- within Tax topic(s)

- with Finance and Tax Executives

- in United States

- with readers working within the Accounting & Consultancy and Aerospace & Defence industries

- with Finance and Tax Executives

- in United States

- with readers working within the Accounting & Consultancy, Aerospace & Defence and Retail & Leisure industries

In our recent McCarthy Tétrault Tax Perspectives tour, speakers from McCarthy Tétrault's National Tax Group led a practical discussion of the evolving legislative and judicial tax landscape in Canada and provided attendees with strategic insights and actionable advice.

The January and February 2026 tour featured presentations on the following three topics: (i) a review of the reportable transaction rules with examples, (ii) the impact of new OECD Pillar Two guidance on Canadian entities and tax credits, and (iii) an update on selected 2025 tax disputes highlights.

New Year, Same MDR Rules: A Helpful Review With Examples, Mike Dolson and Erica Hennessey

Mike Dolson and Erica Hennessey discussed an analytical framework for applying the reportable transaction rules in section 237.3 of the Income Tax Act (Canada) (the "ITA").

The reportable transaction rules generally require certain persons to file information returns with the CRA when there is a "reportable transaction". A reportable transaction is generally an "avoidance transaction" that is entered into by or for the benefit of a person, in respect of which at least one of three hallmarks is present: a contingent fee arrangement; confidential protection; or contractual protection. An avoidance transaction is a transaction (or series) where it may reasonably be considered that one of the main purposes is to obtain a tax benefit.

While many people will immediately focus on the existence of a hallmark, a better approach to determining whether a reportable transaction exists is to identify the transactions, identify the tax benefits (if any), and then determine whether there is an avoidance transaction. After determining that there is an avoidance transaction, the next step is to inquire as to whether one of the three hallmarks is triggered.

In circumstances where there is no avoidance transaction, the reportable transaction rules should not apply. There should not be an avoidance transaction where:

- there is no "transaction";

- there is no "tax benefit"; or

- there is a transaction and tax benefit, but it is not objectively reasonable to conclude that one of the main purposes of the transaction (or series) is to obtain the tax benefit.

If there is an avoidance transaction, then one should determine whether any of the three hallmarks is present. If there is a hallmark, then the avoidance transaction is a reportable transaction and an information return must be filed by certain parties.

Only the enumerated persons must file the information return in respect of a reportable transaction. Those enumerated persons are, broadly, the person who has realized the tax benefit, a person who enters into a transaction for the benefit of that taxpayer, and any advisor or promoter who receives a contingent fee or a fee for providing contractual protection.

The presenters examined various examples where the reportable transaction rules are potentially applicable while highlighting the utility of the approach set out above.

Impact of New OECD Pillar Two Guidance on Canadian Entities and Tax Credits, Stephanie Dewey

Stephanie Dewey provided an overview of the new OECD Pillar Two administrative guidance, released on January 5, 2026. This guidance reflects the agreement reached by members of the G7 in June 2025 to develop a "side-by-side" approach in response to the U.S. administration's threat of retaliatory taxes. The key measures are discussed below.

"Side-by-Side" System

The side-by-side system is comprised of two new safe harbours: (i) the Side-by-Side Safe Harbour ("SbS Safe Harbour"), and (ii) the Ultimate Parent Entity Safe Harbour ("UPE Safe Harbour"). These safe harbours are available to multinational enterprise groups ("MNE Groups") with an ultimate parent entity ("UPE") in a jurisdiction that is a "Qualified SbS Regime" or "Qualified UPE Regime", respectively.

MNE Groups that qualify for and elect into the SbS Safe Harbour will not be subject to the Income Inclusion Rule ("IIR") or the Undertaxed Profits Rule ("UTPR") under Pillar Two. However, the Qualified Domestic Minimum Top-up Tax ("QDMTT") will continue to apply to entities in Pillar Two jurisdictions.

MNE Groups that qualify for and elect into the UPE Safe Harbour will not be subject to the UTPR in respect of profits in the UPE jurisdiction (i.e., in the Qualified UPE Regime jurisdiction). The Pillar Two rules will otherwise continue to apply to the MNE Group outside of this jurisdiction.

