- within Strategy topic(s)

- with Inhouse Counsel

- in China

- with readers working within the Banking & Credit, Securities & Investment and Law Firm industries

Oversupply has long been an issue. Structural demand decline is now the crisis that no one has a quick fix for.

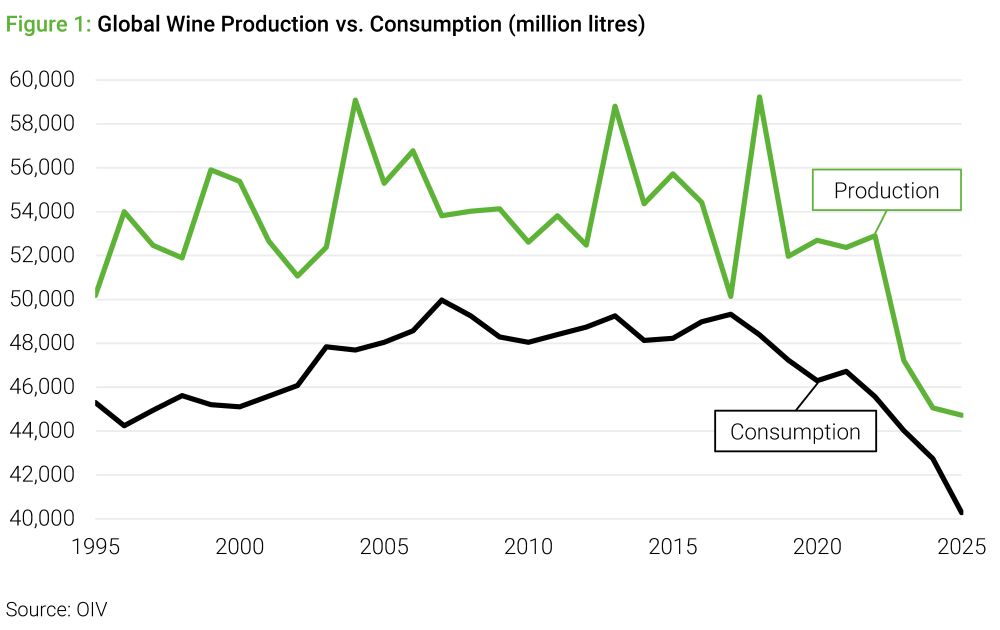

In 2025, global wine consumption reached its lowest level since 1961. In just two decades, the industry reversed 60 years of growth from its 2007 peak.

Having reached almost 50 billion litres in 2017, global consumption has fallen sharply every year since, reaching just 40 billion litres in 2025, a drop of 18% in eight years, and is forecast to drop a further billion litres by 2028. This is a structural reset, and it is accelerating.

Meanwhile, Australia produced 1.13 billion litres of wine in 2024-25, according to Wine Australia, comfortably outpacing total sales (domestic and export) of 1.08 billion litres. National stock levels rose 5%. The stock-to-sales ratio now sits at 1.9, some 15% above the ten-year average, with an excess of approximately 262 million litres sitting in tanks with nowhere to go. To put that in perspective: it is more than half of everything Australians drank last year, unsold and accumulating.

Behind all the numbers sit the businesses, regions, and the harder question of whether the industry has the capacity to respond.

How Australia got here

The structural problem was planted, literally, in the 1990s. Favourable tax settings and aggressive expansion by large wineries triggered a surge in vineyard plantings across warm inland regions, which didn’t slow until the late 2000s. In 2004, at the height of the export boom, Australia produced 3.4 times as much as its own population drank. Even in 2025, production runs at roughly double domestic consumption. For Australian wine, export markets have long been a structural necessity. By 2009, the industry had built more capacity than any realistic view of demand could justify. And then China arrived.

