currently flared gas and eliminate approximately 6 million tonnes of CO₂ annually. It has also indicated potential investment of up to US$2 billion, more than 100,000 direct and indirect jobs, approximately 170,000 metric Q3 2026 Operators must report emissions using IPCC Tier 2 methodologies — at minimum. Jan 2027 Full transition to IPCC Tier 3 — or equivalent measurement-based MRV systems — required. Linked to Nigeria's Net Zero by 2060 commitment, the Zero Routine Flaring by 2030 objective and methane-reduction targets. tonnes of LPG per year and nearly 3 GW of power generation potential, depending on project execution and downstream integration.3

These are programme projections, not realised outcomes. Their significance lies in the move from policy aspiration to documented allocation and implementation sequencing. For the oil and gas sector, the permits translate flare reduction into site specific rights and obligations: access to flare points, defined utilisation plans and documented interfaces with host facilities. In practical terms, this begins to convert flare gas from a compliance by-product into a contracted commodity with measurable volumes, quality parameters and delivery points.

For investors and lenders, this matters because permits alone are not enough. Project finance will depend on robust metering, clear access rights, durable connection arrangements, host-facility interface obligations, gas quality and volume commitments, and creditworthy offtake.

The opportunity

Nigeria's gas-to-power opportunity sits at the intersection of three imperatives: emissions reduction, energy security and industrial policy. While gas-to-power is not framed as a single statutory programme, it is one of the most commercially significant end-use pathways contemplated by Nigeria's flare-elimination and domestic-gas policy architecture.

The opportunity is particularly relevant where flare-gas projects can serve proximate, creditworthy demand. Embedded generation, captive power, industrial clusters, data centres and high-load commercial users may offer stronger payment discipline and dispatch certainty than grid-dependent projects. In contrast, grid-supplied projects remain exposed to familiar risks: payment shortfalls, dispatch constraints, transmission limitations and tariff uncertainty.

Fiscal design may also support the broader commercial case for domestic gas utilisation. Under the PIA, hydrocarbon tax does not apply to associated natural gas and non-associated natural gas, and domestically utilised natural gas benefits from preferential royalty treatment.

These fiscal features do not by themselves make a flare-gas project financeable, and they should be tested against the specific facts of each project and any applicable tax reforms, but they form part of the broader policy environment encouraging domestic gas use.13

For the power sector, flare-gas commercialisation can provide incremental and relatively proximate fuel into a system that remains supply-constrained. However, technical potential should not be confused with deliverable capacity. A projection of power potential only becomes financeable where fuel supply, connection, dispatch, permitting, tariff and payment-security arrangements are aligned.

What NGFCP projects teach, in practice

A typical NGFCP-linked structure involves a permit holder or consortium securing access to identified flare sites and implementing capture, processing and utilisation solutions. Downstream commercialisation may include LPG production, industrial fuel supply or gas supply to independent, embedded or captive power projects. The project category and risk profile will vary by flare-site scale, whether the sites are standalone or clustered, gas composition, proximity to demand, required processing, host-facility interface and end-use market.

From a structuring perspective, NGFCP-linked projects will typically require clear flare-gas access and connection arrangements, host-operator interface protocols, metering and delivery-point obligations, gas quality specifications, curtailment and force majeure regimes, payment security, step-in rights, lender protections and change-in-law allocation.

Where the end-use is power, additional attention will be required for generation licensing, embedded or captive power approvals, grid or private-wire arrangements, power-purchase documentation, tariff treatment and payment support.

The core legal question is not simply whether flare gas can be accessed. It is whether access, measurement, delivery and payment obligations can be documented in a way that financiers accept as resilient to operational disruption at the host facility.

What changes for investors, financiers, and operators?

For operators, the direction of travel is clear: flare exposure is becoming harder to treat as a routine operating cost. Operators will need stronger metering discipline, better evidence of compliance, clearer flare elimination and monetisation plans, and more robust interfaces with third-party commercialisation projects.

The PIA's non-cost-recoverability and non-tax-deductibility provisions also mean that flare penalties should be treated as a direct economic exposure, not merely as a recoverable field cost.

For NGFCP permit holders, the challenge is implementation. A permit is only the starting point. Project viability requires secure access rights, reliable volumes, quality specifications, tie-in arrangements, community and security planning, offtake certainty and payment support.

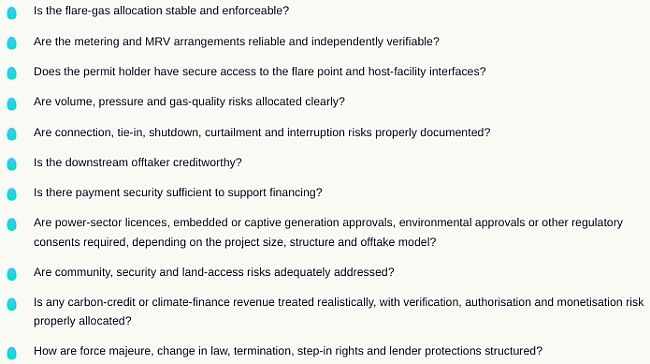

For lenders and investors, the key diligence questions are practical:

These are the issues that will determine whether flare-gas projects become financeable infrastructure or remain stranded policy ambition.

