- with readers working within the Technology industries

Securing Refunds for Invalidated IEEPA Tariffs Following the Supreme Court Ruling

On February 20, 2026, the Supreme Court invalidated the tariffs imposed under the International Emergency Economic Powers Act (IEEPA). This means that duties the United States collected under the IEEPA in 2025 and 2026 could potentially be refunded. Federal Express has already filed suit as-of February 23, 2026 seeking refunds.

An analysis by the Penn Wharton Budget Model estimates the amount of potential refunds at $175 billion. However, the high court's ruling did not establish, or even discuss, a mechanism for potential refunds. To secure potential refunds, businesses must track their import entry status and adhere to specific legal procedures and strict deadlines.

This need for prompt action is critical given the current political climate. As noted in the article, Act Fast for Tariff Refunds as Trump Walks Back DOJ Assurances, "[f]or importers and their counsel, the clock is ticking. The path to recovery will demand swift, strategic—and potentially aggressive— action amid mounting uncertainty, as the administration's post-ruling stance signals a more combative fight over the return of the tariffs."

Understanding Affected Tariffs

The Supreme Court's decision applies only to IEEPA-based tariffs.

- The invalidated tariffs include the pure IEEPA global "reciprocal" tariffs; emergency trafficking/immigration tariffs on Mexico, Canada, and China; and the targeted IEEPA surcharges on Brazil and India.

- The ruling does not affect tariffs imposed under other statutory authorities, such as Section 301 (China programs) or Section 232 (steel and aluminum).

- Moving forward, importers must also account for the newly implemented 15% global tariff under Section 122 of the Trade Act of 1974, effective February 24, 2026 and legally limited to a 150-day duration unless extended by Congress. These new tariffs are entirely separate from the invalidated IEEPA duties and are not covered by the recent Supreme Court ruling. Businesses cannot use the IEEPA refund mechanisms to offset these new costs.

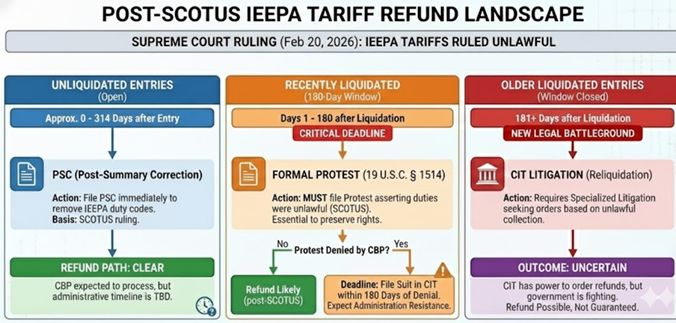

The Role of Liquidation in Securing Refunds

A business's procedural path to a refund depends primarily on the entry status of their imported goods—specifically, whether the entries remain "unliquidated" or have been "liquidated." Import entries typically liquidate (become final) 314 days after the entry date.

- Unliquidated Entries: For entries that have not yet been liquidated, importers can utilize Post-Summary Corrections (PSCs). This process allows businesses to strip out the unlawful IEEPA duties and formally request refunds of excess deposits.

- Recently Liquidated Entries (Within 180 Days): If entries have liquidated within the past 180 days, importers must file a formal protest under 19 U.S.C. § 1514. The protest must assert that the duties were "not required by law." If the protest is denied, the importer then has 180 days to escalate the matter by filing suit in the Court of International Trade (CIT).

- Older Liquidated Entries (Beyond 180 Days): Entries that liquidated more than 180 days ago represent the biggest gray area. Once the standard 180-day window closes, recovering funds will likely require specialized litigation in the CIT. Recent DOJ briefings and CIT precedent suggest the government may not argue that liquidation alone bars refunds where tariffs were ultimately found to be unlawful, although this position may certainly change.

Why Prompt Action is Necessary

Timing is a critical factor for businesses seeking to reclaim these unlawfully collected tariffs.

- Strict Deadlines: Ensuring timely filings of PSCs or formal protests is the key timing consideration, as missing the 180-day post-liquidation window limits administrative recourse and forces more complex litigation.

- High Volume of Claims: An estimated 34 million entries subject to these tariffs were made by over 300,000 importers of record. Thus, a massive number of refund claims is anticipated. Businesses should act quickly to get "first in line" as agencies navigate the backlog.

- Funding Limitations: Given that interest may also be owed on these claims under 19 U.S.C. § 1505(b), it is plausible that the funds earmarked for refunds could eventually face shortfalls or political delays.

- Fluid Political Landscape: Given the novel and unprecedented scale of claims, it is also possible additional legislation, or other action could rapidly change the landscape and process, but potentially not on a retroactive basis. Because of this uncertainty, acting sooner (and prior to any additional legislation) may create substantively better positions on a going forward basis.

Downstream and Contractual Considerations

While the government owes the refund directly to the Importer of Record who paid the tariff, there are downstream commercial implications.

- Many importers passed the cost of these tariffs onto their customers through "tariff surcharges."

- Businesses should review their commercial contracts to determine how these agreements allocate responsibility or rights regarding tariff refunds.

Next Steps for Businesses

To preserve their rights, businesses should take immediate action to organize their import records. Specifically:

- Map Affected Entries: Identify all historical and pending entries where IEEPA-based tariffs were paid.

- Segment the Data: Categorize these entries into three distinct groups to determine the correct legal pathway: unliquidated entries, entries liquidated within the last 180 days, and entries liquidated beyond 180 days.

- Secure Independent Documentation: Maintain accurate, independent backup copies of all entry documentation. Do not rely solely on future access to CBP's Automated Commercial Environment (ACE) system.

- Consider Immediate Litigation: Consider filing an immediate suit, similar to that already filed by Federal Express.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.