Throughout the 2010s, China’s appetite for Australian wine was almost insatiable, until Beijing imposed punitive tariffs on Australian bottled wine in 2020. The release valve closed overnight; suddenly, the oversupply that China had been quietly absorbing had nowhere to go. Production that had been calibrated to include a vast, high-value export market was now stranded.

When China lifted those tariffs in March 2024, the industry exhaled. But the market Australia is returning to is not the one it dominated five years ago. China is now a premium market for Australian wine, not a volume one, and is not expected to return to the lavish levels seen before the tariffs.

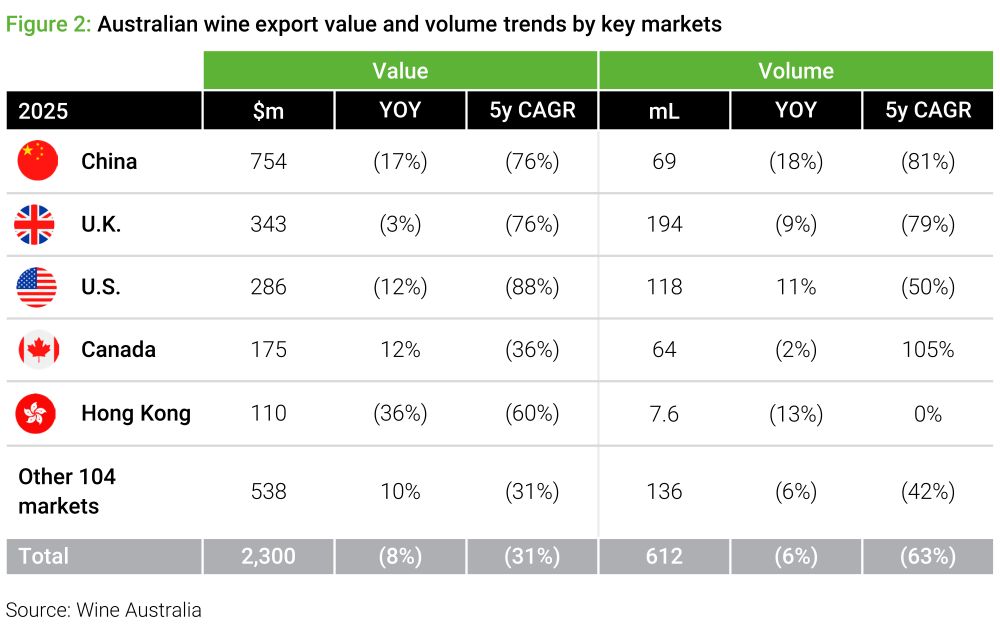

The broader picture gives little comfort. Exports fell 3% in value and 4% in volume to levels we haven’t seen for decades. The U.S., historically Australia’s second-largest market by volume, recorded a 17% decline in volume and a 9% decline in value before the U.S. Administration’s 10% tariff was added in April 2025. In the year that followed, value fell another 22%. The U.K., Australia’s largest market by volume, continues to contract. Every major export pillar is weakening simultaneously. The industry spent a decade avoiding a structural reckoning. It is now facing several at once.

A permanent shift in how the world drinks

Wine’s problem is not just about who is drinking less. It is about where the remaining demand is concentrating. The premium end of the global market (wines above US$10 per bottle) is holding up. Commercial and bulk wine, however, are in structural decline, falling at an average of 4% per year over the past five years. This is especially challenging for Australia where in its two largest export markets (U.S. and U.K.), the country’s wine has become synonymous with cheap, fruit-forward Shiraz. That identity was once a commercial advantage; today it has become a structural liability.

Total wine spend is not collapsing. Global wine value grew by 1% in 2024, even as volume fell by 3%. Globally, and in Australia, we are drinking less wine but spending more per bottle. The category faces polarisation, not collapse. The businesses best positioned to survive are those that understand the difference.

Who bears the pain?