A Qualified SbS Regime must have an eligible domestic tax regime, an eligible worldwide tax regime, and provide a foreign tax credit for QDMTTs. A Qualified UPE Regime only requires an eligible domestic tax regime (enacted and in effect as of January 1, 2026). As of March 3rd, the only Qualified SbS Regime listed in the OECD's central record is the United States and there are no Qualified UPE Regimes.

The OECD has encouraged jurisdictions to implement the SbS Safe Harbour retroactively to fiscal years beginning on or after January 1, 2026. Canada has not yet enacted the UTPR, but it was originally proposed to be effective for fiscal years beginning on or after December 31, 2024. It remains to be seen whether Finance will extend this date to January 1, 2026 to align with the proposed effective date of the side-by-side system.

Substance-based Tax Incentive Safe Harbour ("SBTI Safe Harbour")

The new SBTI Safe Harbour effectively eliminates the top-up tax attributable to certain substance-based Qualified Tax Incentives ("QTIs"), up to a cap, by providing an offsetting adjustment to covered taxes.

To qualify, a QTI must be "substance-based", i.e., it must be calculated based on expenditures incurred (e.g., on research and development), or the amount of tangible property produced (e.g., output of clean energy) in the jurisdiction. A QTI must also be generally available to all taxpayers. The QTI definition does not limit the form of incentive, so a QTI may take the form of a refundable or non-refundable tax credit, or an enhanced allowance or deduction. However, subsidies or incentives that only defer the timing of taxation are excluded (e.g., accelerated depreciation deductions).

The safe harbour is limited by a cap equal to 5.5% of the greater of eligible payroll costs or the depreciation of certain tangible assets in the jurisdiction. An MNE Group may elect on a five-year basis to an alternative cap of 1% of the carrying value of certain tangible assets (excluding land and other non-depreciable assets) in the jurisdiction.

The SBTI Safe Harbour is intended to be available effective for fiscal years beginning on or after January 1, 2026.

Permanent Simplified Effective Tax Rate Safe Harbour ("ETR Safe Harbour")

The new ETR Safe Harbour is intended to replace the Transitional Country-by-Country Reporting Safe Harbour ("CbCR Safe Harbour") (which has been extended by one year under this administrative guidance).

The ETR Safe Harbour allows an MNE Group to determine its effective tax rate according to a simplified calculation ("Simplified ETR") that is based on financial accounts, but with fewer adjustments than are required under the ordinary Pillar Two rules. The ETR Safe Harbour can be elected on a jurisdictional basis where the Simplified ETR is at least 15% (or the jurisdiction has a loss under the simplified calculation). The rules contain certain mandatory adjustments to income and taxes, as well as a number of optional adjustments and elections that may be available to make the Simplified ETR more precise.

To be eligible to first elect into the ETR Safe Harbour for a jurisdiction, the MNE Group must not have had a top-up tax liability in the jurisdiction in any fiscal year beginning in the preceding 24 months. Unlike the CbCR Safe Harbour, there is an ability to re-qualify after a year in which the MNE Group fails to qualify.

The ETR Safe Harbour is generally intended to be available for fiscal years beginning on or after December 31, 2026, with an option to implement one year earlier. The Transitional CbCR Safe Harbour is proposed to be extended to fiscal years beginning on or before December 31, 2027 in order to support the transition to the permanent rule.

Conclusion

Overall, it is encouraging to see that the OECD is taking steps to simplify Pillar Two. MNE Groups will need to monitor the implementation of these new measures in the jurisdictions in which they operate. It is expected that Canada will implement these measures.

For more information on the administrative guidance, please see our recent blog post here.

Selected 2025 Tax Disputes Highlights, Al-Nawaz Nanji and Dominic Bédard-Lapointe

Al Nawaz Nanji and Dominic Bédard-Lapointe delivered a practical tour through four tax disputes developments. The through-line was clear: tax controversy is increasingly shaped by process and administrative tools, as much as by substantive outcomes in the courts.

Revisions to Proposed CRA Audit Powers

There were proposed changes to legislative amendments to the ITA expanding the CRA's audit and information-gathering powers. While not yet enacted, the practical implications are significant.