Diligence, structuring, implementation, and enforcement will determine whether a compliance tool becomes an energy-supply lever

Nigeria's gas flaring regime has long been defined by a paradox: strong legal statements of intent, but historically weak deterrence and incomplete market conditions for utilisation. In practical terms, the outcome will turn on diligence, bankable structuring, disciplined implementation and credible enforcement across the NGFCP value chain.

The PIA and the post-PIA regulatory framework, including the 2023 Gas Flaring, Venting and Methane Emissions Regulations, provide a coherent basis for restricting flaring, measuring it and reallocating gas into productive use. The continuing challenge is ensuring that enforcement, data integrity and infrastructure availability combine to make compliance the dominant economic choice.

What is changing is the availability of commercial pathways. The NGFCP shifts the centre of gravity from prohibition and penalty towards structured commercialisation. Permits, connection arrangements, supply obligations and payment-support arrangements can convert flare gas into fuel for power and industry, with measurable emissions benefits.

The central question is now one of implementation. Can Nigeria convert permits into operating assets, replicate transactions across multiple flare sites and maintain a compliance environment in which metering, verification and sanctions are applied predictably? The answer will determine not only the pace of flare reduction, but also whether gas-to-power and gas-based industrialisation can contribute meaningfully to strengthening Nigeria's energy sector in the near to medium term.

Realising this opportunity will depend on alignment across upstream operators, NGFCP permit holders, regulators, midstream providers, power and industrial offtakers, financiers and host communities. It will also depend on disciplined documentation, clear risk allocation and payment structures that make the interfaces from flare point to end-use commercially workable, legally sound and financeable.

Footnotes

1. Associated Gas Re-Injection Act 1979, section 3. The Act prohibited flaring after 1 January 1984 without written ministerial permission, subject to the then applicable statutory framework. See Associated Gas Re-Injection Act 1979 — PLAC Laws of Nigeria.

2. World Bank, Zero Routine Flaring by 2030 initiative; Petroleum Industry Act 2021, available via the official PIA portal.

3. NUPRC press release dated 15 December 2025, "NUPRC Issues Permit to 28 Firms for Flare Gas Utilisation". The press release states that 28 awardees received Permits to Access Flare Gas after executing connection agreements, milestone development agreements and gas sales agreements. It also refers to 42 successful bidders, 49 flare sites, projected capture of 250–300 MMscf/d, about 6 million tonnes of annual CO₂ reduction, up to US$2 billion investment, more than 100,000 direct and indirect jobs, approximately 170,000 metric tonnes of LPG annually and nearly 3 GW of power potential. Available through the NUPRC News archive.

4. Petroleum Industry Act 2021, sections 104–108. Section 104 establishes the offence and provides that flare fines are not eligible for cost recovery and are not deductible for hydrocarbon tax. Section 105 confers the Commission's right to take flare-destined gas free of charge at the flare stack. Section 106 requires metering. Section 108 requires submission of natural gas flare elimination and monetisation plans. See also the World Bank's Nigeria flaring and venting regulatory tracker.

5. NUPRC, Gazetted Regulations; Gas Flaring, Venting and Methane Emissions (Prevention of Waste and Pollution) Regulations 2023; World Bank, Nigeria flaring and venting regulatory tracker.

6. Climate Change Act 2021, in particular the provisions establishing the National Council on Climate Change, the carbon-budget framework and the annual greenhouse-gas reporting obligations for prescribed private entities. See Climate Change Act 2021 — FAOLEX.

7. National Environmental Standards and Regulations Enforcement Agency (Establishment) Act 2007, particularly the provisions framing several NESREA functions and powers by reference to matters "other than in the oil and gas sector". See NESREA Act 2007.

8. Jonah Gbemre v Shell Petroleum Development Company of Nigeria Ltd & Ors, Suit No. FHC/B/CS/53/05, Federal High Court, Benin Judicial Division, 14 November 2005. ELAW's case summary records the rights-based holding and notes that the respondents appealed; the Business & Human Rights Resource Centre also records the appeal history.

9. NUPRC, 2025 Gas Production Status Report. The report records total gas production of 2,706,014 MMscf, total gas utilised of 2,499,929 MMscf and total gas flared of 203,965 MMscf, representing 7.54% flared, with October to December 2025 data marked as provisional. The 2025 flare volume is above the 192,887.06 MMscf recorded in NUPRC's 2024 Gas Production Status Report.

10. World Bank, 2025 Global Gas Flaring Tracker Report; and NOSDRA, Nigerian Gas Flare Tracker. The NOSDRA tracker states that displayed flare volumes and company allocations are estimates based on available data and should be treated as indicative rather than empirical.

11. NUPRC, "Directive on implementing standardised templates and transitioning to measurement-based methane and GHG reporting", April 2026. The directive requires adoption of GHGEMP and methane/GHG accounting templates, IPCC Tier 2 reporting from Q3 2026 and transition to Tier 3 or equivalent measurement-based MRV systems by January 2027.

12. UNFCCC, Article 6 of the Paris Agreement. Article 6.2 provides accounting and reporting guidance for internationally transferred mitigation outcomes; Article 6.4 establishes a mechanism for trading high-quality carbon credits.

13. Petroleum Industry Act 2021, section 260 and the Seventh Schedule fiscal provisions. See the World Bank's Nigeria flaring and venting regulatory tracker, particularly the section on fiscal and emission-reduction incentives. The Nigeria Tax Act 2025 and Nigeria Tax Administration Act 2025 should also be reviewed for any subsequent fiscal reforms applicable to upstream petroleum operations.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.