Grape growers in the warm inland irrigated regions (Riverina, Riverland, Murray Darling) carry the most acute pain. Close to three-quarters of Australia’s grapes are grown in these areas, predominantly red varieties, with average prices in 2024 of ~A$345 per tonne. In 2024, Shiraz recorded its lowest ever price in the past 15 years, having dropped 63% in the past four years alone to just A$249/tonne. Compare that with A$1,531 per tonne for cool-climate premium fruit. Many growers have been unable to sell their grapes at all, leaving fruit unharvested. Speaking firsthand with a winemaker recently, many growers have already exhausted their savings to stave off the unprofitable years. They no longer have the capital to change their operations away from grape growing, even if they wanted to.

At the corporate level, the rationalisation underway speaks for itself. One of Australia’s largest wine groups booked almost A$1 billion pre-tax non-cash impairment on its U.S.-based assets and attempted to divest its entire commercial portfolio, but had to retain them by default when no buyer emerged. Others are cutting brands in a move toward premiumisation. The decision by one of the world’s largest spirits companies to exit wine entirely itself signals where institutional confidence in the category now sits.

What a credible recovery looks like

There is no quick fix. The inventory overhang alone will take years to work through. A credible recovery requires a sequence of hard decisions to be made before the market makes them by default.

- Right-sizing supply is the precondition for everything else. Coordinated vineyard removal, targeted at oversupplied warm-inland red varieties and guided by accurate supply data, is the only mechanism that addresses the structural imbalance at its root. For large wine companies, premiumisation cannot succeed while the category is defined by surplus and commodity pricing. Scarcity supports value, and the industry needs to act with more urgency than it has shown so far.

- The strategic shift from volume to value has moved beyond aspiration to survival. Australia has demonstrated it can compete at the premium end. Penfolds’ recovery in China is proof that the country’s top-tier reputation remains intact. The question is whether the broader industry can reposition away from the identity that has dominated its export profile for two decades: affordable bulk red. That repositioning requires investment in brand, region and story, at a moment when margins are under maximum pressure, yet the alternative is to continue competing on price in a segment that is structurally shrinking.

- Export diversification must be pursued with realistic expectations. Southeast Asia offers a near-term opportunity, while India is the longer-term prize. Australia exports just A$9.3 million in wine to India annually, compared with a peak of more than A$1 billion to China. India’s wine market is projected to grow up to 16% annually to 2033, according to market forecasts. Around 19 million Indians reach legal drinking age every year, bringing with them a growing middle class, improving wine infrastructure and bearing no historical baggage with Australian wine. No other market generates that pipeline. India will not solve today’s crisis, though; building a presence across both markets will be patient, relationship-driven work over a decade or more. The companies that don’t start now will be playing catch-up.

- Production must align with where demand is actually going. That means more whites, more sparkling, more lighter-style reds, and investment in alternative varietals, Fiano, Vermentino, and Tempranillo, which are finding genuine market traction. Procurement and contracting decisions made today will shape what the industry looks like in 2035.

A reset, not a collapse

The Australian wine industry is not broken. It is overbuilt for a world that is drinking less and wants different things. The distinction matters. The response to a broken industry is managed decline. The response to an overbuilt one is deliberate restructuring.

The wines being made at the premium end, from Yarra Valley Pinot Noir to Tasmania’s world-class sparkling, from McLaren Vale old-vine Grenache to Margaret River Cabernet, are genuinely world-class. The problem lies elsewhere: the volume of commodity red wine sitting in warm-inland tanks, produced at a cost that exceeds what the market will pay, by an industry that has not yet fully reconciled itself to a permanently smaller demand environment.

The real strategic challenge is the resistance to acknowledging that the industry’s own footprint must fundamentally change. The companies that navigate this reset successfully will not wait for conditions to improve; they will be making deliberate strategic choices while others hesitate.

The next decade of Australian wine will be smaller in volume. Whether it emerges stronger in value depends on whether the industry can make the hard structural decisions now, before the market – and the vines it doesn’t bother to save – makes them instead.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]