Compliance orders and the proposed "compliance order penalty"

For context, if the CRA asks for information or documents and the taxpayer does not provide them, the CRA can go to the Federal Court to seek a compliance order – i.e., a court order compelling production. Under the proposed new powers, however, the CRA would also gain a new tool: if the CRA succeeds in obtaining a compliance order, it could assess a penalty tied to that success.

Three taxpayer-friendly refinements have been proposed to the new penalty:

- Penalty amount becoming discretionary "up to" 10%. Rather than a flat 10% of the tax payable penalty (as the original proposal stated), the new proposal would allow a penalty up to 10%, creating a spectrum from 0% to 10%. This introduces room to argue proportionality and context on quantum.

- A solicitor-client privilege-based exclusion. Now, a carve-out would apply where the taxpayer has a reasonable belief the material requested is protected by solicitor-client privilege.

- An objection path where the CRA must vacate unfair or disproportionate penalties. Third, taxpayers would be able to object, and the CRA would be required to vacate the penalty, where it is disproportionate or unfair in the circumstances. For example, a large corporate taxpayer failing to produce a minor item (e.g., a $100 receipt), should not automatically translate into a penalty outcome that is wildly out of proportion (e.g., a 1% penalty where tax payable is $1 million, amounting to $10,000).

Information-gathering

The original proposal to amend the ITA was that taxpayers had to comply with the CRA's information gathering powers without cost to the Crown. However, the words "without cost to the Crown" were dropped in the latest proposal. This means that when requests become sprawling – especially where documents are archived offsite, held by third parties, or stored in formats that are difficult to retrieve – taxpayers should be ready to argue that proportionality matters, including on cost and feasibility. In other words, taxpayers can now argue the cost would be disproportionate to providing a document and taxpayers do not necessarily have to foot the bill.

Notice of non-compliance penalties

For context, where the CRA makes a request for information or documents within 10 days and the timeline is not met, the CRA can issue a notice of non-compliance which keeps the limitation period open until the information or document is provided. The penalty that can be assessed for failing to comply is $25/day up to $25,000. These elements have not changed.

What has changed, however, is that there would be a new exclusion: if a taxpayer has a reasonable belief that the information or document is privileged, it may be legitimate not to provide it to the CRA, and the CRA cannot impose a penalty in that case.

While this is a win for taxpayers, it is important to note that there is no exclusion for the actual notice of non-compliance. Even where taxpayers are not assessed the penalty, they would still need to fight a notice of non-compliance (once issued), or the limitation period would be open forever. In addition, the exclusions from the penalties are only applicable if the document is protected by solicitor-client privilege. This does not address litigation privilege, settlement privilege, or common interest privilege. It remains to be seen whether a constitutional challenge will be brought in this regard when it becomes legislation.

The chart below summarizes the revisions to the proposed legislative amendments.

|

udget 2024 |

August 2024 Proposals |

|

Compliance order penalty = 10% of aggregate tax payable |

Compliance order penalty = up to 10% of aggregate tax payable |

|

|

|

|

CRA's information gathering powers and requirements (domestic and foreign-based) had to be complied without cost to the CRA |

Removed reference to the obligation to comply being without cost to the CRA |

|

Penalty if provided with notice of non-compliance for not providing information/documents to the CRA |

Penalty doesn't apply if one of the reasons for the person not complying was reasonable belief that the information/documents were protected by solicitor-client privilege |

Proportionality and Reasonableness of Information Requests

As the volume of discoverable documents continues to increase due to the accelerated digitalization of the corporate practice and the fact that all information accessible from Canada (including on foreign servers) is producible, the CRA also has more power now than ever to request documents. The CRA's expanded audit powers (most recently expanded in December 2022) are subject only to solicitor-client privilege and a very low relevance threshold.

In practice, taxpayers have had limited success in attempting to object to CRA requests on the basis of relevance. Moving forward, the combination of more documents being discoverable and expanded CRA audit powers may create the opportunity for taxpayers to be more successful making arguments based on the proportionality of CRA requests and the reasonableness of taxpayer attempts to respond (especially as the costs of responding to CRA requests significantly increase).

In Canada (National Revenue) v Cohen, 2025 FC 2012, the Federal Court declined to grant a compliance order under section 231.7 of the ITA with respect to the CRA's extensive request for information. In its reasons, the Federal Court made three main points that further support an argument on the basis of proportionality and reasonableness for taxpayers:

- reasonable efforts to comply with the CRA's request are sufficient;

- reasonableness depends on the context in question (e.g., the taxpayer provided 766 files, but would have been required to provide over 1,000 documents to satisfy the CRA's request); and

- the seriousness of the consequences of non-compliance must be taken into account when determining whether a compliance order should be issued (i.e., was the taxpayer unable to comply or was the taxpayer simply uncooperative?).

In light of this decision and the general trend of increased audit requests, taxpayers may want to consider monitoring the number of hours and total costs incurred (including advisors costs) in responding to CRA requests for information, so as to be prepared to make a future objection on the basis of proportionality or reasonableness, in appropriate and relevant circumstances.

In-house Loss Utilization is Not GAAR-able

Also discussed was a recent Federal Court of Appeal ("FCA") decision involving in-house loss utilization and GAAR: Canada v Quebecor Inc, 2025 FCA 207 ("Quebecor").

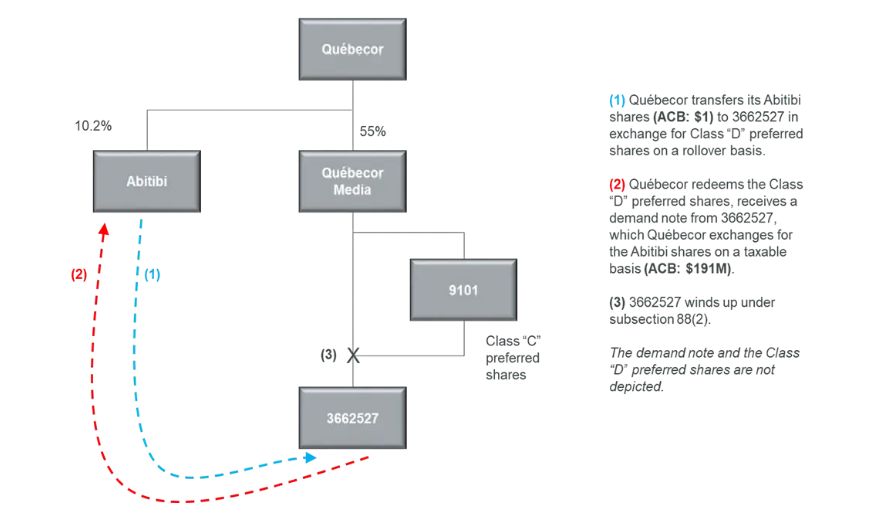

Briefly, per the diagram below, Quebecor owned the shares of Abitibi, which had a high fair market value and low adjusted cost base. So, there was a large unrealized capital gain. Quebecor also owned the shares of 3662527 ("366"). 366 owned the shares of Videotron, which had a low fair market value and a high adjusted cost base. So, there was a large unrealized capital loss.

The facts in Quebecor are summarized as follows:

- First, Quebecor transferred its shares of Abitibi to 366 in exchange for preferred shares of 366. This transfer was done on a tax-deferred basis.

- Second, Quebecor redeemed the preferred shares of 366 for a note equal to their fair market value. Quebecor used the note to purchase back the Abitibi shares at fair market value. 366 realized a capital gain as they sold the shares with the low-cost base.

- Finally, 366 was wound up. Notably, 366 was wound up in a manner such that subsection 88(1) of the ITA did not apply. Where subsection 88(1) does not apply to a wind-up, paragraph 69(5)(a) deems the proceeds of disposition of property, in this case the Videotron shares, to be at fair market value, not cost. So, 366 realized a capital loss on the disposition of the Videotron shares, which loss was not denied under the stop-loss rules due to paragraph 69(5)(d). As a result, the capital gain on the disposition of the Abitibi shares was offset against the capital loss on the disposition of the Videotron shares.

The CRA challenged the arrangement under the general anti-avoidance rule in the ITA ("GAAR"), claiming abusive tax avoidance. At the Tax Court of Canada, Quebecor conceded the existence of a tax benefit and an avoidance transaction, so the focus was whether there was abusive tax avoidance. The taxpayer won at the Tax Court of Canada and the Crown appealed.

The FCA agreed with the Tax Court of Canada finding no abuse.

- First, there was no abuse of the scheme applicable to windings-up. Since 366 was not a wholly-owned subsidiary, subsection 88(1) did not apply and instead paragraph 69(5)(a) applied, which deemed 366 to have disposed of the Videotron shares at their fair market value. That was clearly intended by Parliament.

- Second, the FCA also found that there was no abuse of the capital gains and capital losses scheme. There was no artificial increase resulting from an artificial loss. The loss was realized because the Videotron shares were deemed to have been disposed of.

- Third, the FCA found that a transfer or consolidation of losses between related persons was not abusive. The FCA referred to the technical notes on the GAAR and that in-house loss utilization was not abusive.

- Fourth, the FCA asked whether the Crown was arguing that 366 claimed a loss in respect of the Videotron shares that were still held by the group – i.e. not an actual disposition, but a deemed disposition – and whether that was abusive. The Crown took the position that the fact that the Videotron shares were still within the group was not abusive. As the Crown could not point to any abuse, the FCA found that the Crown had not established that there was a policy that was abused and that GAAR did not apply. This was a significant taxpayer win in the context of GAAR.

CRA Discretion and Judicial Review

The discussion ended on a recent administrative law case from the FCA: Jennings-Clyde (Vivatas, Inc) v Canada, 2025 FCA 225.

For context, discretionary CRA decisions (such as on interest and penalty relief, extensions of time to file, and other determinations where the CRA is not merely applying a computational rule but making a judgment call) are challenged via judicial review in the Federal Court. In these cases, the question is whether the CRA's decision was reasonable, including whether adequate reasons were provided.

This case involved a discretionary CRA decision and featured the following facts:

- The corporate taxpayer would have been in a refund position but had not filed its tax return for more than 3 years.

- There is a requirement in subsection 164(1) for a taxpayer to file its tax return within 3 years of the taxation year to get the refund.

- The taxpayer was out of time and so asked the CRA to extend the deadline, as the CRA has the authority under subsection 220(3) to extend the deadline to file a tax return.

- The CRA decided that it could not extend the deadline in subsection 164(1).

- The CRA only said that while there was another case that allowed an extension of a different refund provision, that case was different and the CRA would not extend the deadline.

Notably, no reason was given regarding what prohibited the CRA from not extending the time to file the return, why the other case was different, or the reasons or analysis for the decision. Moreover, the CRA did not request any submissions on the other case referred to.

The taxpayer sought a judicial review of the Minister's decision in the Federal Court. The Federal Court dismissed the judicial review on the basis that the taxpayer did not demonstrate that the CRA's interpretation was unreasonable. The taxpayer appealed to the FCA.

The FCA allowed the appeal and concluded that the CRA did not give an adequate explanation in its decision. The Court harshly criticized the CRA and explained why there is a need for adequate reasons – namely, it is a principle of administrative law that decision makers must provide adequate explanations for their decisions given the rights and interests affected.

Notably, the FCA did not just order the decision back to the CRA for reconsideration. Instead, the Court ordered the following: (1) the taxpayer be given a fair opportunity to make submissions on all relevant issues; (2) the CRA had to consider those submissions; and (3) the CRA had to redetermine the matter with adequate reasons.

This was a significant win for taxpayers: if the CRA decides to deny a request relating to a discretionary decision, and there are insufficient or inadequate reasons, taxpayers may have a good case for judicial review. It is important to note, though, that the court will not make the decision for the CRA but will, at best, send it back for redetermination.

Conclusion

From proposed changes to the CRA's audit powers; to the proportionality and reasonableness of audit requests; to new GAAR and administrative law tax cases, there are a plethora of new tax disputes developments one should keep in mind heading into 2026.

To view the original article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]